VantageScore spots ‘subtle migration’ of consumers toward lower credit tiers in March

Charts courtesy of VantageScore.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

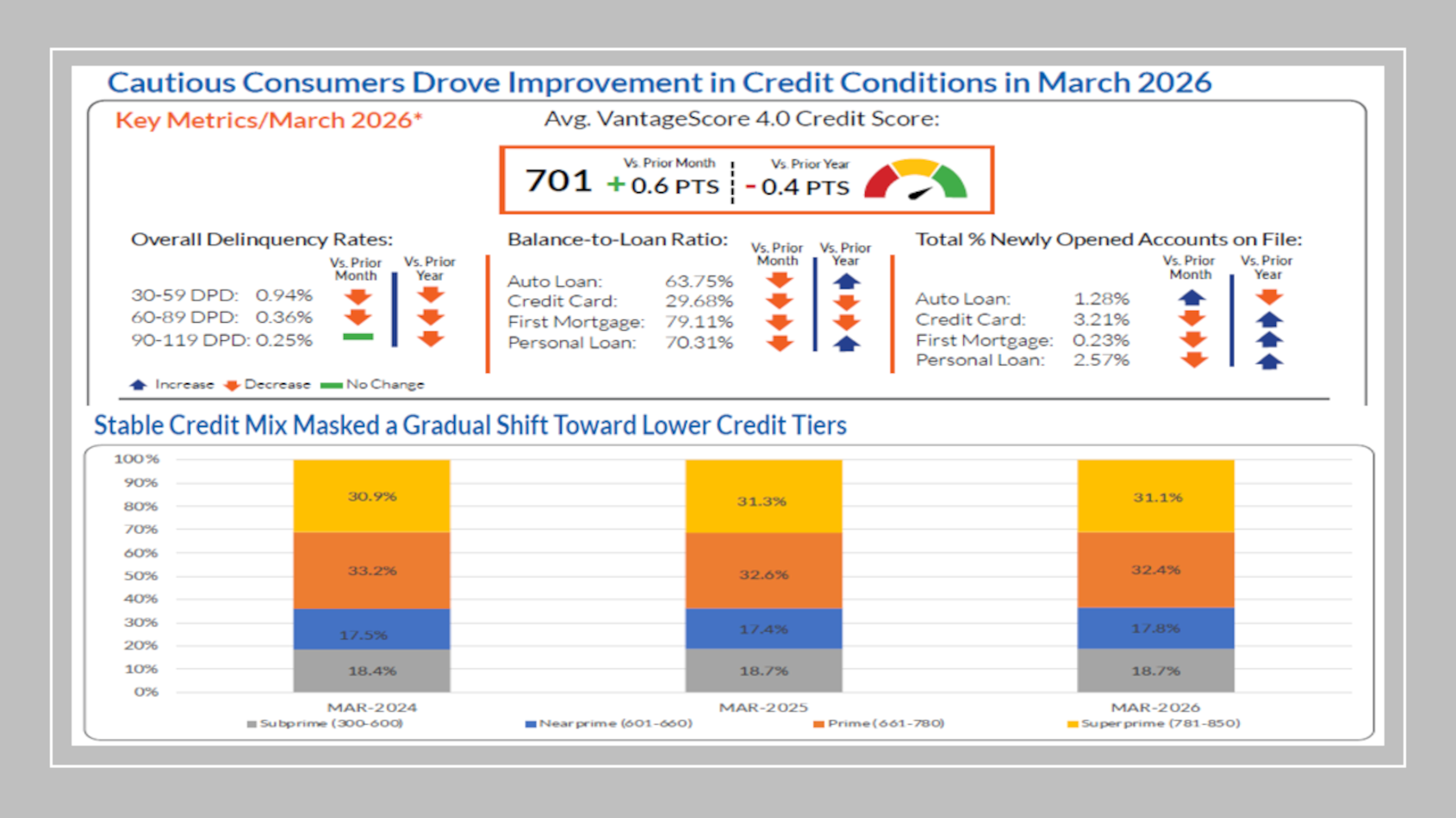

The March edition of CreditGauge from VantageScore showed the average VantageScore 4.0 credit score held steady at 701, reflecting continued consumer resilience amid elevated borrowing costs and broader macroeconomic uncertainty.

Analysts explained in the report that the distribution of consumers across VantageScore credit tiers stayed largely stable, with a slight shift toward lower tiers.

Year-over-year, the VantageScore subprime share remained flat at 18.7%, while the VantageScore near-prime segment increased by 0.4% to 17.8%.

Meanwhile, VantageScore noted its prime (32.4%) and super-prime (31.1%) categories declined modestly, each edging 0.2 points lower.

“This subtle migration toward lower tiers suggests that despite stable average scores, underlying pressure persists for some borrowers. This points to a bifurcated consumer population, where stronger borrowers remain stable while others gradually weaken,” analysts said in the report.

In a video that accompanied CreditGauge (available in the window below), VantageScore senior vice president and head of credit insights Atif Mirza said, “So consumers are managing their credit obligations well. However, we do see some signs of stress emerging, especially in early-stage delinquencies where we saw they rose in February to 1.15 percent, same levels as we saw in pre-pandemic in January of 2020. What’s notable is that the stress is not just concentrated in high-risk borrowers.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“It’s expanding from subprime into prime and even super-prime levels as well. That tells us that the financial stress is growing, and we saw that with the slowdown in new hires, elevated interest rates, and high cost of living,” Mirza added.

Looking closer at just auto finance, VantageScore indicated the average outstanding balance rose to $24,900, increasing modestly month-over-month and moving up 2.1% year-over-year.

Meanwhile, analysts pointed out the balance-to-loan ratio edged down by 0.09% to 63.75% from February.

“Higher loan balances alongside a slight decline in balance-to-loan ratios point to continued price pressure in auto markets,” VantageScore said in the report.

When looking at auto-finance originations, analysts noticed that they rose by +0.1% month-over-month for Gen Z, Millennials and the Silent Generation, while remaining unchanged for Boomers and Gen X.

Comparing year-over-year, VantageScore mentioned auto-loan originations declined across all generations, with the largest decreases seen among the Silent Generation (0.6% to 0.5%) and Boomers (1.0% to 0.9%).

Analysts also determined that overall credit delinquencies declined across all stages month-over-month, indicating improvement in borrowers catching up on payments.

VantageScore explained year-over-year delinquency improvements were driven primarily by mortgages, which decreased due to unusually high refunds with the State and Local Tax (SALT) deduction increase, greatly benefiting mortgage holders.

Analysts added average credit card balances declined month-over-month from February, contributing to a drop in utilization to 29.68%, which fell both month-over-month (0.72%) and year-over-year (0.23%).

VantageScore attributed the decline in revolving balances provided “clearer” evidence of consumer deleveraging, suggesting households are paying down debt and moderating spending, supported in part by seasonal inflows such as tax refunds.

“Improved credit conditions this month reflect a cautious but resilient consumer who is actively managing debt and moderating borrowing,” said Susan Fahy, executive vice president and chief digital, data and technology officer at VantageScore.

“The decline in credit card balances and stabilization in delinquencies point to households prioritizing balance sheet health even as economic pressures persist,” Fahy added in a news release.