Experian: Subprime share, overall terms keep climbing in Q1

Chart courtesy of Experian.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

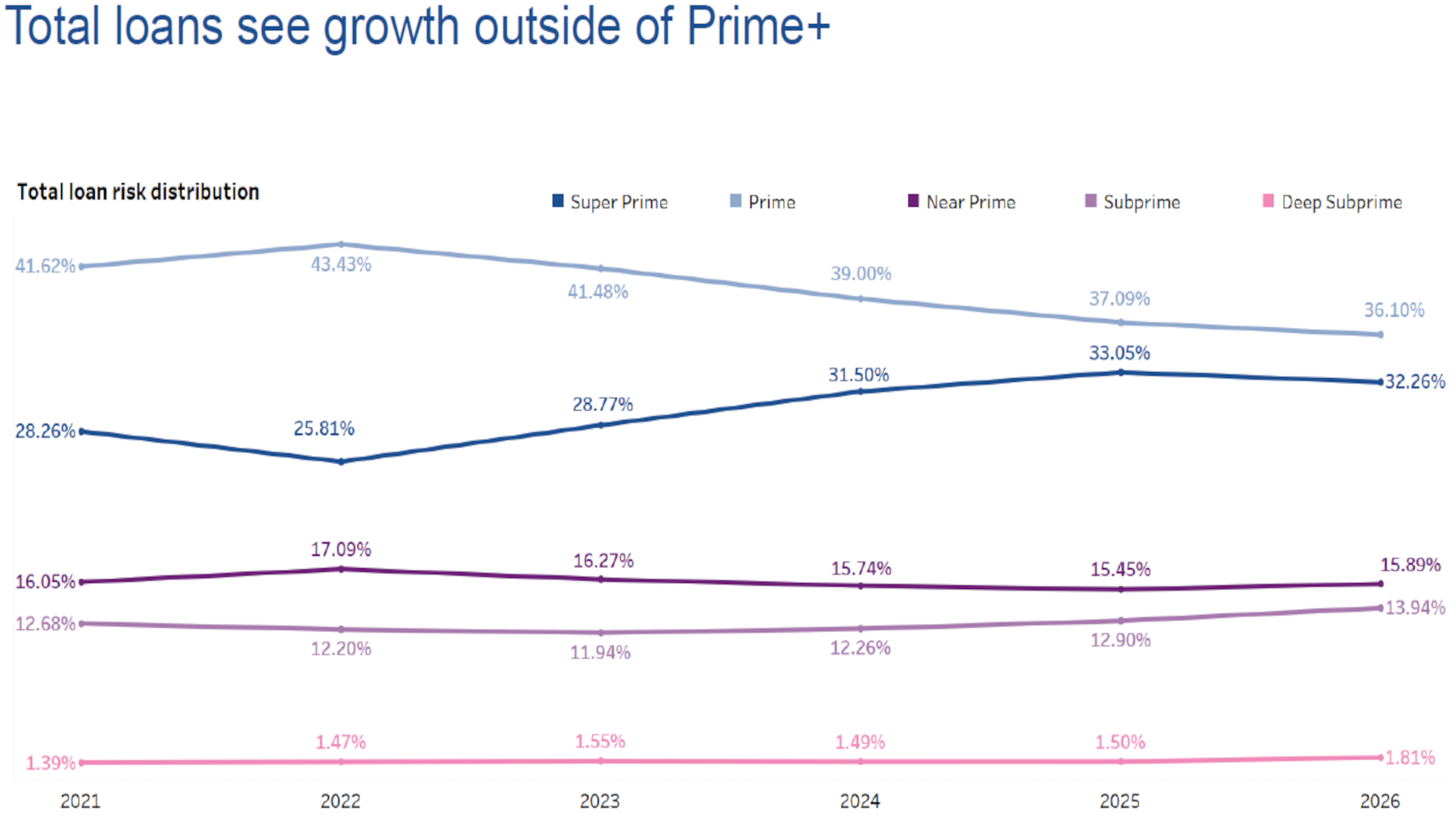

As contract terms keep stretching throughout auto financing, Experian is seeing a gradual increase in the subprime segment, too.

According to Experian’s State of the Automotive Finance Market Report: Q1 2026 released on Thursday, subprime consumers made up 15.75% of total vehicle financing booked during the first quarter. That level represented an increase from 14.40% last year.

For new vehicle financing, analysts noticed the subprime market grew year-over-year to 6.88% from 5.61%. In used-vehicle financing, the subprime market increased from 19.36% last year to 20.60% this past quarter.

“There continues to be increased momentum within the subprime segment as financing options expand across the automotive finance market,” said Melinda Zabritski, Experian’s head of automotive financial insights.

As affordability remains a top priority across the automotive market, Experian spotted that longer contract terms are being booked to get consumers into what they deem to be manageable monthly payments.

Experian reported the percentage of new vehicles with loan terms stretching more than six years reached 35.55% in Q1 2026, up from 30.83% a year ago.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Additionally, new loans with terms longer than 85 months increased from 2.95% to 3.33% over the same period.

Analysts noticed a similar pattern in the used-vehicle market.

The percentage of used vehicles with loan terms of more than six years hit 31.54%, up from 28.60% in Q1 2025.

Meanwhile, used vehicles with financing terms of more than 85 months grew to 1.40% in Q1, from 1.32% the year prior.

“Affordability continues to shape financing decisions across the automotive market,” Zabritski said in a news release. “While shoppers continue to lean toward larger, more expensive vehicles, we’re seeing more consumers take advantage of longer-term loans to offset rising monthly costs.”

In the first quarter of 2026, the average loan amount for a new vehicle increased $2,150 year-over-year, reaching $43,925, while the average monthly payment for a new vehicle increased from $748 to $770 during the same period.

On the used side, the average loan amount saw an uptick of $785 from a year ago to $27,070 in Q1, and the average monthly payment grew from $523 last year to $531 this poast quarter.

Interestingly, while the average monthly payment for new vehicles continues to rise, Experian mentioned nearly 20% of new vehicles had an average monthly payment less than $500 in Q1.

Refinancing gaining more traction

As interest rates steadily decline, Experian said refinancing has increasingly become an option for consumers looking to ease monthly payment pressures, as well as lenders hoping to find ways to offer more competitive rates.

In Q1, on average, Experian determined consumers trimmed 2.2% off their interest rate after refinancing. The average refinanced interest rate was 8.05%, down from 10.29%. This lowered the average monthly payment by $81 for consumers who refinanced during the quarter.

Interestingly, analysts found that credit unions accounted for the largest share of automotive refinancing at 63.43%, from 62.31% in Q1 2025, compared to banks going from 23.51% to 22.59%.

In addition, the payment difference when refinancing with credit unions was $101 this quarter and those who refinanced with banks saved $60, according to Experian.

Zabritski said, “Consumers are benefiting from improved refinancing conditions.”

Other notable trends

Experian pointed out a few additional findings from its Q1 data, including:

—The average loan term for a new vehicle was 69.48 months this quarter, and the average loan term for a used vehicle was 67.73 months.

—Banks accounted for 28.42% of total market share in Q1 2026, followed by captives (26.83%), and credit unions (20.09%).

—30-day delinquencies rose to 2.00% in Q1 2026, from 1.95% in Q1 2025, while 60-day delinquencies increased from 0.83% to 0.86% year-over-year.

—New electric vehicle financing declined from 10.93% last year to 6.23% this quarter, and hybrid vehicles increased from 12.08% to 14.90%.

To learn more, watch the entire State of the Automotive Finance Market Report: Q1 2026 presentation on demand.