Explaining ‘genuine crosscurrents’ that could impact auto finance & retail this summer

Charts courtesy of VantageScore.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Jeremy Robb might have single-handedly summarized data and observations offered by Comerica Bank, Cox Automotive and VantageScore in recent days.

“For dealers, the picture heading into summer is one of genuine crosscurrents,” Robb, who is Cox Automotive’s chief economist, wrote in his weekly analysis Monday.

The job market, interest rates and credit performance are among those crosscurrents pointing to even the most resourced consumers taking cautious approaches to spending nowadays.

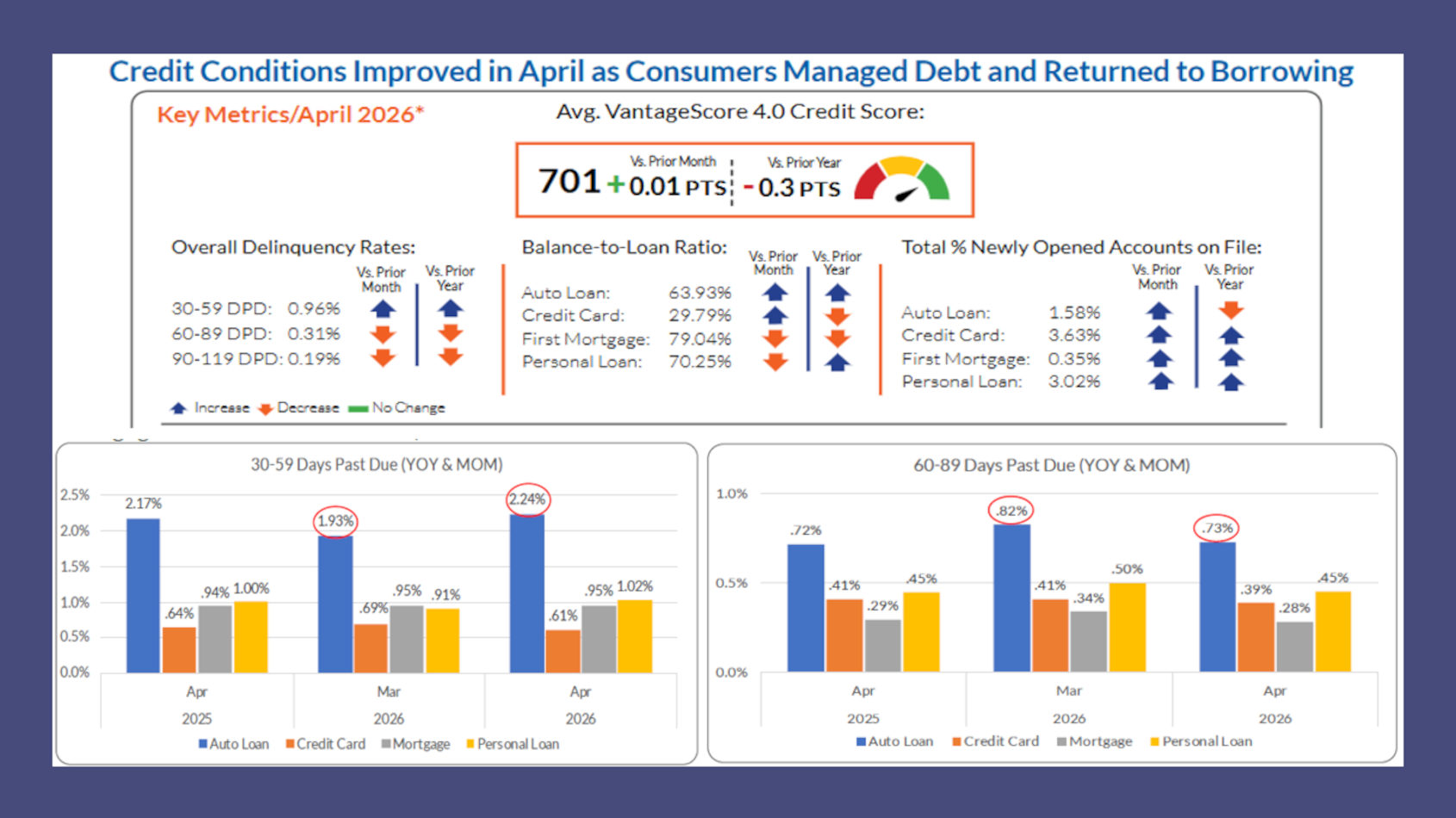

According to the latest edition of CreditGauge from VantageScore, the average VantageScore 4.0 credit score held stable at 701 in April, indicating that consumer credit health remains stable despite elevated interest rates and persistent affordability pressures.

Analysts explained in the report that consumer credit conditions in April continued to stabilize as delinquency trends improved across most stages and products, supported by seasonal tax-related relief and disciplined balance management.

VantageScore also noted that the distribution of consumers across credit tiers remained largely unchanged year-over-year in April, reinforcing the broader stability in consumer credit quality.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Analysts indicated the subprime and super-prime segments both remained flat at 18.7% and 31.0%, respectively, while near-prime increased modestly to 17.8% and prime declined slightly to 32.5%.

Susan Fahy, executive vice president and chief digital, data and technology officer at VantageScore, said the limited movement across tiers suggests credit conditions are stabilizing overall, though some pressure persists among middle-tier borrowers.

“April’s data points to a consumer that is exercising restraint,” Fahy said in a news release, adding, “consumers continued to preserve credit capacity and borrow selectively despite ongoing affordability pressures.”

Of course, consumers usually can afford things like car payments, mortgages, utilities and more if they’re gainfully employed. That’s the part of those crosscurrents covered by Bill Adams, chief U.S. economist at Comerica Bank.

“Employers added a solid 172,000 jobs in May, well above the 88,000 consensus and our forecast of 85,000,” Adams wrote in an analysis Monday. “Job growth was concentrated in leisure and hospitality, up 70,000, local government, up 55,000 and health care and social assistance, up 47,000, three industries that are relatively insulated from the effects of AI. The unemployment rate held steady at 4.3%.

“In the survey of households, the labor force rose 83,000, but was down 414,000 on the year, equivalent to 35,000 per month,” he continued. “The economy has added 114,000 jobs per month so far in 2026, up from a paltry 10,000 per month last year. This trend could lower the unemployment rate in the second half of 2026 if sustained, and even cause labor supply bottlenecks by next year. That would pressure the Fed to raise rates even if the inflation shocks from the Iran War and tariffs fade.

“But for now, the risk is hypothetical: A 4.3% unemployment rate isn’t a call to action for the Fed,” Adams added.

As dealers and lenders navigate the official arrival of summer later this month, Robb explained what might be ahead.

“Price pressure is showing up beyond the automotive showrooms. Executives at major public retailers — including Dollar General, Five Below, Ollie’s, Macy’s, and Ulta Beauty — have cited elevated fuel prices as the single largest consumer headwind, consistent with the Federal Reserve’s May Beige Book,” Robb wrote in his analysis. “The income bifurcation that has defined this market has escalated since the Middle East conflict began and is becoming more entrenched: Lower-income consumers are under meaningful stress, middle-income households are deferring non-essentials, and even higher-income consumers are turning cautious.

“New-vehicle demand at the higher end of the market remains. Used-vehicle demand and trade-in values continue to benefit from substitution effects,” he continued. “Credit availability remains near multi-year highs. But gas prices near $4.25 nationally, rising Treasury yields, and consumers increasingly cautious on discretionary spending are creating real headwinds for volume in the mid-market.

“This week’s Consumer Price Index (CPI) and Producer Price Index (PPI) releases will be the first comprehensive read on inflation pass-through from the energy price shock and will likely shape the rate outlook for the remainder of 2026,” Robb went on to write.