Equifax sees auto lenders looking to subprime for growth opportunities

Chart courtesy of Equifax.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

As total outstanding balances and accounts moved in opposite directions, Will Holleman highlighted notable trends specific to subprime auto financing contained in the Equifax May 2026 Credit Trends report released this week.

The vice president of sales for auto at Equifax Workforce Solutions pointed out that year-to-date, subprime accounts — consumers with a VantageScore 3.0 reading of 620 or lower — rose by 10.1%, while subprime balances jumped 17.7% year-over-year.

In fact, Holleman said a “striking” 20.0% of all auto originations were booked with subprime buyers.

“Lenders are searching for growth in riskier tiers, and the data shows they are finding it,” Holleman said via social media.

Looking at overall metrics from the report, the Equifax data showed total outstanding balances on auto loans and leases have increased 2.2% year-over-year to $1.70 trillion.

Analysts noted the number of outstanding auto loan accounts has decreased 0.9% year-over-year to 79.38 million.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

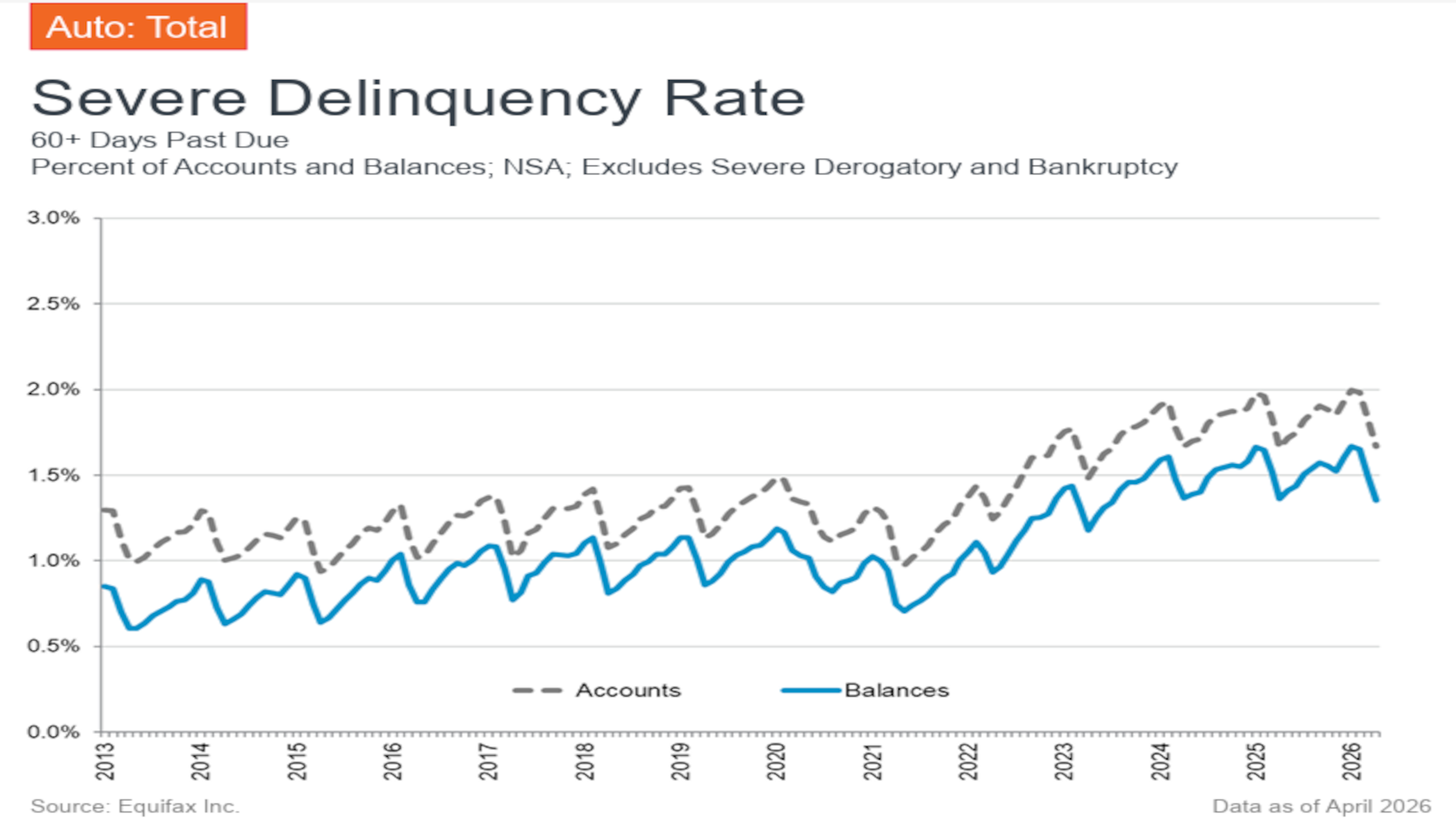

Equifax added the severe delinquency rate — what the company considers to be the share of balances 60 days or more past due — came in at 1.36% in April, “which is comparable to April 2025.”

And analysts mentioned auto write-offs stood at 26.8 basis points in April, up from 26.0 bps in the previous year.

In another commentary on social media, Holleman delved into how finance companies are trying to gauge the risk they’re bringing into their portfolios.

“While current employment proves immediate income, prior employment records provide the context of time and behavior,” Holleman said.

Holleman explained that Equifax data shows that employment history — specifically job frequency —can be “a powerful predictor of loan performance.”

According to an Equifax internal study of auto loans, Holleman recapped that historical employment stability correlates directly with 90-day past due rates:

—The stability advantage: Consumers with only one previous job recorded have a rate of 3.8%.

—Moderate risk: Those with two previous jobs show a rate of 4.9%.

—The high-frequency gap: Conversely, consumers with seven or more previous jobs present a significantly higher risk, with an 11.3% rate.

“Incorporating previous employment data allows lenders to look beyond current income alone. If a consumer has just started a new role but possesses a stable history with a previous employer, that data serves as a powerful indicator of stability,” Holleman said.

“By integrating previous employment data points into the initial decisioning workflow, lenders can expand their pool of actionable records, optimize their risk pricing, and capture profitable subprime volume that traditional metrics overlook,” he continued.

“In a competitive market, the lenders who win won’t just be the ones looking at where a consumer is today. They’ll be the ones using historical data to predict where they are going tomorrow,” Holleman went on to say.