How auto performed in May within ‘resilient consumer credit landscape’

Charts courtesy of VantageScore.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

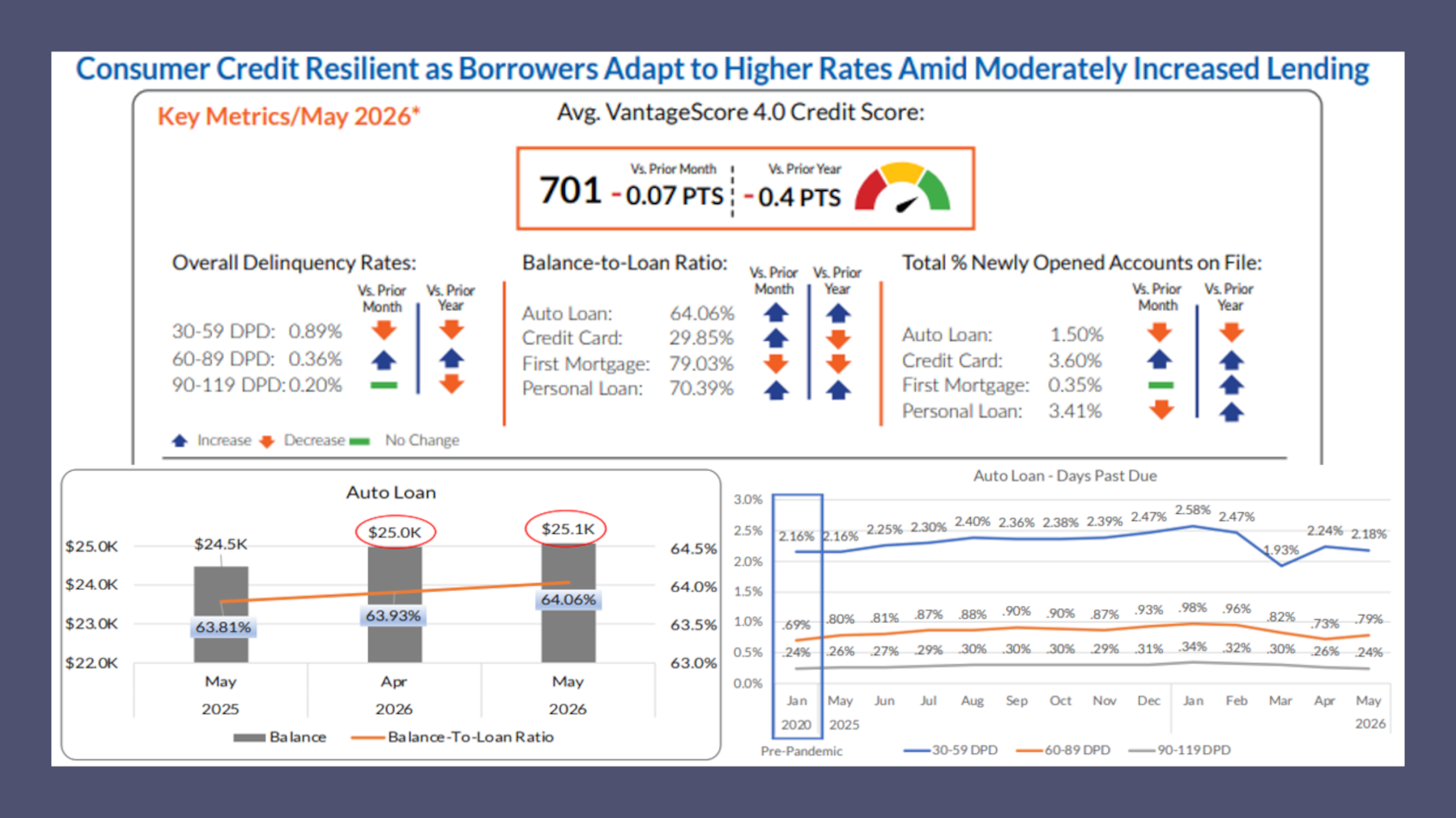

Amid “a resilient consumer credit landscape,” the latest edition of CreditGauge from VantageScore showed the average auto loan balance in May rose to $25.100, increasing modestly month-over-month and 2.5% year-over-year.

Analysts also indicated the balance-to-loan ratio ticked up 0.13% to 64.06% in May and is now 0.25% above the year-ago level.

VantageScore said the balance-to-loan ratio reflects the average balance-to-loan amount on open and active installment accounts.

“Rising balances alongside an increasing balance-to-loan ratio point to sustained vehicle price pressure and thinning down-payments,” analysts said in the report released Wednesday.

VantageScore noticed auto-finance originations declined slightly in May, “reflecting pull-forward effects from 2025.”

Noticing that the origination slowdown happened no matter the age demographic, analysts added the trajectory “is consistent with softer vehicle demand following the tariff–related purchase pull-forward observed in 2025.”

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Furthermore, VantageScore reported delinquency rates in May for auto loans stayed predominantly near year-ago readings:

—30 to 59 days: 2.18%

—60 to 89 days: 0.79%

—90 to 119 days: 0.24%

Looking at the overall market, VantageScore determined consumer credit performance remained healthy in May.

Meanwhile, the average VantageScore 4.0 credit score held steady at 701, reinforcing the overall stability of consumer credit health.

Atif Mirza, executive vice president and chief digital and insights officer at VantageScore explained delinquency rates across all delinquency stages remained below pre-pandemic levels, suggesting that most borrowers have successfully adjusted to a prolonged, higher-rate environment despite ongoing affordability challenges.

Mirza noted that taken together, these indicators point to a resilient consumer credit landscape, even as elevated interest rates and cost-of-living pressures persist.

“While consumer sentiment has softened in recent months, the underlying credit data tells a more stable story,” Mirza said in a news release. “Delinquency rates remain below pre-pandemic levels across all delinquency stages, reflecting the continued resilience of consumers despite elevated interest rates and rising household expenses.

“Coupled with a rebound in new credit originations, these credit trends point to a credit market that remains healthy and accessible,” he went on to say.