PayNearMe research: Lenders sustain more than $100B in costs beyond transaction fees annually

Graphic courtesy of PayNearMe.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

It’s a cliché to say it takes money to make money. Well, new research from PayNearMe connected some specific figures to that saying for auto lenders and others involved in financial services.

The platform that supports all major payment types and channels reported on Tuesday the U.S. bill pay market incurs more than $100 billion annually in payment acceptance costs beyond transaction fees.

The company’s new Payment Experience Gap report found that the total cost of payment acceptance is approximately six times higher than what bill pay organizations typically measure through transaction fees alone.

PayNearMe said these costs rarely appear on a processor invoice, yet they represent more than 80% of the total cost of payment acceptance.

As lenders and other bill pay organizations increasingly focus on improving efficiency, reducing operational costs and protecting margins, the report introduced the Payment Experience Gap.

“The new framework helps organizations understand the difference between what they believe payments cost and the actual costs incurred across the payment journey once the impacts of payment friction, support and operational costs are included,” PayNearMe said in a news release.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

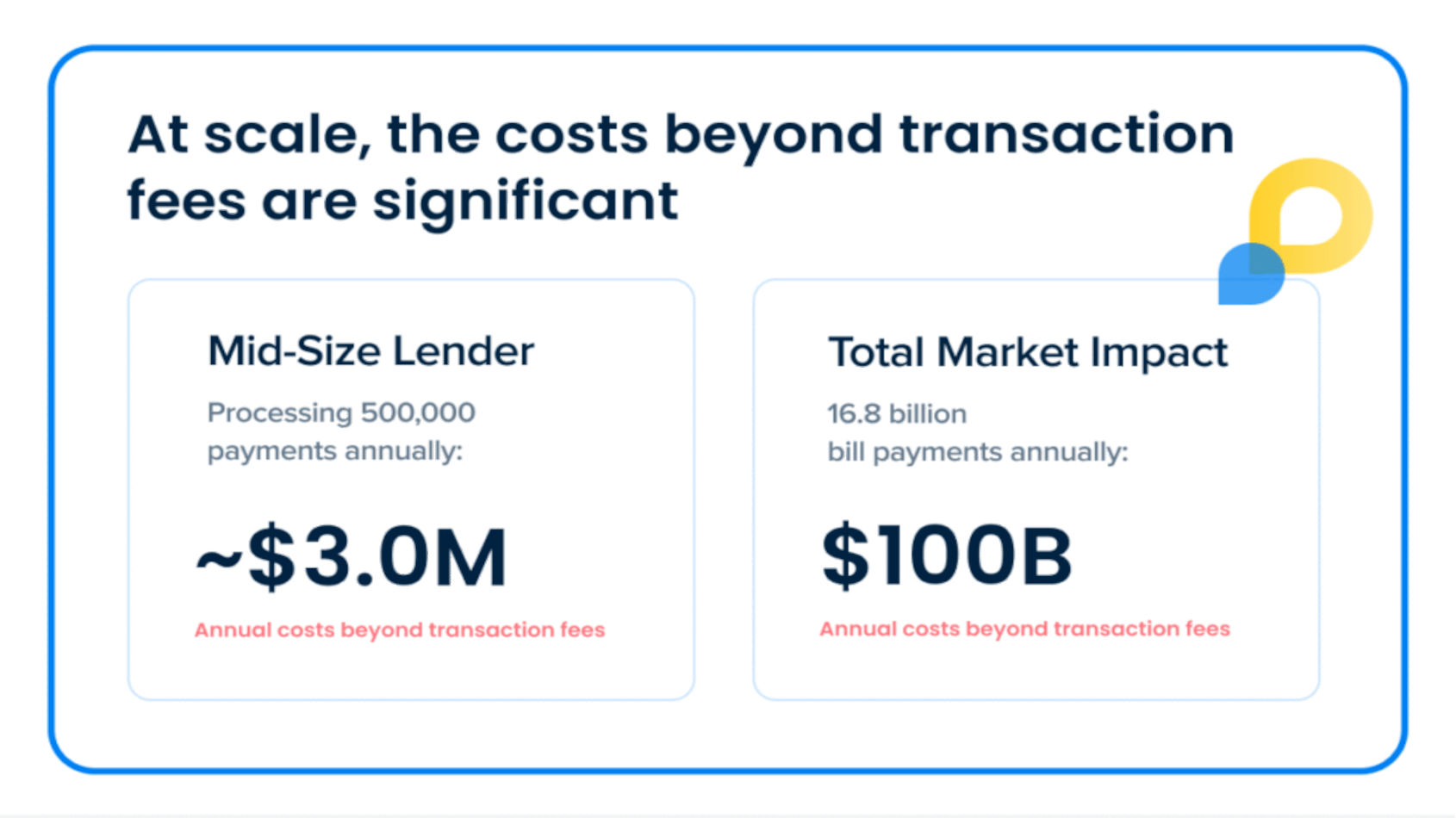

Based on a representative lending environment, the analysis found that businesses incur approximately $7.22 in total cost per payment, including $1.20 in transaction fees and an additional $6.02 in costs beyond transaction fees.

For a mid-market to enterprise lender processing 500,000 payments annually, this equates to approximately $3 million in additional payment-related costs.

For auto lenders, PayNearMe said that hidden cost can show up as failed payments, borrower support calls, late payments, collections follow-up, reconciliation work and manual recovery effort.

“In other words, some payment problems are not only about whether a borrower can pay. They are also about whether the lender makes it easy enough for the borrower to complete the payment,” PayNearMe said.

PayNearMe reiterated key findings from its report include:

—U.S. bill pay organizations incur more than $100 billion annually in payment acceptance costs beyond transaction fees.

—The total cost of payment acceptance is approximately 6× higher than what organizations typically measure through transaction fees alone.

—More than 80% of the total cost of payment acceptance exists outside of transaction fees.

—Businesses incur approximately $7.22 in total cost per payment, including $1.20 in transaction fees and an additional $6.02 in costs associated with customer experience, support and operations.

—A representative mid-market to enterprise lender processing 500,000 payments annually incurs approximately $3 million in costs beyond transaction fees.

—Support represents the single largest cost category at approximately $2.70 per payment.

—Operational costs average approximately $2.01 per payment, including ACH returns and recovery, chargebacks, check and money order processing, in-person payment handling, and reconciliation and back-office labor.

—The customer experience category represents the financial impact of payment friction and averages approximately $1.31 per payment, driven by delayed payment completion, payment abandonment and increased servicing burden.

PayNearMe explained the findings suggest that organizations may be significantly undercounting the true cost of payment acceptance because many payment-related costs are managed and measured outside of the payments function.

Delayed or incomplete payments, increased support needs and higher operational burden all contribute to the total cost of getting paid, yet are rarely viewed holistically, according to PayNearMe.

“Our research exposes a significant financial blind spot for many billing organizations,” PayNearMe chief revenue officer Mike Kaplan said in the news release. “When the true cost of payment acceptance is six times higher than what’s on your processor invoice, it becomes very clear that improving the payment experience is one of the most overlooked opportunities to improve cash flow and profitability.”

The Payment Experience Gap report combines PayNearMe operational benchmarks, third-party industry research and conservatively modeled assumptions to quantify the costs created by payment friction, support and operations across the payment journey.

The company said its methodology reflects a representative mid-market to enterprise lender processing approximately 500,000 payments annually, with an average payment size of $640. Those per-payment economics are then applied across the broader U.S. bill pay market, which includes 16.8 billion annual bill payments.

“Importantly, the analysis focuses on payment intent, acceptance and early-stage recovery activity. It does not attempt to quantify downstream collections or other costs associated with severe delinquency, making the findings intentionally conservative,” PayNearMe said.

PayNearMe went on to say that reducing the payment experience gap requires organizations to move beyond the transaction mindset and manage payments as an end-to-end journey.

PayNearMe called this payment experience management (PEM), a discipline its PayXM platform supports by automating and continuously improving the entire payment journey, from request through reconciliation.

The company highlighted the auto-specific proof points are strong.

PayNearMe has seen lenders measure meaningful operational improvements after changing the payment experience, including a 275% increase in autopay enrollment at First Texas Auto Credit, more than a 50% reduction in late payments at Automotive Partners Funding, and a 70% reduction in inbound calls at Northwoods Automotive.

“For years, businesses have optimized for the transaction, not the journey,” said Anne Hay, executive vice president and chief marketing officer at PayNearMe. “But transaction fees tell only part of the story. The next frontier of payments isn’t about cheaper processing. It’s about payment experience management; a new approach that transforms payments from a back-office cost center into an operational advantage.”

For more information, go to paynearme.com.