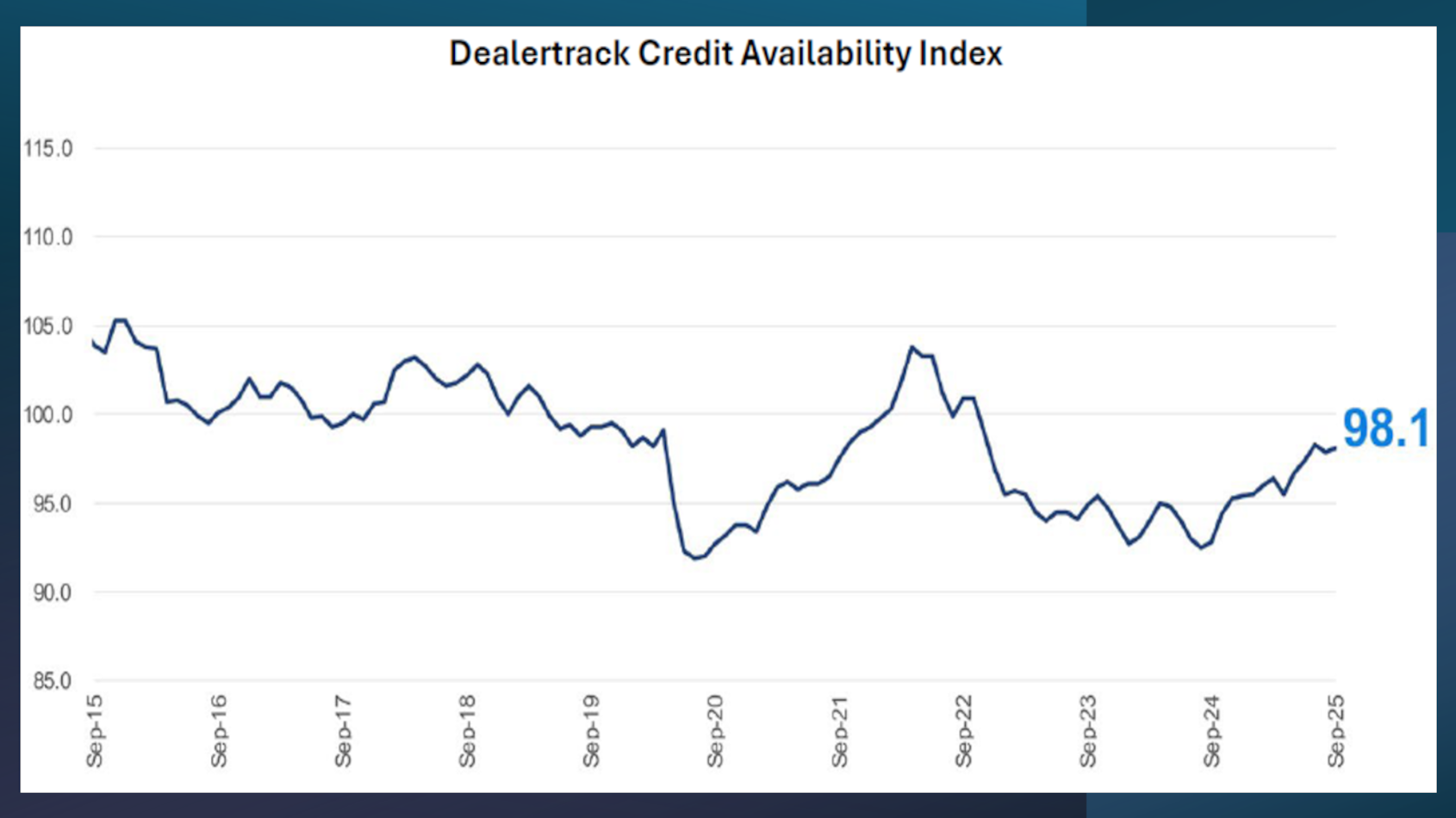

Auto credit availability improves slightly again in September

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Perhaps because of automotive market and general economic turbulence, there might be some tightening of underwriting by finance companies.

The Dealertrack Credit Availability Index showed that development has yet to come based on Cox Automotive data gathered in September.

The index continued its general upward trend of improved credit access after a slight tightening in August. The September index ticked up to 98.1 from 97.9.

Jonathan Gregory is a senior manager on Cox Automotive’s economic and industry insights team.

“Overall, the September Dealertrack Credit Availability Index reflected a return to loosening in auto credit conditions after a brief pause in August, influenced by the recent rate cut but reflecting still evolving economic signals and elevated loan performance risk,” Gregory wrote in an analysis that accompanied the index update.

“Consumers experienced slightly improved access to financing, particularly among subprime borrowers, but consumers paid for that improvement with higher rates,” he continued.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Cox Automotive indicated the approval rate for auto loans remained steady at 74.4% in September, but approvals rose 2.3 percentage points from September of last year.

“This stability at a high level reflects lenders’ confidence in borrower profiles and heightened competition for volume,” Gregory wrote.

The update pointed out that the share of loans to subprime borrowers increased by 60 basis points month-over-month in September, climbing from 13.6% to 14.2%. The latest share also is 170 basis points higher year-over-year.

“This suggests lenders are expanding access to higher-risk borrowers as overall credit loosens,” Gregory wrote.

What about the potential yield finance companies could be generating?

Cox Automotive calculated the yield spread widened by 38 basis points from 6.86 to 7.24, while the average contract rate rose by 25 basis points from 10.65% to 10.90%.

Analysts added the 5-year Treasury yield dipped by 13 basis points from 3.79% to 3.66%.

“This indicates lenders are offering slightly higher rates to compensate for higher risks as the cost of funds has fallen,” Gregory wrote.

A metric that made a notable move in September was contract terms.

Cox Automotive reported the share of loans with terms longer than 72 months jumped by 130 basis points in September from 25.5% to 26.8%. The number of contracts in that category is 200 basis points year-over-year, according to the update.

“This may reflect greater affordability pressures or lender flexibility on term length,” Gregory wrote.

Negative equity has generated a bit of negative attention so far this year, but the September trend didn’t alarm Cox Automotive.

Analysts determined the proportion of borrowers with negative equity rose by 50 basis points month-over-month and 60 basis points year-over-year.

“This signals some increase in risk but remains within historical norms,” Gregory wrote.

Meanwhile, Cox Automotive noticed that down payments softened a bit in September.

Analysts computed the average down payment percentage declined by 10 basis points last month. It’s also off by 50 basis points year-over-year.

“This may indicate increased consumer demand or lender flexibility,” Gregory wrote.

Gregory went on to mention credit availability among banks improved by 1.6% in September, “reflecting a strong appetite for growth and increased willingness to extend credit.”

But Gregory pointed out that captives tightened by 0.9% last month, indicating a more cautious approach.

He added, “Overall, lenders are showing more willingness to extend credit, with banks and finance companies driving the improvement.”

Gregory wrapped up his analysis with these observations.

“The continued improvement in credit access, especially in used and non-captive new vehicle segments, offers more financing opportunities,” Gregory wrote. “The drop in down payments and stable approval rates may enhance affordability. However, consumers should remain mindful of longer loan terms and slightly higher negative equity levels when evaluating loan offers.

“The mixed performance across lender types reflects varying risk appetites and strategic priorities,” he continued. “Finance companies, captives and banks appear to be expanding access, while credit unions are slightly more conservative. As credit conditions evolve, lenders must balance growth with prudent risk management, especially amid shifting rate environments and consumer behavior.”