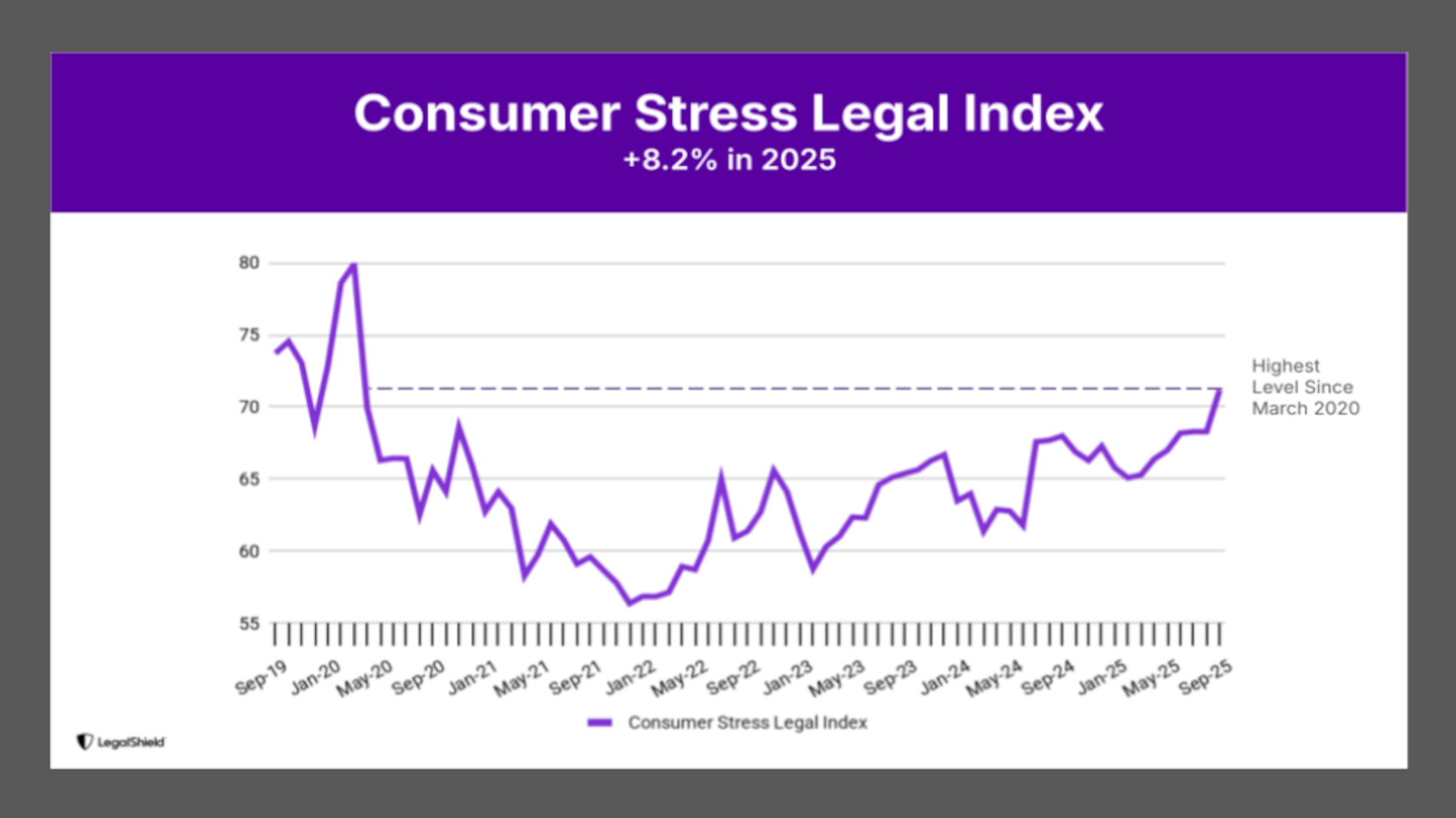

LegalShield Consumer Stress Legal Index hits highest point in more than 5 years

Chart courtesy of LegalShield.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Almost 400,000 individuals have already filed for bankruptcy during the first three quarters of this year.

And the newest LegalShield Consumer Stress Legal Index (CSLI) showed that trajectory might continue for the remainder of 2025 and beyond.

Consumer legal stress hit its highest level in nearly five-and-a-half years, driven by a 17% surge in bankruptcy inquiries to LegalShield’s network of provider lawyers during the third quarter.

The LegalShield Consumer Stress Legal Index (CSLI) rose to 71.2 in September from 68.2 in June. The index is now up 26.3% from its December 2021 post-COVID low of 56.4.

The index has climbed steadily for seven consecutive months, according to LegalShield.

LegalShield senior vice president of consumer analytics Matt Layton, who analyzes consumer legal trends across more than 36 million calls dating to 2002, said the timing of the surge is particularly concerning.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“We’re seeing families hit crisis mode heading into the holiday season,” Layton said in a news release. “The question now is whether this consumer legal stress translates into a pullback in spending in the final quarter of 2025.”

LegalShield’s data comes from more than 150,000 monthly calls to law firms across the country. Analysts said these real actions people take when facing financial and legal challenges, not surveys measuring sentiment.

Christopher Peoples is a LegalShield provider attorney in Kansas with Riling, Burkhead, & Nitcher. Peoples counsels dozens of families in financial distress each month, explaining debt issues are no longer confined to mortgages.

“We’re seeing a spike in bankruptcy-related calls here in Kansas,” Peoples said in the news release. “I’ve talked to my legal colleagues in other states like Utah and Idaho and they’re saying the same thing.

“People are drowning in this economic state we’re in — so much to pay for with prices constantly increasing and credit cards with exorbitant interest rates, everyday Americans are running out of options. Bankruptcy is their last lifeline,” Peoples went on to say.

According to the Federal Reserve, 4.4% of outstanding debt went delinquent as of June. That’s up 0.1 percentage point from the first quarter. The increase came primarily from delinquent mortgages, home equity lines of credit (HELOCs), and student loans, signaling growing financial pressure on American households.

This trend is reflected in LegalShield’s Q2 Foreclosure Index, which jumped 13.0% quarter-over-quarter and 28.9% year-over-year.

Property data firm ATTOM reported that foreclosure filings rose 11% in July compared to the previous month and 13% compared to July of the prior year.

August filings remained elevated, down just 1.1% from July but up 18.1% year-over-year, indicating sustained financial stress among homeowners, according to the news release.

Given that LegalShield’s bankruptcy data historically leads actual filings by two quarters, Layton predicted a difficult start to 2026.

“If the pattern holds, we’re likely to see a significant spike in actual bankruptcy filings in the first quarter of next year,” Layton said.