Fitch continues dialogue about affordability & delinquency with latest look at subprime auto securitizations

Charts courtesy of Fitch Ratings.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Affordability and delinquencies topped the latest Fitch Ratings report about auto loan asset-backed securitization performance, which weakened during the second half of 2025.

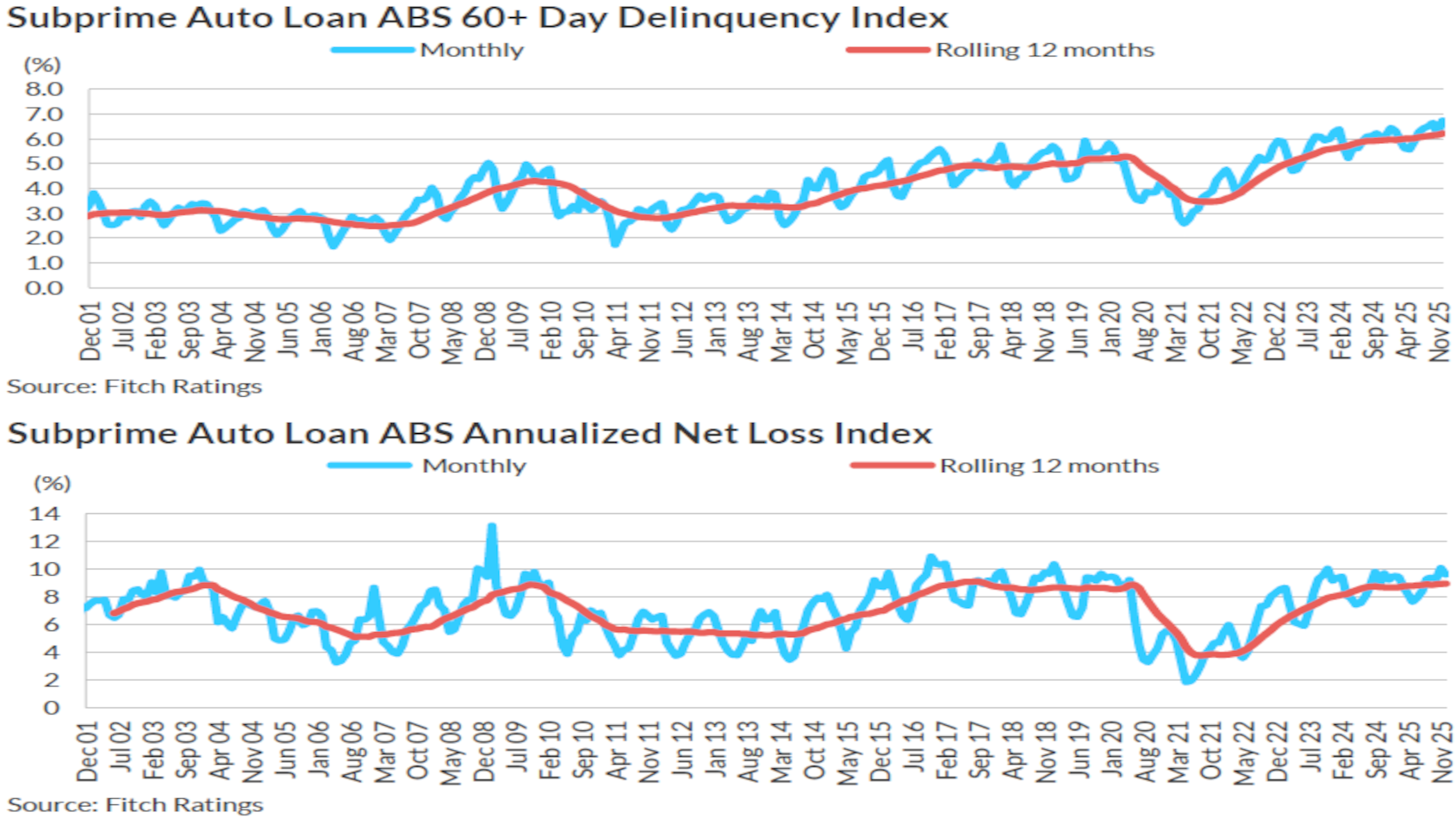

Along sharing more details about the subprime sector with Cherokee Media Group, Fitch determined that its 60-day delinquencies in the prime sphere rose to 0.43% at the close of last year. Meanwhile, the subprime reading for that level of delinquency reached 6.74% due to weaker 2022 and 2023 vintages.

“Annualized losses increased but less sharply than delinquencies, as some borrowers cycled in and out of delinquency,” Fitch said in a news release.

“Affordability remains the key pressure point in both prime and subprime auto,” analysts said. “Within prime, performance is bifurcated, with some platforms showing higher delinquencies and losses in recent vintages, while others are improving due to tighter underwriting.

“In subprime, newer vintages are improving more broadly, but are still performing worse than pre-pandemic cohorts, with deeper subprime facing more pressure,” Fitch added.

Through the report, analysts pointed out that subprime delinquencies have been steadily climbing since they sunk to a low point at 2.58% in May 2021 during the period of strong borrower performance induced by pandemic stimulus.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“The increase is driven by continued deterioration within the segment, along with composition shifts within the index, with stronger pre-pandemic and early-pandemic vintages paying off and being replaced by recent vintages,” Fitch said. “These recent vintages are performing slightly better than the stressed 2022 and 2023 vintages but worse than most pre-pandemic vintages.”

As a result, Fitch calculated annualized net losses in subprime ticked up to 9.63% at the close of 2025. That’s up from 9.23% registered at the end of 2024.

For context, this metric posted a pandemic-era low of 1.84% in May 2021, according to Fitch.

Analysts explained, “That said, the increase in losses appears to be slowing and does not proportionally match the increase in delinquencies, likely due to borrowers churning in delinquency.”

Meanwhile, Fitch noticed that recoveries continue to weaken, with its Subprime Recovery Index slipping to 32.86% in December 2025. That’s down from 35.25% a year earlier.

Analysts mentioned that while the movement is part of a post-pandemic downward trend, it is “partially due to a higher preponderance of older vehicles with higher mileage in subprime auto ABS transactions,” according to Fitch.

Amidst those trends, Fitch indicated that the issuance of subprime securitizations have remained stable with the segment generating approximately $41.5 billion in new issuance in 2025, slightly up from $38.7 billion in 2024.

For reference, Fitch noted that there was $43.3 billion in subprime securitizations in 2023.

What might happen this year?

“Fitch expects U.S. prime and subprime auto loan ABS performance to deteriorate in 2026 versus 2025 as macroeconomic headwinds, tariff uncertainty and a cooling labor market will continue to pressure affordability,” analysts said in the news release.

“Solid household balance sheets and healthy, but slowing, disposable income growth will be offset by inflation stress, especially for lower-income households. This trend reinforces the K-shaped recovery narrative,” Fitch went on to say.