Spring arrives with bump in Canadian wholesale market — but don’t expect it to last

Image courtesy of Canadian Black Book.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Spring has sprung in the Canadian wholesale used-vehicle market.

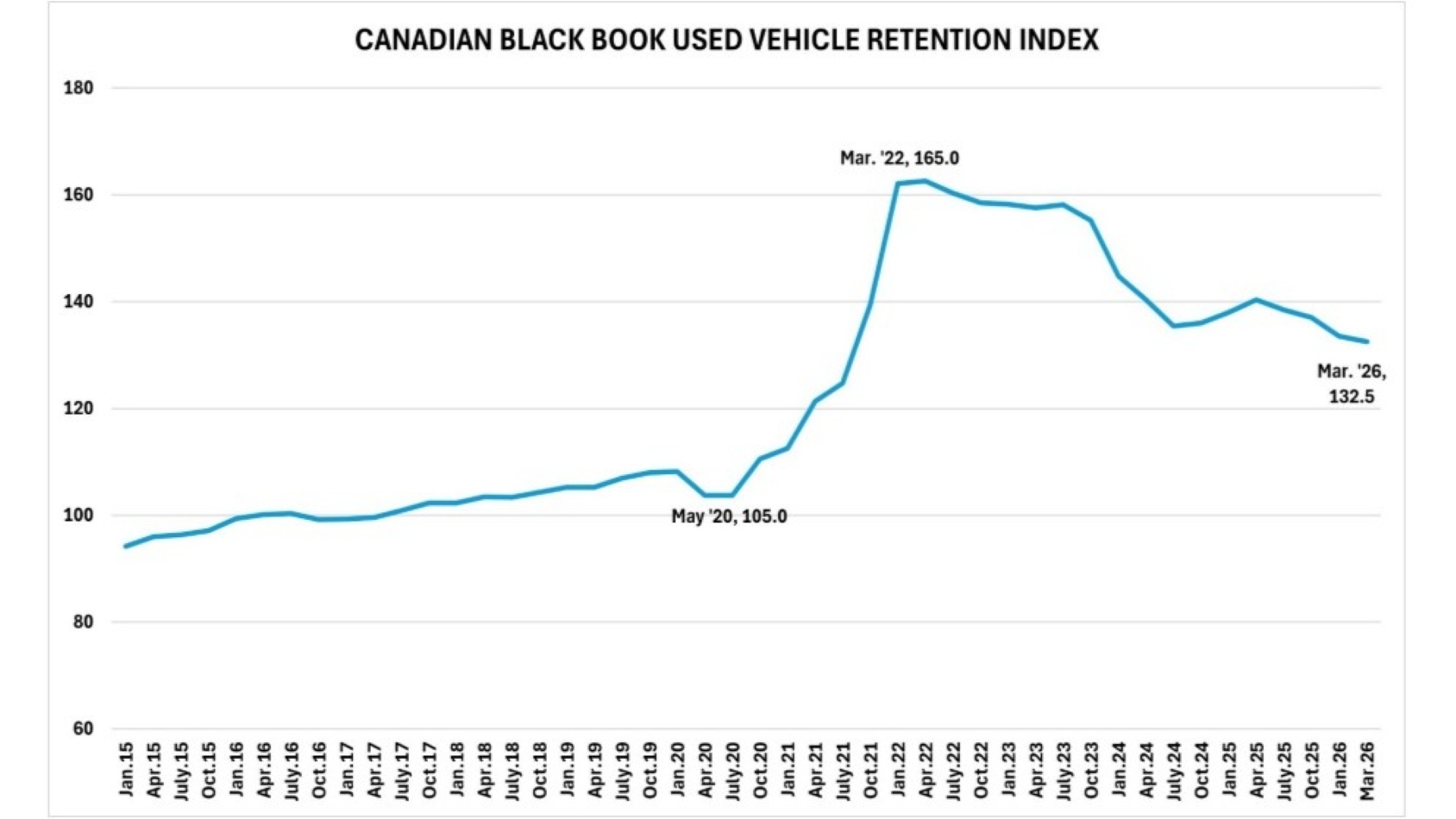

Canadian Black Book’s Used Vehicle Retention Index for March showed birds singing and flowers blooming in the form of a slight month-over-month increase to 132.5, up 0.3 points from February, a small bump that’s a clear sign of the seasonal market in action.

Just don’t expect it to last, CBB senior manager of industry insights and residual value strategy Daniel Ross said.

“There’s no denying a spring market,” he said. “When we see the prevailing trends of wholesale values pause for this seasonal positivity, there is an expectation of it lasting only for a limited time.”

Even with the rise, the index was still down more than 5% from March 2025 thanks to last year’s elevated prices and strong pull-ahead demand caused by threats of U.S. tariffs.

Ross said the current used wholesale environment is also showing how those tariffs continue to affect the Canadian market.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“What has transpired over the past 30 days for used vehicles mostly highlights the impact of the U.S. market,” he said. “While our overall retention measure is slightly positive, there is a distinct inflection point separating vehicle segments. So much so that mid- and full-size crossovers, along with pickup trucks, are the only vehicles seeing positive value trends last month.

“This stresses the impact of tariffs on used vehicles produced outside of the U.S., and the returning used-vehicle demand in that country, as American consumers digest high fuel prices (like us), but also the impact of tariffs on new vehicle pricing.”

The Canadian Black Book Used Vehicle Retention Index is calculated using CBB’s published wholesale average value on two to six-year-old used vehicles, as a percent of original typically equipped MSRP. It is weighted based on registration volume and adjusted for seasonality, vehicle age, mileage and condition.

For now, the spring feel is real. According to CBB’s weekly Market Insights report for the week ending April 4, the new month began with an overall decline of just 0.06%, though it was the car segments showing the more solid performance with a break-even week.

Sporty cars (up 0.58%, $151) and premium sporty cars (0.28%, $228) led the gainers, joined in the car category by full-size cars (up 0.29%, $53). Among truck/SUV segments, Ross’ usual suspects — mid-size crossover/SUVs (0.22%, $52), full-size crossover/SUVs (0.13%, $50) and full-size pickups (0.21%, $71) were the only ones in plus territory.

Midsize cars showed the largest percentage decline at 0.86% ($142), while prestige luxury cars took the biggest dollar loss at $172 (0.30%). Three truck/SUV segments dropped more than $100, led by minivans ($146, 0.64%).

Monitored auction sale rates showed greater strength and stability, averaging 53.7% and ranging from 25.9% to 69.6%, just a week after the average dropped to 31.1% with a high of just 42.7%. Used retail prices held steady at $37,300.