Point Predictive gives 10 recommendations as projected fraud exposure surpasses $10B

Graphic courtesy of Point Predictive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

A portion of Point Predictive’s latest Fraud Intelligence Brief examined how much fraud is happening at dealerships and why lenders are watching the issue even more.

Point Predictive said its consortium data — which comes from 307 million applications, $5 trillion in scored value, and 105 million unique consumers — showed more than 400 dealerships are currently operating what the firm deemed to be “extreme risk conditions.”

Point Predictive also said 255 different dealerships reported more than 50 confirmed fraud incidents in the past year, with each one averaging $45,000 in losses, putting those dealers on track to absorb as much as $2.25 million in fraud exposure annually.

“These dealers … are frequent targets of organized fraud rings submitting loans that default at alarming rates,” Point Predictive said in its report. “For lenders still funding deals through these locations, the risk compounds quickly. Fraudulent loans originated at these stores carry higher default rates, trigger costly buyback demands, and erode the profitability of entire portfolios.

“Many of these dealerships have been flagged repeatedly, yet continue to process high volumes of applications with minimal verification. Without proactive monitoring and intervention, both dealers and lenders remain exposed to losses that are entirely preventable,” Point Predictive continued.

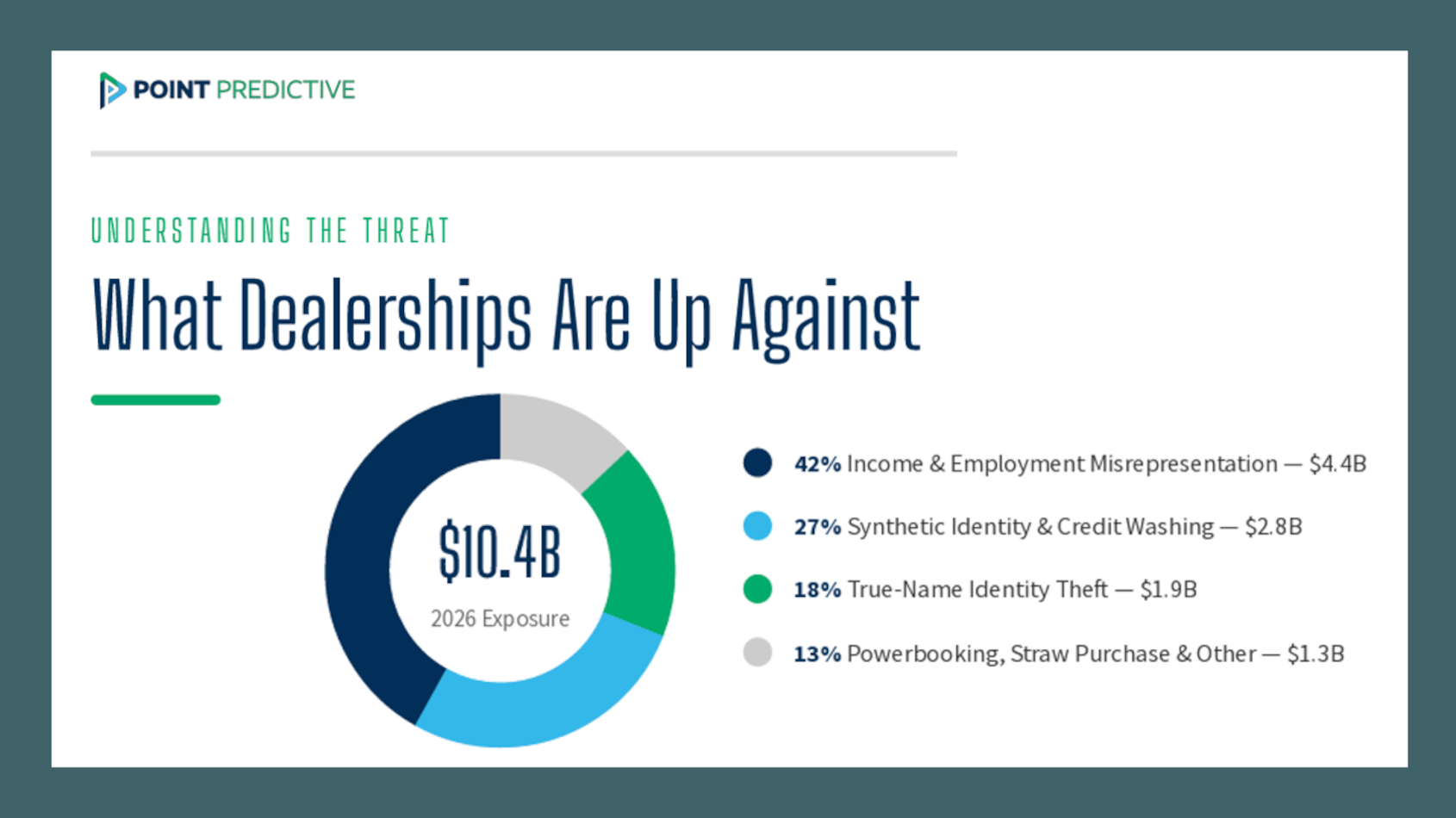

In 2023, Point Predictive estimated that auto lenders faced $7.9 billion in fraud and misrepresentation exposure. By 2024, that figure climbed to $9.2 billion. Going into 2026, Point Predictive projected exposure will exceed $10.4 billion.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“For years, dealers viewed fraud as a lender problem. If a loan went bad, the lender absorbed the loss. That’s no longer true. When fraud is discovered after funding — and it’s being discovered more often thanks to improved analytics — lenders push the losses back to the dealership through buyback clauses,” Point Predictive said in the report.

According to a Point Predictive survey of more than 35 auto finance companies, 60% now require dealers to buy back fraudulent and early payment-default loans. Only 15% of lenders never require buybacks.

“One dealership reported close to $500,000 in repurchase demands in just six months — after never experiencing a single buyback in the prior history of the business,” Point Predictive said. “The dealer is left holding the full value of the loan, responsible for repossession, and at risk of losing the lender relationship entirely.

“The reputational damage with lending partners can be even more costly — elevated fraud metrics trigger additional stipulations, unfavorable pricing, and ultimately terminated relationships,” Point Predictive said.

Before store managers just throw up their hands in complete frustration, Point Predictive made 10 suggestions to help reduce fraud exposure and keep the relationship of dealerships with finance companies on better footing. They included:

- Scan every ID forensically: Use a scanner that checks the barcode, tests for forgeries, and screens against fraud databases. Don’t rely on visual inspection.

- Stop trusting paper paystubs: One in five paystubs submitted with auto loans is fake, according to Point Predictive. Generators cost $10 online. Use automated income verification.

- Replace KBA With OTP verification: Knowledge-based questions are easily answered using dark web data. One-time passcode confirms phone possession.

- Screen every deal, including prime: High credit scores don’t mean low fraud risk. Point Predictive said credit washing jumped 162% in 2024. Run screening on every customer.

- Audit deal jackets before submission: Missing signatures and compliance errors trigger buybacks and funding delays. Catch problems before the lender does.

- Train the team quarterly: Annual training isn’t enough when new scams emerge monthly. Document all training to prove due diligence.

- Monitor fraud metrics: Track EPD rates, buyback causes, and rejection rates monthly by store and F&I manager. See problems first.

- Update the Red Flags program: The FTC Red Flags Rule requires an identity theft prevention program. Penalties can run up to $11,000 per violation, per day.

- Lock down data security: The FTC Safeguards Rule requires encryption, MFA, and vendor oversight. Penalties can reach $51,744 per violation.

- Screen everyone against OFAC: Buyers, co-signers, and trade-in sellers on every transaction. Strict liability with penalties up to $1.5 million.

Point Predictive chief innovation officer Frank McKenna closed an industry letter at the beginning of the brief by saying, “The dealerships that will be best positioned in 2026 are the ones verifying every deal now.”