Records set in Edmunds Q1 data reinforce thought of ‘cliff’ connected to 84-month contracts

Chart courtesy of Edmunds.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

AutoPayPlus recently surveyed 2,000 automotive dealers and F&I executives who fear a growing “84-month trade-in cliff,” removing customers from the purchase cycle for too long and threatening future sales volume and dealer profitability.

Well, first-quarter data about new-car financing from Edmunds showed how real that “cliff” likely is.

Analysts determined extended contract terms reached a record high, underscoring buyers’ growing reliance on longer loans to manage monthly costs.

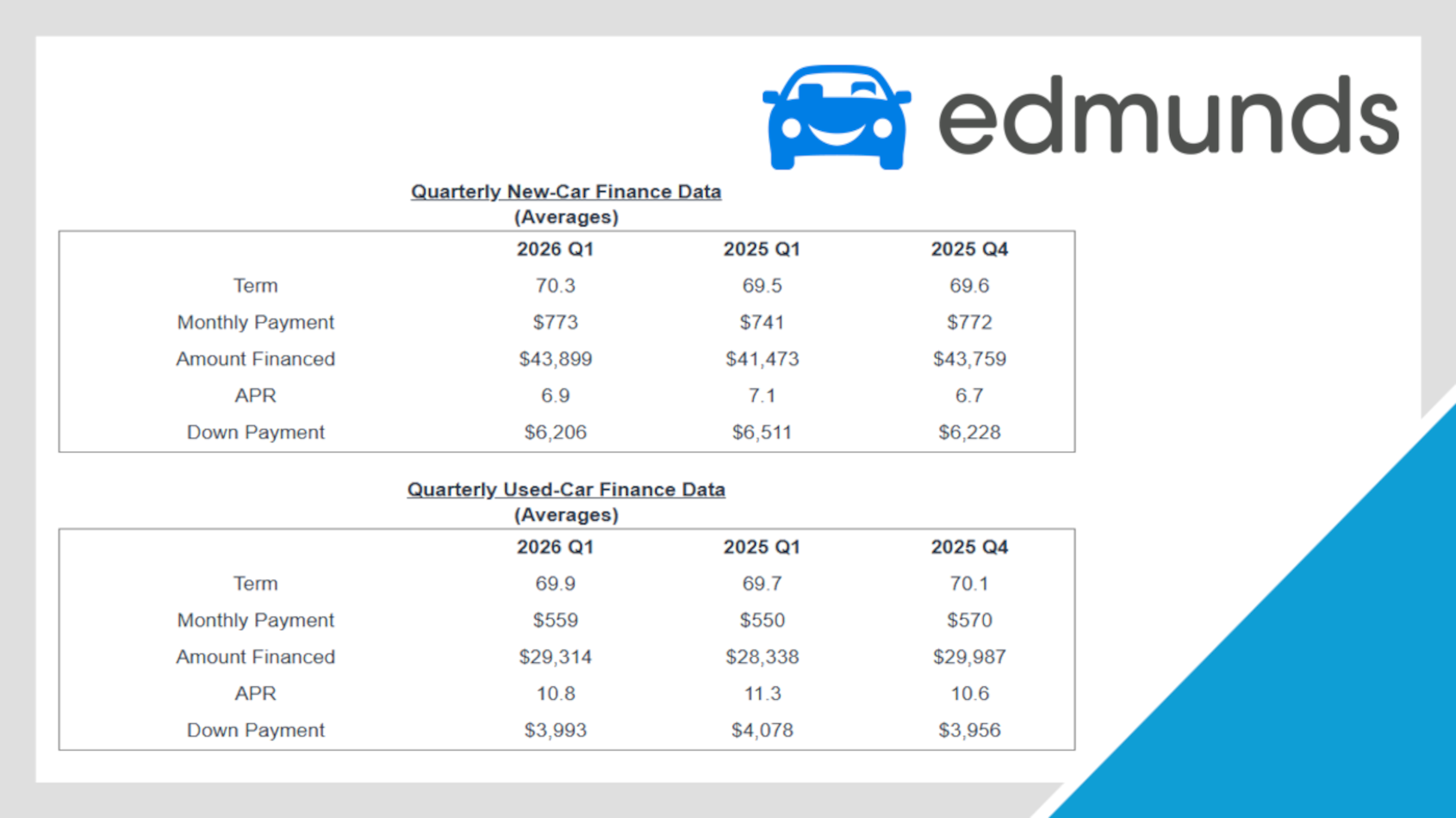

Edmunds data showed that 84-month or longer contracts made up 22.9% of financed new-car purchases in Q1, which is an all-time high. That level is up from 20.8% in Q4 2025 and 21.2% in Q1 2025.

“Q1 financing data shows that car buyers are getting creative just to keep their purchases within reach,” said Edmunds head of insights Jessica Caldwell, who is among the recipients of the 2026 Automotive Intelligence Awards.

“As loan amounts and monthly payments continue to climb to record levels, consumers are having to work harder to make the numbers fit — a clear sign of how strained affordability has become,” Caldwell continued in a news release.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

And the total amount consumers are financing for a new car and the monthly payments they’re accepting are also at record highs, according to Edmunds tracking. Here are those details:

—Consumers are financing more than ever to buy new vehicles. The average amount financed for new vehicles climbed to a record high of $43,899 in Q1, compared to $43,759 in Q4 2025 and $41,473 in Q1 2025.

—Monthly payments for new vehicles also reached a new all-time high. The average monthly payment on financed new-vehicle purchases rose to $773 in Q1 2026, edging past $772 in Q4 2025 and up from $741 a year ago.

—Monthly payments of $1,000 or more remain persistently high. The share of new-car buyers committing to monthly payments of $1,000 or more accounted for 20% of all financed new-vehicle purchases in Q1, nearly flat from 20.3% in Q4 2025 but up from 17.7% in Q1 2025.

—Buyers are putting less money down to manage upfront costs. The average down payment for new-vehicle deliveries fell to $6,206 in Q1 — one of the lowest first-quarter levels since 2022 — compared to $6,228 in Q4 2025 and $6,511 in Q1 2025.

What about the used-car financing market?

Well, Edmunds reported that 5.3% of used-vehicle buyers committed to monthly payments $1,000 during the first quarter. That’s down from 6.3% in Q4 2025 but up from 4.9% a year ago.

Edmunds analysts explained affordability considerations are clearly playing out in how buyers are structuring their financing.

“Right now, consumers are picking their battles when it comes to affordability,” Edmunds director of insights Ivan Drury said in the news release. “While a larger down payment is typically the better financial move, many buyers simply don’t have that flexibility in today’s market, especially if it means diverting funds away from more immediate needs.

“In those cases, extending the loan term can help achieve a similar monthly payment, but it often comes with higher long-term costs and added financial risk,” Drury continued.

As affordability challenges persist, Drury pointed out some shoppers may find more viable options outside the new-car market.

“For shoppers who are struggling to make the numbers work on a new vehicle, the used market could offer more opportunity in the months ahead,” Drury said. “As more off-lease vehicles return to the market, we expect inventory to improve, which could help ease pricing and give buyers more flexibility.”