From the editor: Fed’s in-depth examination into BHPH shows how much Tricolor downfall alarmed banking world

Chart courtesy of the Federal Reserve.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Last year’s bankruptcy filing by Tricolor Holdings and subsequent federal fraud charges levied against former chief executive officer Daniel Chu prompted five financial experts at the Federal Reserve to do extensive research to learn about how the buy-here, pay-here dealership segment functions.

While their resulting report perhaps didn’t reveal anything that operators didn’t already know, the fact that the Fed expended this much energy and effort to examine the BHPH segment reinforces how much the impact Tricolor’s downfall had on the banking community.

That might be especially apparent since Chase and Fifth Third Bank were allegedly two of the institutions that sustained the most losses from Tricolor’s alleged fraud scheme.

In the opening of their report, Subprime Auto Lending: Trends in Buy Here Pay Here Auto Lending, authors Olena Chyruk, David Cox, Lily Liu, James Wang, and Stephen Zoulalian wrote they wanted to know “what distinguishes BHPH auto dealers from traditional auto finance, examining their customer profile, risk mitigation strategies, and their bank funding sources to better understand the risks of this increasingly scrutinized, high-risk sector.”

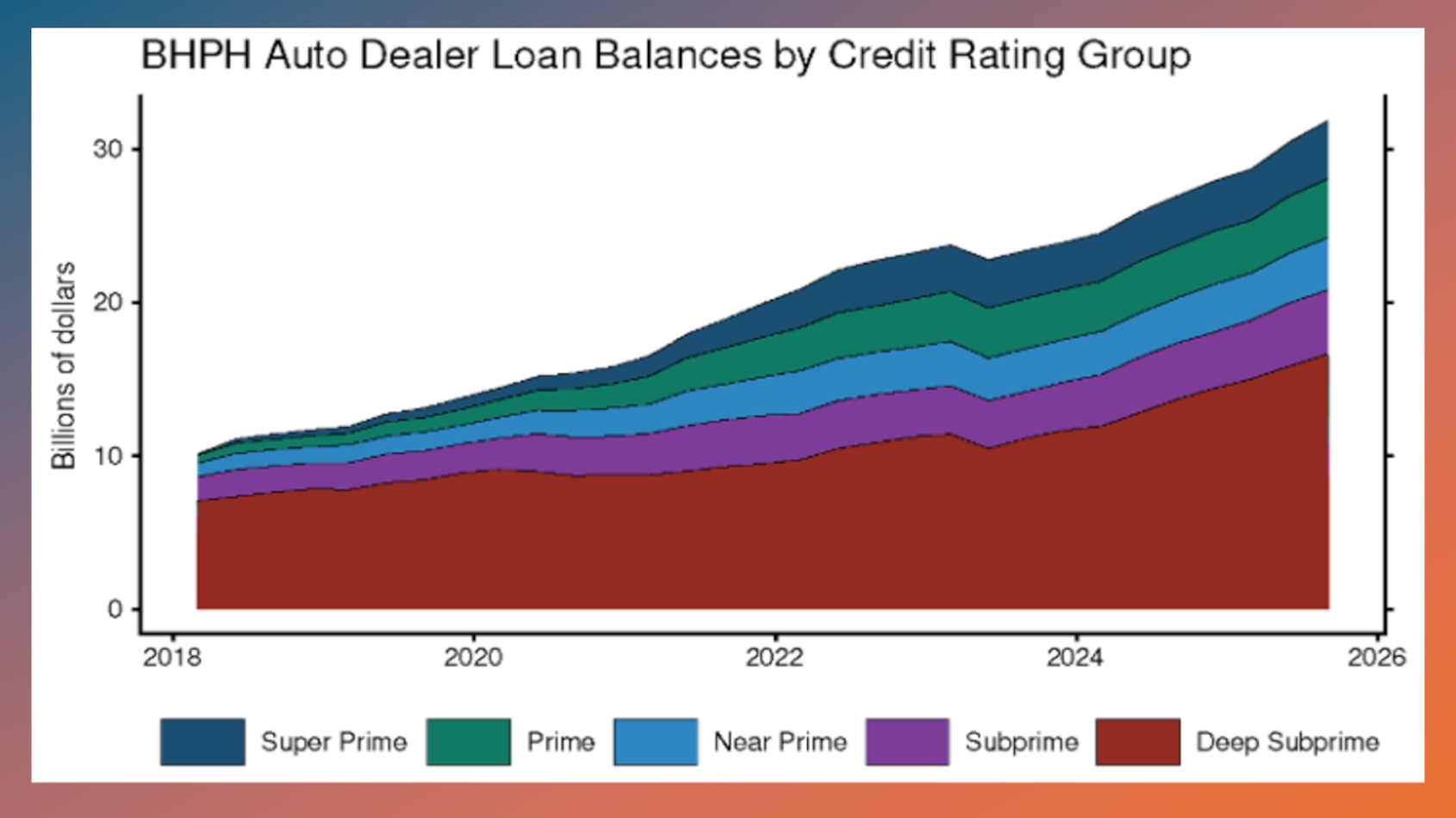

After delving into data from Equifax and other sources at the Fed’s disposal, the report orchestrators found that BHPH dealers have moved to less risky consumer segments, reducing their share of deep subprime customers from 70% of their portfolios in 2018 to slightly above 50% of their outstanding contracts in 2025.

The Fed experts also identified that larges banks are a major source of funding for BHPH dealers.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“Despite banks being historically cautious toward subprime consumer lending, our results find that banks have indirect exposure to this high-risk sector through inventory and loan receivable-based lending,” Chyruk, Cox, Liu, Wang, and Zoulalian wrote. “While our name-match process is not intended as a full inventory of funding to BHPH auto dealers, we document that the more than $2 billion in loan commitments that we identify were rated by these large banks as being of lower risk compared to loans to traditional auto dealers.

“We attribute the loans’ lower perceived risk partly to structural protections that banks build in, such as lower loan advance rates resulting in over-collateralization, to mitigate the higher risk profile of the underlying BHPH vehicle loans,” they added.

The bulk of the report delved into more data points the Fed found, including the average amount financed ($15,402), term (55 months) and weighted interest rate (25.39%).

Someone not in the car business might have looked at the report and been astonished when those metrics were compared to overall readings the Fed noted. But the report authors acknowledged that the overall data also included prime and super-prime consumers who financed both new- and used-vehicles and can procure better rates and other incentives.

Finding a new model delivered via a BHPH contract might be as rare as me passing up a second helping of my wife’s delicious Thanksgiving dinner.

The conclusion of the Fed’s report might be the most encouraging part of the entire project for BHPH operators who are navigating the current environment of more expensive vehicles and customers who are being stretched even more thin by higher gas and food prices.

“By matching BHPH auto dealers with corporate obligor names in regulatory data, we find that large banks maintain direct exposure to this sector through corporate lending,” Chyruk, Cox, Liu, Wang, and Zoulalian wrote. “Notably, these loan commitments show lower probabilities of default and lower loss given default compared to loans to traditional auto dealers, which we attribute to more structural protections, such as loan guarantees, over-collateralization, the use of special purpose entities (SPEs), and BHPH auto dealers’ advantages in vehicle repossessions.

“At the same time, bank ratings of BHPH credit quality have deteriorated over the last few years, including immediately after the Tricolor bankruptcy, suggesting BHPH’s risk differential may not be permanent as banks re-adjust their outlook of BHPH auto dealers,” they continued. “As the sector continues evolving post-Tricolor, our findings highlight the importance of understanding this unique business model, as well as the need for continued monitoring of both consumer-level risks and the interconnections between BHPH dealers and the banking system.”

Learning how a business functions before jumping to conclusions. How refreshing is that?

Nick Zulovich is senior editor with Cherokee Media Group and can be reached at [email protected].