3 segments potentially ripe for auto refinancing

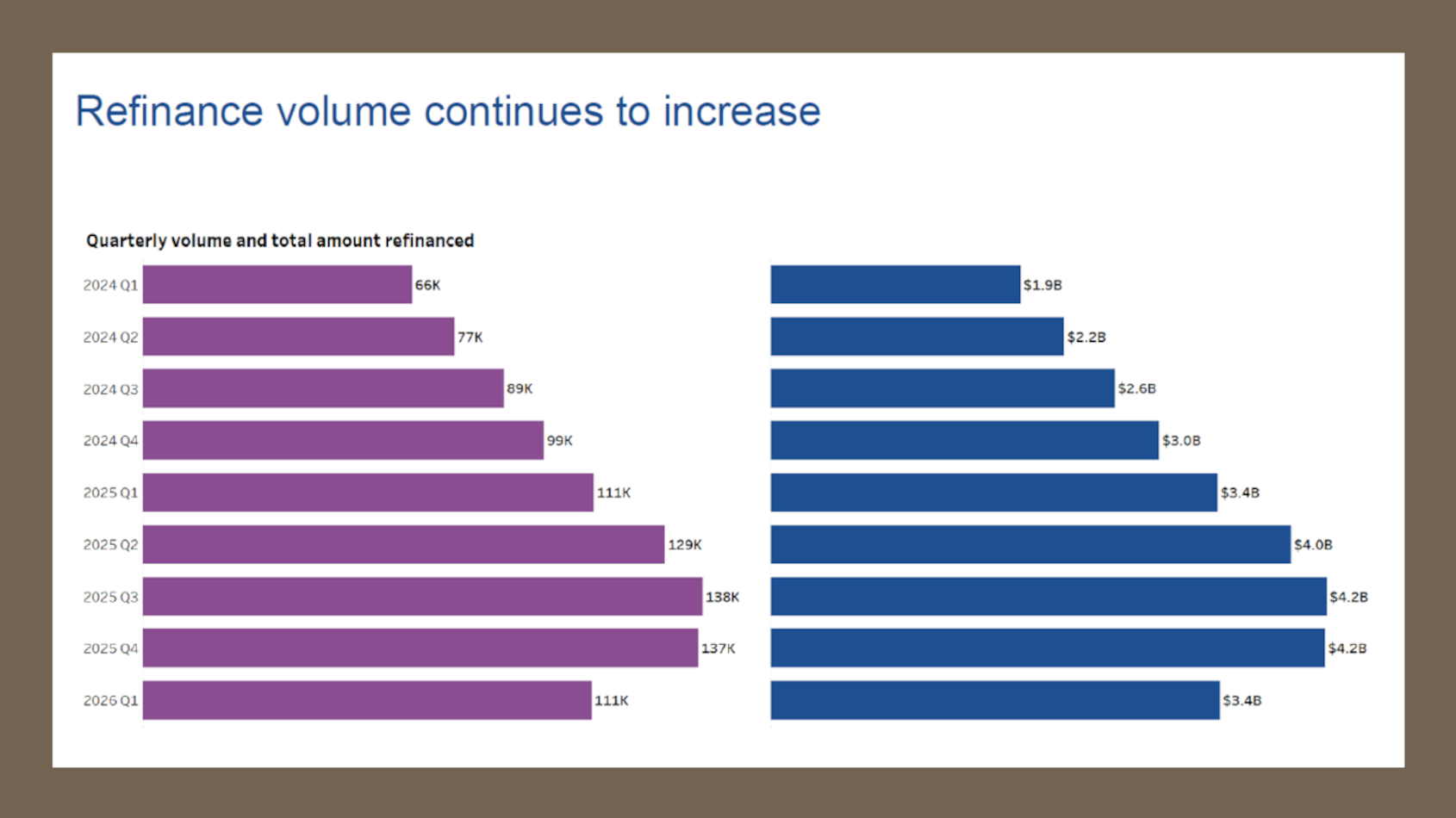

Chart courtesy of Experian.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

According to Experian’s State of the Automotive Finance Market Report: Q1 2026, the industry has generated at least 111,000 refinanced contracts during each of the past five quarters.

And iLending sees the prospect for future refinancing volume might be even more robust.

Based on current conditions highlighted in its State of the Auto Refinance Industry, iLending said the opportunity to benefit from auto refinancing is:

—Strong for near-prime and sub-prime borrowers with improved credit and stable payment history

—Moderate to strong for prime borrowers seeking payment flexibility and monthly savings

—Time-sensitive for loans originated during peak pricing and interest rate periods

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“Vehicle values are behaving differently than many expected,” iLending president Nick Goraczkowski said in a news release. “We’re seeing pockets of strength that are creating opportunity but also reinforcing how quickly conditions can change.”

Experian reported that the average time into contract terms when the consumer completed refinancing during the first quarter was 26.41 months. That’s on par with the past five quarters of activity previously mentioned.

Experian also said 50.53% of the Q1 refinancing was connected with consumers in the prime credit tier, with 12.08% falling in subprime and 18.98% in near prime.

As the economy moves through 2026, iLending explained the landscape is defined by a mix of moderating but fluctuating inflation, elevated borrowing costs relative to pre-pandemic norms, and continued pressure on household budgets.

In this environment, iLending said auto loan refinancing remains one of the most immediate and practical tools available to consumers seeking financial flexibility.

“Consumers are no longer waiting for relief, they’re creating it,” iLending vice president of marketing Chad Nordhagen said in the news release. “Refinancing is one of the fastest ways to improve cash flow without sacrificing mobility. In today’s environment, that matters more than ever.”

And according to Experian tracking, credit unions are doing most of the refinancing, with 63.43% of the Q1 volume being completed by those institutions. Experian added that credit unions have booked at least 60% of the refinancing volume during each of the past five quarters.

Banks have completed at least 20% of the refinancing volumes during each of the past nine quarters, Experian reported.

“Lender appetite has improved entering 2026, particularly for borrowers with strong credit profiles and consistent payment histories. However, underwriting standards remain disciplined, with heightened emphasis on credit quality and loan performance metrics,” iLending said.

“Opportunities remain strongest for borrowers who have improved their credit, maintained stability, and can demonstrate responsible payment behavior. Lenders continue to introduce targeted programs focused on payment flexibility and affordability,” iLending went on to say.