Auto defaults now at lowest point in 10 years

Graphic courtesy of S&P Dow Jones Indices.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

NEW YORK –

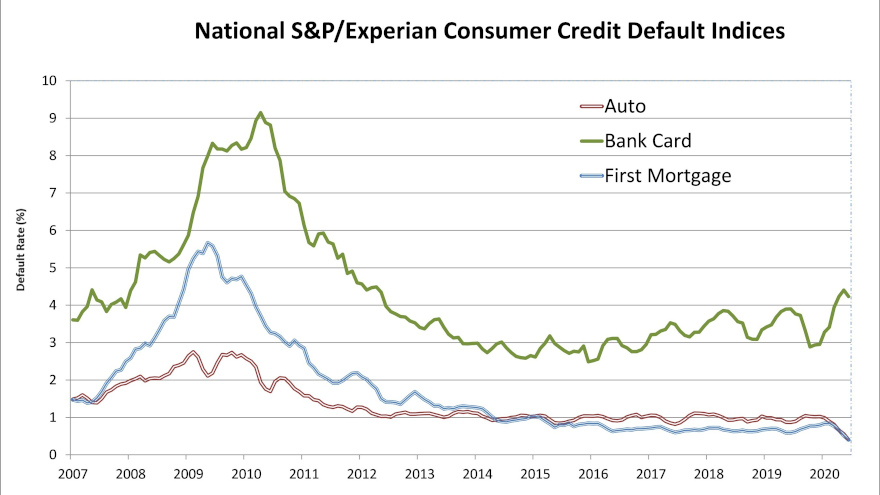

For what it’s worth amid so much uncertainty nowadays triggered by the coronavirus pandemic, auto-finance defaults are at the lowest point recorded by S&P Dow Jones Indices and Experian going back 10 years.

According the data through June released on Tuesday morning, the auto portion of the S&P/Experian Consumer Credit Default Indices dropped 16 basis points to come in at 0.40%; a reading less than half of what it was back in January.

For context, here is where the auto-default reading has stood at the year’s midpoint since 2010:

2019: 0.87%

2018: 0.93%

2017: 0.82%

2016: 0.91%

2015: 0.85%

2014: 0.96%

2013: 1.00%

2012: 1.04%

2011: 1.29%

2010: 1.70%

It’s highly likely the newest default reading is so low because of how many contracts have been modified by finance companies for consumers who have been impacted financially by the pandemic. Both Kroll Bond Rating Agency (KBRA) and S&P Global Ratings discussed their finding on that topic that SubPrime Auto Finance News recapped in this report.

Turning back to defaults, analysts found the composite rate of the S&P/Experian Consumer Credit Default Indices that represent a comprehensive measure of changes in consumer credit defaults declined 12 basis points in June to settle at 0.66%.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Analysts went on to mention the bank-card default rate fell 17 basis points to 4.23%, and the first mortgage default rate decreased 11 basis points to 0.41%.

Looking at the June data within the five largest metropolitan areas, the S&P/Experian Consumer Credit Default Indices indicated four of the cities posted sequential declines in June.

Chicago generated the largest decrease, dropping 14 basis points to 0.69%. Dallas was right behind, falling 13 basis points to land at 0.66%, while New York dropped 9 basis points to settle at 0.74%.

Analysts said Miami came in 3 basis points lower to register at 1.40% in June. However, they pointed out that Los Angeles went in reverse as its rate edged 2 basis points higher to 0.72%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.