CFPB’s Ficklin Maintains Agency’s Target on Dealer Participation

Patrice Ficklin is assistant director of the office of fair lending and equal opportunity at the Consumer Financial Protection Bureau.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

NEW ORLEANS –

The Consumer Financial Protection Bureau reiterated its uneasy assessment of how the dealer participation system operates when one of the agency's top officials made prepared remarks and answered a handful of submitted questions during the American Financial Services Association's Vehicle Finance Conference on Thursday.

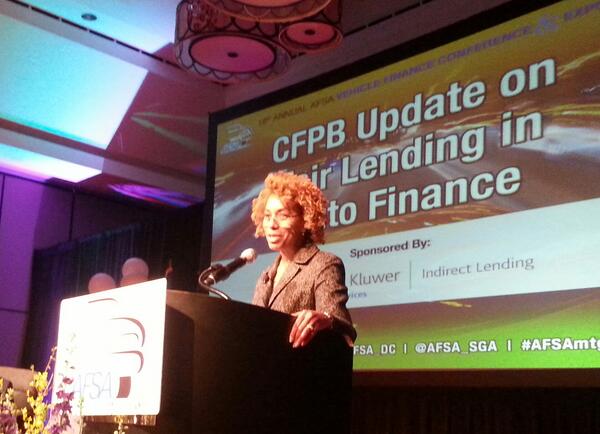

Patrice Ficklin spoke to a spillover gathering of more than 600 finance company executives, service providers and dealers about the bureau's concerns regarding how F&I managers can mark up a sales contract after the sales price, trade-in value and lender buy rates are all established.

Ficklin, the bureau's assistant director of the office of fair lending and equal opportunity, said that dealers should be compensated for arranging vehicle financing, better known as indirect lending. But Ficklin stressed that other avenues should be pursued, including finance companies switching to flat fees to compensate dealers rather than allowing stores to mark up contracts anywhere from 100 to 200 basis points.

"We have been approached by lenders about the types of compensation systems that will be acceptable to the bureau," Ficklin said in prepared remarks that lasted close to 30 minutes. "The answers really depend on the specifics of each lender's business. But we believe one factor to consider in term of evaluating compensation systems is that compensation be based on non-discriminatory terms rather than terms that require discretion to modify.

"As we've indicated, it's been our experience that permitting discretion and tying compensation to the exercise of that discretion often significantly increases fair-lending risk," she continued. "Potential alternative compensation systems could vary in design and sophistication, depending the needs of the individual lender's business."

Much of Ficklin's prepared remarks also recapped the settlement the CFPB recently reached with Ally Financial, a package of enforcement actions that included $98 million in penalties and instruction on how the company should revamp its compliance department to prevent future alleged discriminatory activities.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Following her prepared remarks, AFSA president and chief executive officer Chris Stinebert whittled down a stack of submitted questions written on index cards from attendees. Stinebert asked if the bureau's goal is to eliminate discretion altogether or to make sure it's exercised under certain parameters. Ficklin responded by citing the Equal Credit Opportunity Act.

"You raise an important point that ECOA does not outlaw discretion," Ficklin said. "There are situations where discretion can be valuable. There are times where individual determinations might be valuable to the borrower. But we don't have a specific system to tell you what you should do."

In closing the hour-long panel session that was one of the highlights of AFSA's annual gathering ahead of the National Automobile Dealers Association Convention & Expo, Ficklin again reiterated four elements as to how a finance company can organize a compliance department to ensure dealerships are not being discriminatory.

Those four points first came from the bureau last March when it released its guidance on auto financing.

"Those four components are the bureau's position as well as the Department of Justice's position about what are the essential elements of appropriate compliance," Ficklin said.

The bureau official also made reference to a concern AFSA is looking to address in a year-long study that's being orchestrated beginning this month. Ficklin maintained that much of what drive bureau action is data.

"I will say that while we've certainly heard the assertion that consumers pay less in an indirect scenario, we have still not seen solid studies showing that. And we would welcome that. That's something of interest to the bureau more broadly," Ficklin said.

"But the specific area we're focused on right now is the fair lending risk created by the discretion and the markup policies," she went on to say.