Edmunds pinpoints top 20 trades with negative equity in Q2

Graphic created with Edmunds data using Nano Banana 2.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Individuals holding thousands of dollars in negative equity with their trade might not necessarily be pushed into the special finance or subprime departments at dealerships and lenders.

But the record-setting negative equity data Edmunds shared on Thursday might very well be complicating the processes of getting paper bought and deliveries completed.

Edmunds said nearly three in 10 trade-ins toward new vehicles in the second quarter were in an underwater position, the highest Q2 figure since 2020.

Analysts found that 29.6% of trade-ins toward new-vehicle purchases had negative equity in Q2. This is a slight decrease from the 30.9% share recorded in Q1 but represents an increase from 26.6% in Q2 2025 and is the highest Q2 mark since 2020 when it was 37.2%.

Edmunds also indicated the average amount owed on upside-down loans hit a record high for the second quarter of a calendar year. The average negative equity amount in Q2 came in at $6,884, the highest for a second quarter on record, compared to $7,183 last quarter and $6,754 in Q2 2025.

And here’s where it could be even more complicated to get the deal funded and the car over the curb.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Edmunds pointed out that climbing negative equity is leading to record average monthly payments and interest costs.

Analysts calculated the average monthly payment for a new-vehicle loan with negative equity on the trade-in reached $944 in Q2, the highest figure Edmunds has on record and $167 more than the industry average of $777 in Q2.

Edmunds explained buyers rolling negative equity into a new loan are projected to pay an average of $16,270 in interest over the life of that contract, another all-time high and nearly $6,500 more than the $9,811 paid by the average new-vehicle buyer in Q2 this year.

What’s fueling all these deal headwinds?

Edmunds also noticed the average age of underwater trade-ins inched up to a Q2 record.

The average trade-in age of vehicles with negative equity reached a Q2 record of 4.0 years this past quarter, up from 3.8 years in Q2 2025 though down from 4.3 years last quarter.

Analysts note this aligns with vehicle purchases made in 2022, a period characterized by limited inventory, minimal incentives, and transactions at or above MSRP, which set the stage for current long-term negative equity positions.

“Consumers are incurring more debt than ever when trading in vehicles that are underwater,” Edmunds’ head of insights Jessica Caldwell said in a news release. “Buyers who financed at 2022’s peak prices are starting to come back to trade in, and they’re bringing thousands of dollars in old debt with them. With interest rates still elevated, this is creating a costly snowball effect for consumers.

“As buyers roll over their negative equity, their new loan principals swell. Relying on longer loan terms as a coping mechanism to keep monthly payments down only causes total interest charges to be higher in the long run,” Caldwell added.

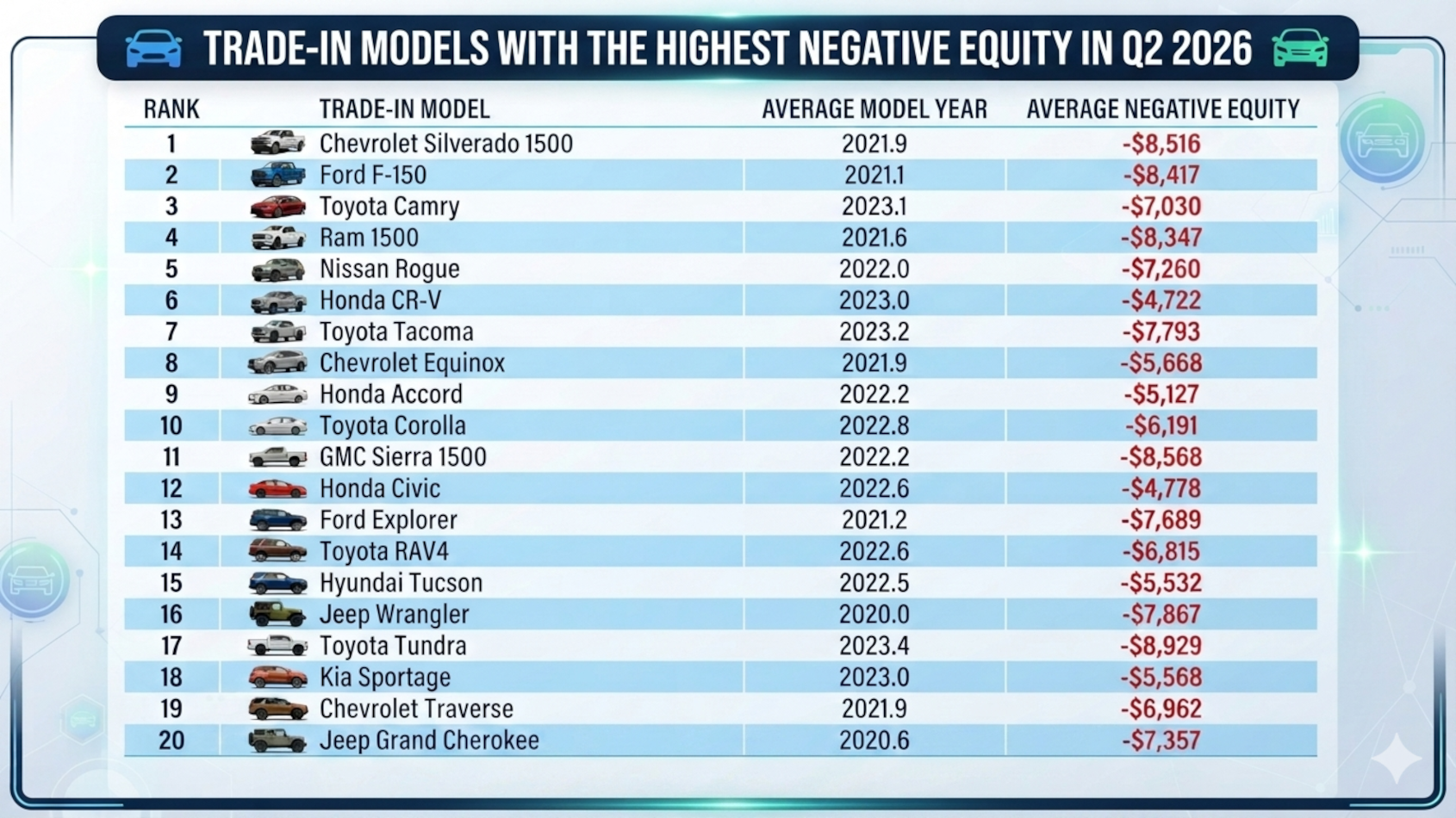

Edmunds analysts also researched models holding the highest amounts of negative equity as trade-ins in Q2.

Their findings revealed that even highly regarded vehicles known for holding their resale value are not immune to financing challenges. The list features popular trucks and SUVs, alongside traditional residual winners.

“It’s easy to assume negative equity is just a story about vehicles that depreciate quickly, but some of the biggest dollar losses we’re seeing are on trucks and sedans that traditionally hold their value better than most,” Edmunds’ director of insights Ivan Drury said. “When historically safe residual value bets are showing up underwater, it’s clear this is a financing problem, not always a vehicle choice problem.

“These examples are a harsh reminder that a great vehicle choice can still be completely undermined by a punishing loan structure,” Drury went on to say.