Experian: Subprime financing originated during a Q4 climbs to highest level in four years

Chart courtesy of Experian Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Call it the subprime surge.

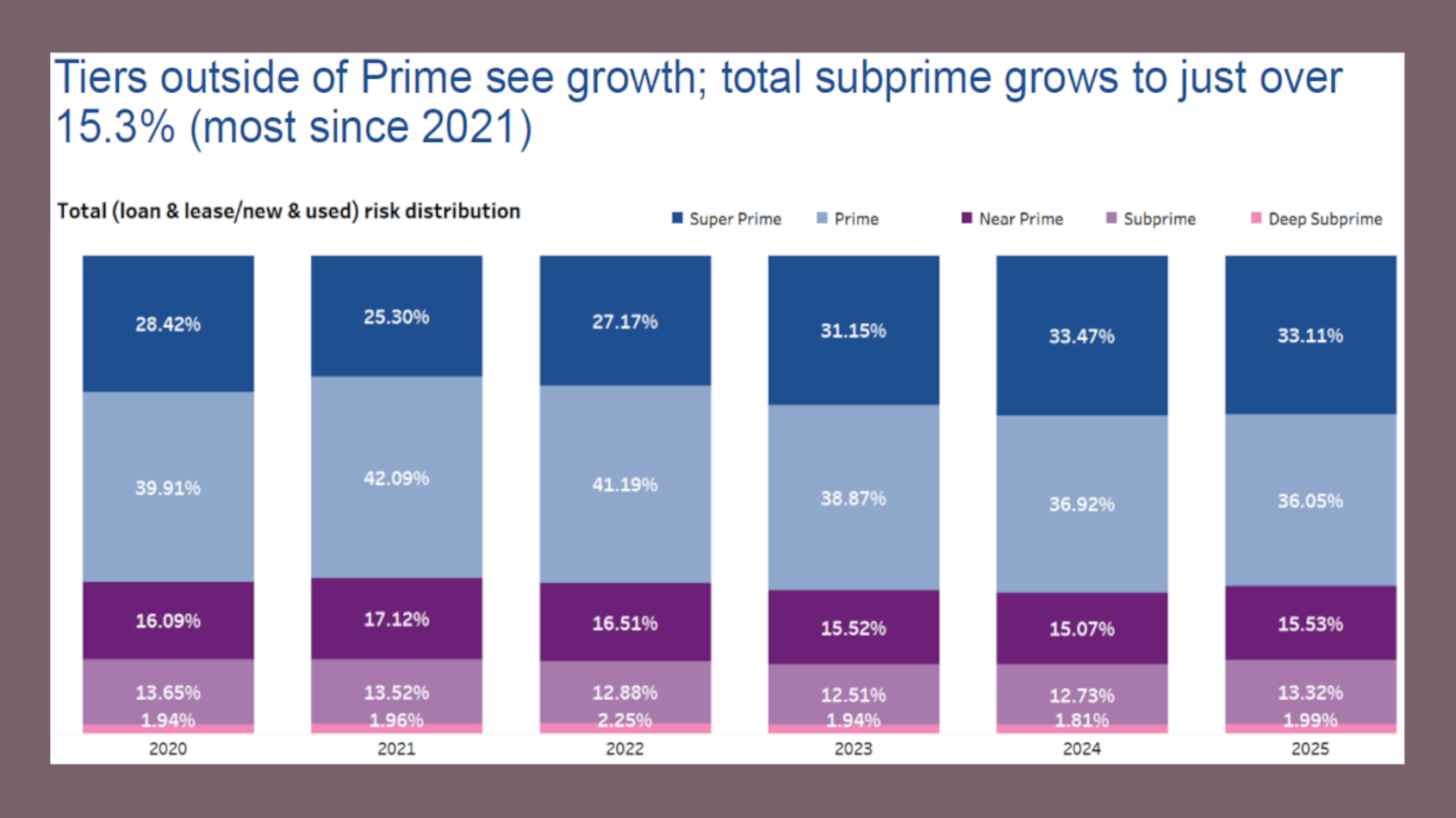

According to Experian’s State of the Automotive Finance Market Report: Q4 2025, subprime consumers made up 15.31% of total vehicle financing in the quarter. That’s up from 14.54% in the closing quarter of 2024.

Furthermore, Experian determined the level represents subprime consumers’ largest share of the total vehicle finance market in the fourth quarter since 2021.

“Recent growth in the subprime segment reflects sustained consumer demand for vehicle financing, even as market conditions continue to shift,” said Melinda Zabritski, Experian’s head of automotive financial insights.

“As affordability remains top of mind, both lenders and consumers are adapting, reflecting broader trends in credit patterns and vehicle financing behavior,” Zabritski continued in a news release.

And it’s not just the financing of vehicles near the end of their lifespan that’s fueling this subprime surge.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

For new-vehicle financing, Experian reported the subprime market grew to 6.61% in Q4 2025, up from 5.74% during the same time a year earlier. Meanwhile, analysts noted there was a slight decline in prime, going from 36.49% to 35.33% based on the same comparison.

But the used-car market still has plenty of subprime paper. Experian found that subprime consumers constituted 22.47% of used-vehicle financing during the quarter, up from 22.11% in Q4 2024. And prime went from 36.75% to 35.88%, according to Experian tracking.

Meanwhile, whether the individual is within the subprime basket or has nearly a perfect credit file, Experian indicated the amount financed continued to rise.

In the fourth quarter of 2025, Experian the average loan amount for a new vehicle increased $1,882 year-over-year, reaching $43,582. The average monthly payment for a new vehicle increased $21 to $767 during the same period, while the average interest rate was at 6.37% this quarter, from 6.34% last year.

Analysts noted used-vehicle financing saw a slight uptick in the average loan amount, increasing $872 from a year ago to $27,528 in Q4 2025. The average monthly payment increased to $537, from $528 and the average interest rate declined from 11.63% to 11.26% year-over-year.

As the average loan amount for new and used vehicles increased, Experian data showed growth in the longer loan term distributions.

For example, analysts noticed the percentage of financed new vehicles with 73- to 84-month contract terms increased to nearly 30% in Q4 2025, up from 26.03% in Q4 2024.

And Experian discovered the percentage of financed new vehicles with contract terms of more than 85 months was at 2.22% this quarter, from 1.84% last year.

Similarly, the percentage of financed used vehicles with 73- to 84-month contract terms went from 26.11% to 28.68% year-over-year, and the percentage of financed used vehicles with terms of more than 85 months increased from 0.95% to 1.03%.

“Despite shifts in average loan amounts and monthly payments, we’re seeing the market adapt,” Zabritski said. “Consumers and lenders are finding ways, such as extending loan terms, to make the financing fall within a budget. It will be important to monitor how some of the trends evolve over the next 12-18 months.”

Experian mentioned additional findings for Q4 2025 included:

—Banks continued to lead the total automotive finance market share in Q4 2025 at 29.29%, followed by captives (27.55%), and credit unions (19.56%).

—30-day delinquencies increased to 2.54% this quarter, from 2.45% last year and 60-day delinquencies went from 0.94% to 1.00% in the same period.

—The average monthly savings when refinancing a vehicle was $84 in Q4 2025, up from $73 last year.

—New-vehicle financing slightly grew from 41.20% to 42.20% year-over-year, while used-vehicle financing declined from 58.80% last year to 57.80% this quarter.

—New-vehicle leasing remained steady, going from 24.87% in Q4 2024 to 24.37% in Q4 2025.

Experian also is offering a free webinar to elaborate on the Q4 data. Go to this website for more details.