January VantageScore report shows how affordability impact is chipping away at consumer credit health

Chart courtesy of VantageScore.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

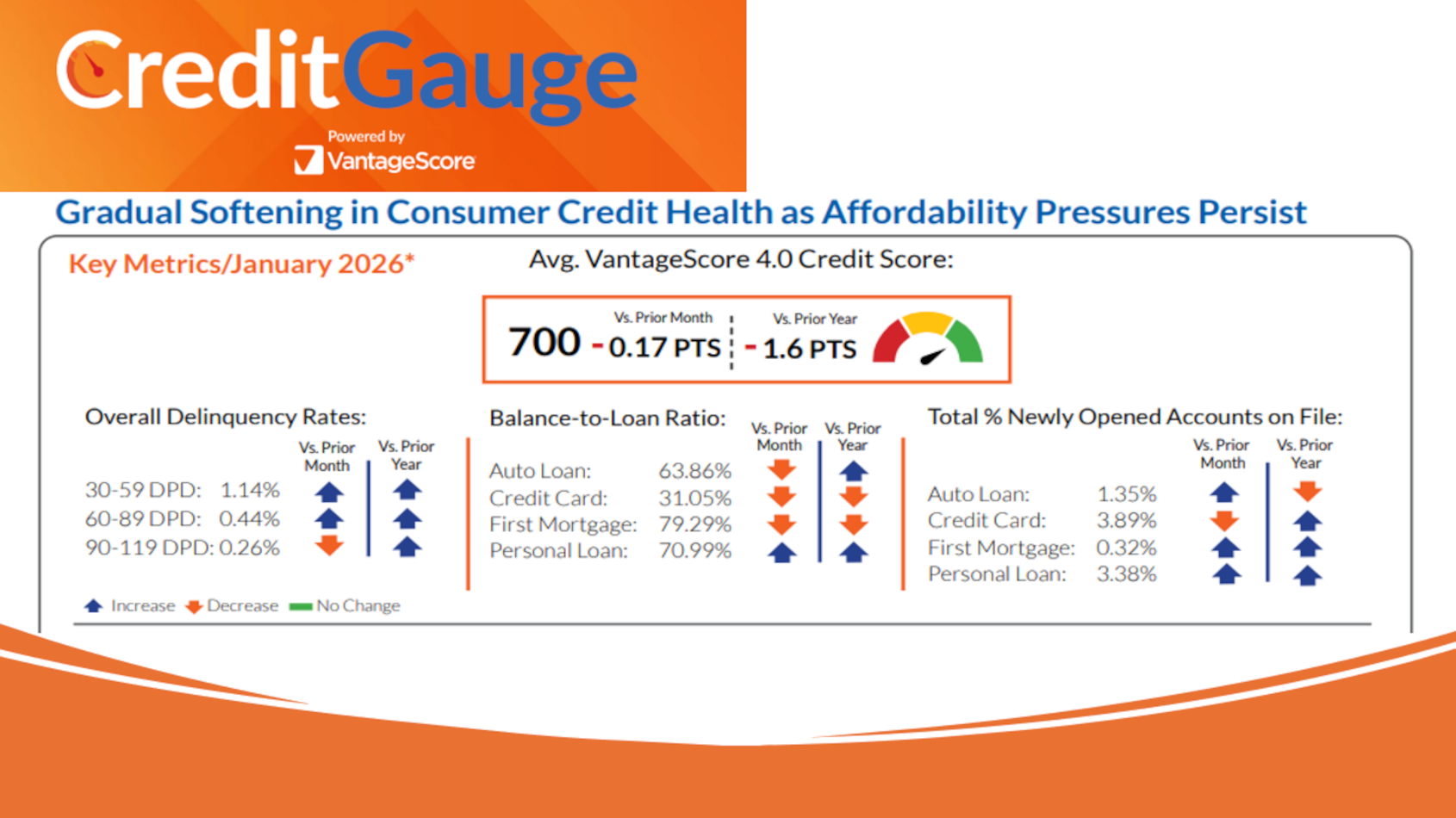

Experts from VantageScore are taking measured reactions when reviewing the January data highlighted in the latest edition of CreditGauge — a report that showed modest upticks in overall delinquency rates and slight deterioration in credit scores.

Looking at overall delinquency rates, which include auto, mortgage and credit cards, VantageScore reported on Thursday that delinquencies between 30 and 59 days past due rose to 1.14% in January, up from 1.07% in December and continuing a gradual upward trend from the middle of last year.

Analysts indicated mid-stage delinquencies — accounts between 60 and 89 days past due — edged higher to 0.44% in January, while late-stage delinquencies (ones between 90 and 119 days past due) ticked slightly lower to 0.26%.

VantageScore said in the report that the last two readings remained above pre-pandemic benchmarks, but “the steady rise in early-stage delinquencies, coupled with persistent elevation in mid- and late-stage buckets, reflects sustained affordability strain that could leave more vulnerable borrowers sensitive to further economic shocks.”

Looking specifically at auto finance, VantageScore indicated readings for the three buckets of delinquency in January came in at 2.58%, 0.98% and 0.34%, respectively. Analysts pointed out those levels in January 2020 before the pandemic officially arrived stood at 2.16%, 0.69% and 0.24%.

The upticks in delinquency might have impacted the average VantageScore 4.0 credit score, which held steady on a sequential comparison in January at 700. But that’s 2 points lower than a year earlier, according to the report.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

VantageScore determined that the share of subprime consumers increased slightly to 19.2%, up from 18.7% in January 2025, while the near-prime segment edged up to 17.8% from 17.5%.

Meanwhile, analysts added the prime and super-prime tiers declined modestly to 32.4% and 30.7%, respectively, compared to January of last year.

“This incremental growth in lower-tier shares likely reflects the combined effects of resumed student loan reporting and rising delinquencies, suggesting emerging strain among borrowers most sensitive to elevated costs and interest rates,” VantageScore said in the report.

Two of VantageScore’s experts reiterated assertions made in the January report.

“The broad-based rise in early-stage credit delinquencies across VantageScore credit tiers underscores persistent macroeconomic pressures, particularly for more vulnerable borrowers,” said Susan Fahy, executive vice president and chief digital, data and technology officer at VantageScore.

“Sustained cost pressures and interest rates may leave some consumers increasingly exposed to future economic shocks,” Fahy continued in a news release.

In a video that accompanied CreditGauge (available in the window below), VantageScore senior vice president and head of credit insights Atif Mirza added, “We track population distribution across credit tiers in our CreditGauge analysis year-over-year. And what we saw historically was that the prime segment shrank and some of the consumers moved into subprime and some moved up into super-prime. But in January, in most recent data, what we are seeing is that prime and super-prime segments shrank about half a point in prime segment and about a quarter point in super-prime. And population actually went down into near-prime and subprime segments.

“Now, this is not a sudden drop in population distribution, but a gradual increase that shows that the most more borrowers are feeling the pressure,” Mirza went on to say. “Now, the two reasons behind this, one we feel is a strong loan reporting resumption that’s affecting the credit scores for some of the borrowers. And also, as Susan alluded to, higher delinquency rates across credit tiers and credit segments.

“Now, this tells us at the start of the 2026, most consumers are feeling the pressure of high interest rates and high cost of living,” he added.

And in feeling that pressure, consumers might not be taking on lots of additional debt unless necessary.

In January, VantageScore calculated average overall credit balances carried by consumers were essentially flat at $106,800, up just $47 from December. However, that reading did reach a new post-pandemic high, according to the report, which showed the year-over-year rise to be $1,148 or 1.1%.

“Over the same period, the balance-to-loan ratio declined to 50.67%, the lowest level observed since the pre-pandemic period,” analysts said. “Together, higher balances and lower utilization suggest improved income support, increased credit availability and more selective borrowing following the holiday season.”

Turning specifically back to auto, VantageScore reported the average auto loan balance held steady at $24,800 In January, unchanged from December and up 1.9% year-over-year.

“Over the same period, the balance-to-loan ratio edged down to 63.8%, reflecting continued borrower sensitivity to financing costs amid elevated vehicle prices,” VantageScore said.

Wrapping up the auto discussion, VantageScore indicated auto loan originations in January rose month-over-month for Gen X and millennials, led by millennials at 10.9%), while activity was flat for Boomers and Gen Z and declined for the Silent Generation.

Year-over-year, analysts added auto loan originations declined across all generations, with the largest relative decrease observed among the Silent Generation at approximately 19.8%.