More mixed views of consumer confidence create added headwinds for vehicle purchase plans

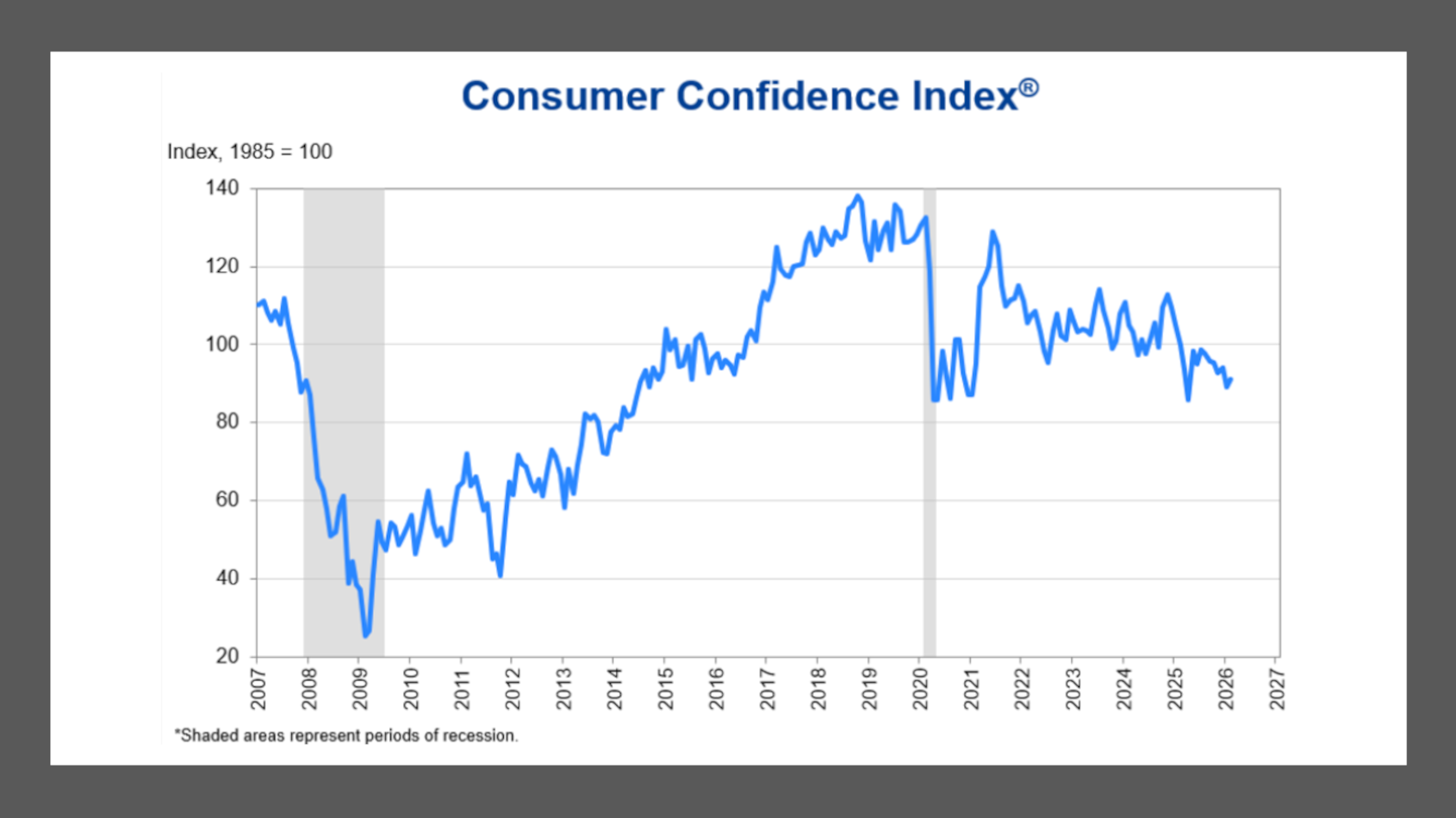

Chart courtesy of the Conference Board.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

How consumers are really doing and feeling nowadays varies significantly depending on which measurement you are viewing.

Confidence is up, but so is stress.

While the Conference Board’s Consumer Confidence Index increased in February, the LegalShield Consumer Stress Legal Index (CSLI) rose 4.4% in the fourth quarter. This marked the third consecutive quarterly increase and pushed the index 10.4% above 2024 levels to its highest sustained point since early in the pandemic.

And Cox Automotive chief economist Jeremy Robb said vehicle purchase plans ticked down slightly in February but remain up 11.2% year-over-year, “suggesting sustained interest in vehicle purchases despite broader confidence weakness.”

What all experts agree on, however, is the imminent lift that can come from federal income tax refunds.

According to the third update for this filing season from the Internal Revenue Service, the average refund is coming in about 10% higher than last year at $3,804.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Perhaps that injection of cash helped to push at least one trend higher.

The Conference Board’s Consumer Confidence Index rose 2.2 points in February to 91.2 from an upwardly revised reading of 89.0 in January.

The Present Situation Index — based on consumers’ assessment of current business and labor market conditions — decreased by 1.8 points to 120.0 in February.

The Expectations Index — based on consumers’ short-term outlook for income, business, and labor market conditions — rose by 4.8 points to 72.0.

The cutoff for data examined by the Conference Board and its preliminary results was Feb. 17.

“Confidence ticked up in February after falling in January, as consumers’ pessimistic expectations for the future eased somewhat,” said Dana Peterson, who is chief economist for the Conference Board. “Four of five components of the index firmed. Nonetheless, the measure remained well below the four-year peak achieved in November 2024 (112.8).”

Peterson added, “Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. Comments about prices, inflation, and the cost of goods remained at the top of consumer’s minds. Mentions of trade and politics also increased in February. Labor market mentions eased a bit in February, while observations about immigration increased somewhat.”

The Conference Board indicated consumers’ average and median 12-month inflation expectations were little changed but remained elevated. Consumers also believed that interest rates will persist at higher levels over the next 12 months, according to the Conference Board.

On net, the Conference Board said consumers’ views of their family’s current financial situation retreated in February, after an unexpected surge in January.

“Expectations for their family’s future financial situation continued to be less optimistic,” the Conference Board said. “Meanwhile, the share of consumers who said a U.S. recession over the next 12 months is ‘very likely’ fell, while those saying ‘not likely’ rose.

“Respondents who said recession is ‘somewhat likely’ over the next year increased somewhat, and the percent believing we are ‘already in one’ dipped,” the Conference Board went on to say, pointing out that these measures are not included in calculating the Consumer Confidence Index.

LegalShield senior vice president of consumer analytics Matt Layton explained how that firm’s data reinforced some of the findings from the Conference Board.

LegalShield’s Consumer Finance subindex grew 16.3% since January 2025, reflecting a sharp rise in legal inquiries tied to billing disputes, collections, and creditor negotiations.

And LegalShield said Q4 bankruptcy inquiries rose 15.6% year-over-year, serving as a leading indicator for federal court filings.

“Rising consumer stress seems to be a new normal,” Layton said. “Increased consumer debt is fueling consistent spending and driving up the CSLI quarter over quarter over quarter.”

Robb said last week started with the 2026 National Association of Business Economists (NABE) conference, three days of economic discussion and three Federal Reserve members speaking, “providing a great primer for thoughts about where our economy may head in 2026.”

Robb shared what caught his attention in his weekly Auto Market Weekly Summary.

“Perhaps the most striking insight from the conference: Fed governors indicated that current productivity gains in the economy are not yet being driven by AI investment — they’re coming from other factors,” Robb said in that analysis. “The implication is that AI-driven productivity is still ahead of us, potentially sustaining economic gains for years to come.

“Governors also noted that consumer spending growth is becoming more broad-based, no longer concentrated among the highest earners — a healthier demand signal for big-ticket purchases like vehicles,” Robb added.