StoneEagle: PVR record in November among Q4 performances generated by dealer F&I departments

Graphic courtesy of StoneEagle.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

StoneEagle data showed dealerships had a lot to be thankful for, especially in November, when it came to the performance of their F&I departments during the fourth quarter.

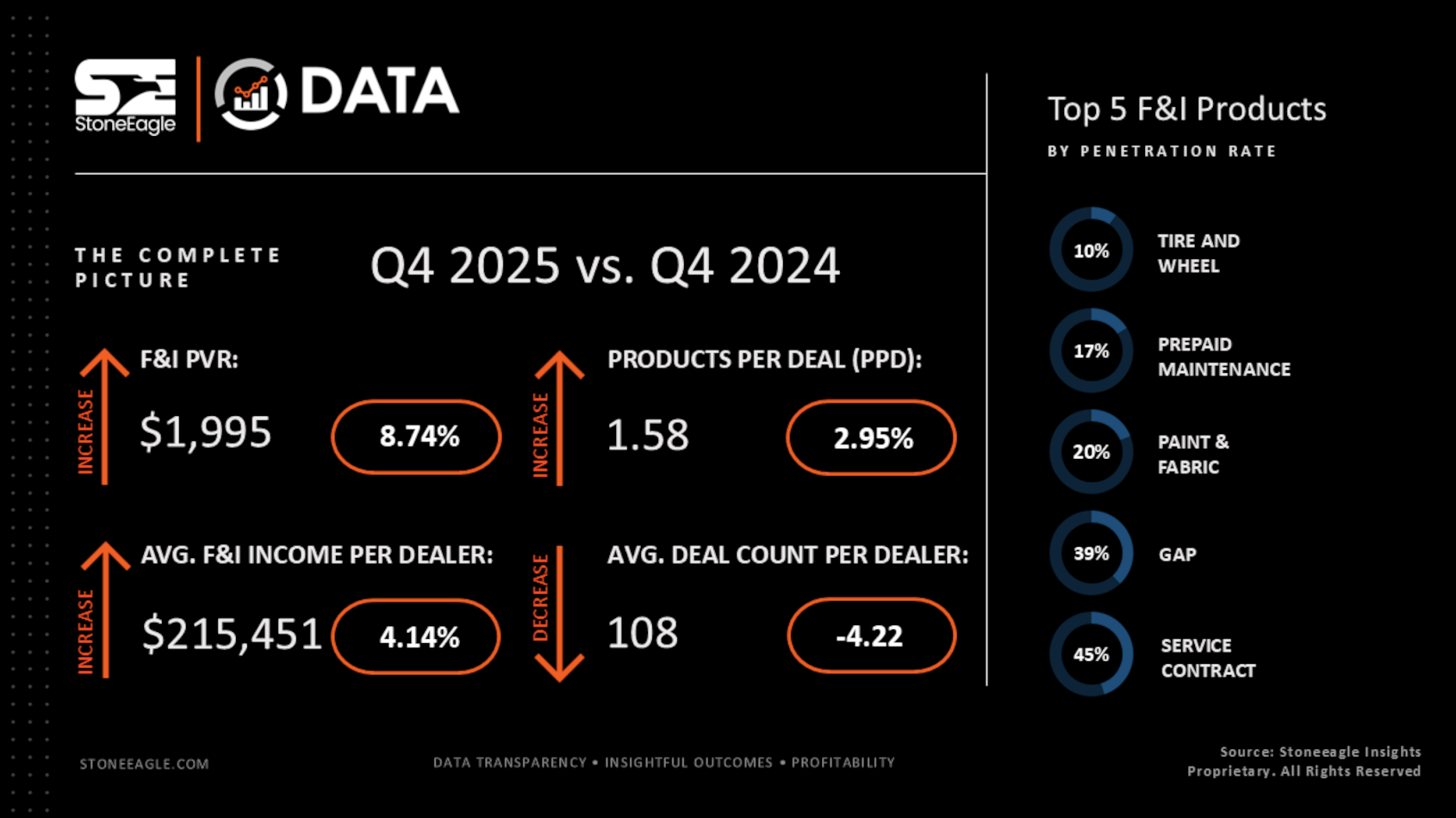

The newest StoneEagleDATA F&I Benchmark Report indicated that in the fourth quarter, F&I offices posted the highest quarterly average F&I profit per vehicle retailed (PVR) of 2025 at $1,995 and set an all-time monthly record in November at $2,025.

For the full year, StoneEagle reported average F&I income per dealer increased more than 8% compared with 2024, while average deal count remained essentially flat.

By December, nearly nine out of 10 gross dollars per deal came from F&I, according to the report, that also touched on the headwinds dealers faced.

StoneEagle pointed out that dealers turned a year marked by tariff talks, inventory swings, electric-vehicle questions, and affordability concerns into steady, consistent results as front-end margins fell to their lowest level since January 2022 at $279 per deal to close out 2025.

Through that compression, StoneEagle reiterated that F&I provided the foundation that kept results steady throughout the year.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

StoneEagle CEO Cindy Allen said, “2025 had plenty of noise — tariff concerns, rate concerns and affordability pressure — but when you zoom out, the data tells a clear story.

“Even with a flat engine from a deal-count perspective, products per deal increased, PVR reached an all-time high, and F&I income per dealer moved up year over year. I call that a pretty good year, with F&I serving as the foundation of dealership profitability,” Allen continued in a news release.

StoneEagle acknowledged the year “did not run in a straight line.”

Analysts recapped that deal volume spiked in March amid tariff-driven pull-forward activity, then lifted again in late summer as EV timing influenced buying patterns, before returning to more typical seasonality by year-end.

By December, the StoneEagle data showed a “clear” trade-off: dealers gave up front-end gross to keep deals moving, and total gross per deal closed out 2025 at $2,253, down 6.4% year over year.

The report mentioned other notable Q4 trends, including:

—F&I PVR: Averaged $1,995 per deal in the fourth quarter, up from $1,931 in the third quarter and $1,834 in the fourth quarter of 2024.

—Products per deal (PPD): Averaged 1.58 products per deal in the fourth quarter, up from 1.56 in the third quarter and 1.53 in the fourth quarter of 2024.

—Average total F&I income per dealer: Averaged $215,451 in the fourth quarter, down from $223,395 in the third quarter and up from $206,879 in the fourth quarter of 2024.

—Average front-end gross per deal: Averaged $403 per deal in the fourth quarter, down from $561 in the third quarter and $508 in the fourth quarter of 2024.

—Total gross per deal: Averaged $2,397 in the fourth quarter, down from $2,492 in the third quarter and $2,484 in the fourth quarter of 2024.

StoneEagle went on to mention that product performance remained steady throughout the year, with service contracts and GAP continuing to anchor F&I production.

The report showed that performance strengthened into the fourth quarter, with service contracts reaching 46% in November and GAP peaking at 40%.

Analysts added ancillary categories remained a significant contributor, accounting for roughly one-third of product-driven F&I income and reinforcing the balanced revenue structure seen throughout 2025.

Here are some other specifics that StoneEagle uncovered:

—Vehicle service contracts (VSC): Reached 45% penetration in the fourth quarter, up from 44% in the third quarter and 43% a year earlier.

—Guaranteed asset protection (GAP): Reached 39% penetration, up from 38% in the third quarter and 35% a year earlier.

—Paint-and-fabric protection: Averaged 20%, unchanged from the third quarter and consistent with the fourth quarter of 2024.

—Prepaid maintenance: Increased to 17%, up from 16% in the third quarter and 16% a year earlier.

—Tire-and-wheel protection: Averaged 10%, matching the third quarter and the fourth quarter of 2024.

“The engine that drives F&I is product,” StoneEagle chief product officer Colin Snyder said in the news release. “Core coverages like service contracts and GAP stayed steady, while ancillary remained the expansion story.

Dealers are leaning into that flexibility — including bundled options and protections that resonate even on cash deals — to keep performance strong,” Snyder went on to say.