StoneEagle sees F&I trends stay strong among Q1 dealer profits

Graphic courtesy of StoneEagle.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Just ahead of Memorial Day weekend, StoneEagle released first-quarter findings from its StoneEagleDATA F&I Benchmark Report, highlighting how much hay dealership F&I offices made during the first three months of the year.

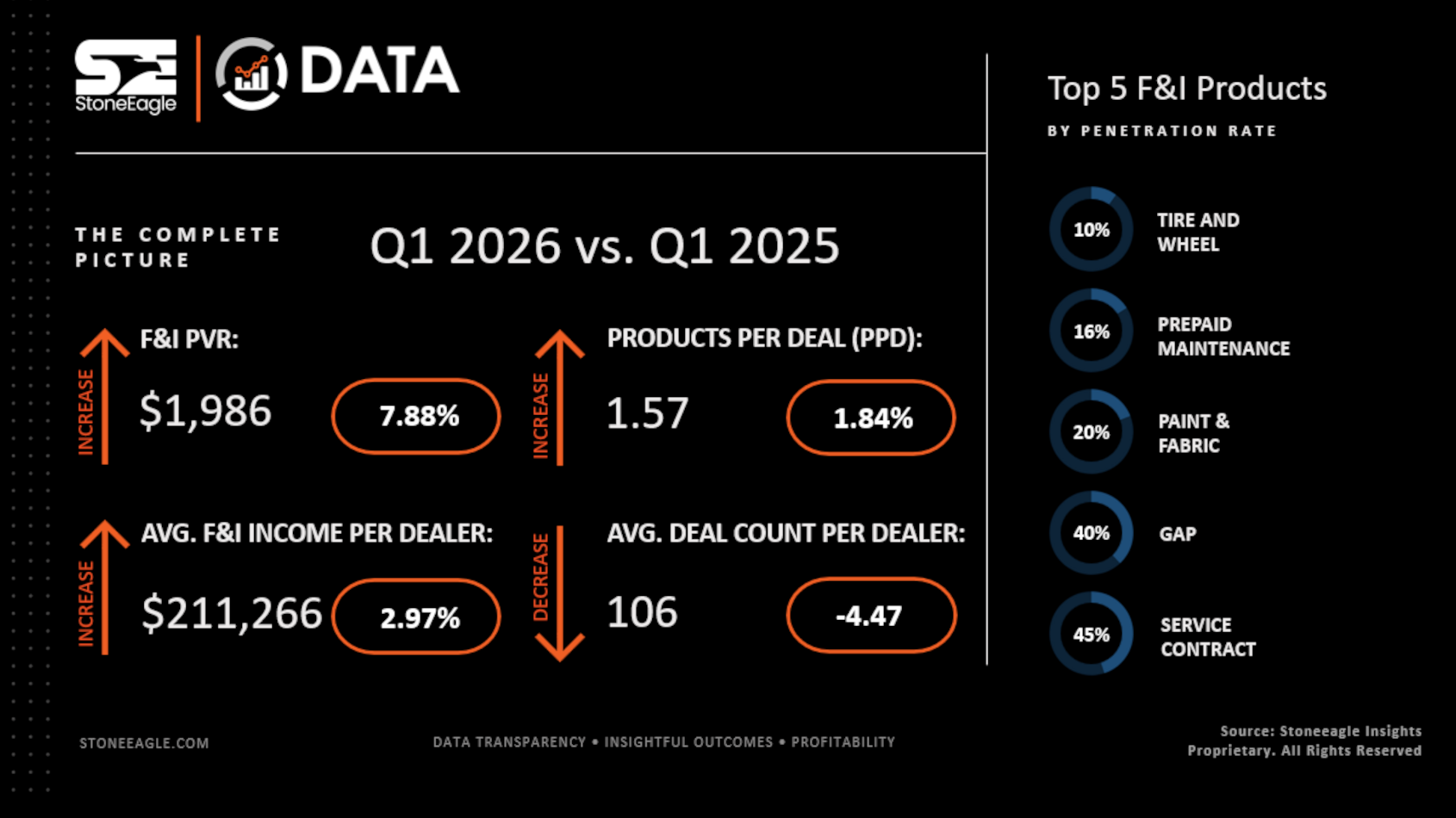

Analysts indicated the first quarter extended one of the strongest F&I performance stretches in StoneEagleDATA, with F&I offices averaging $1,986 in F&I profit per vehicle retailed (PVR).

StoneEagle determined that figure is up nearly 8% year-over-year, landing roughly 50% above 2019 levels.

Analysts determined stronger per-deal performance helped push average monthly F&I income per dealer 3% above prior-year levels, reaching $211,266. StoneEagle said this growth arrived despite 4.4% fewer deals per dealer than a year ago, as retail activity returned to more typical seasonal patterns.

“The first quarter showed that dealership F&I performance remained historically strong even as retail activity settled back into more traditional seasonal patterns,” StoneEagle CEO Cindy Allen said in a news release.

“Even with fewer deals moving through the average dealership, F&I income still increased year over year as dealers relied more heavily on F&I to help balance affordability pressure and lower front-end gross, reinforcing F&I’s role as the foundation of stability and profitability for dealerships,” Allen continued.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

StoneEagle highlighted other key Q1 performance metrics, including:

—F&I profit per vehicle retailed (PVR): Averaged $1,986 per deal in Q1 2026, up from $1,841 in Q1 2025.

—Average products per deal (PPD): Averaged 1.57 products per deal, up from 1.54 in Q1 2025.

—Average monthly total F&I income per dealer: Averaged $211,266 in Q1 2026, up from $205,175 in Q1 2025.

—Average deal count per dealer: Averaged 106 deals per dealer, down from 111 in Q1 2025.

—Average front-end gross per deal: Averaged $539 in March 2026, down from recent post-COVID highs but still 33% above January 2019 levels.

The topic of the year so far — affordability — also surfaced in the StoneEagle report.

Analysts acknowledged pressures continued compounding inside the first quarter’s average car deal, with nearly one in four financed purchases stretched to 84 months or longer.

StoneEagle reported the average amount of negative equity carried into new-vehicle purchases rose 36% year-over-year to $8,728, while average down payments declined 14% to $3,993.

“Together, the trends showed how the average vehicle transaction is carrying substantially more weight than it did just a few years ago,” analysts said.

As a result, StoneEagle determined the pressure continued shaping dealership profitability through the first quarter, with average front-end gross falling 21% from January 2025 to $539 in March 2026. That’s still roughly 33% above 2019 levels but more than 50% below the post-COVID peak reached in 2022.

Analysts also touched on ancillary products, which continued to gain share, according to StoneEagle tracking.

Perhaps to be expected, StoneEagle found that vehicle service contracts (VSC) and guaranteed asset protection (GAP) anchored F&I performance again during the first quarter, while ancillary products expanded their contribution to dealership profitability.

StoneEagleDATA benchmarks showed ancillary products accounting for roughly one-third of total F&I product revenue, up roughly 19% since 2020.

A few other trends connected with this part of F&I included:

—VSC: Maintained a 45% penetration rate in Q1 2026, up from 44% in Q1 2025 and nearly 5% since 2022.

—GAP: Maintained a 40% penetration rate in Q1 2026, up from 38% in Q1 2025 and more than 6% since 2022.

—Paint-and-fabric protection: Reached a nearly 20% penetration rate in Q1 2026, up from 19% a year earlier and nearly 76% above 2020 levels.

—Prepaid maintenance: Held above a 16% penetration rate in Q1 2026, consistent with Q1 2025 and up nearly 11% since 2020.

—Tire-and-wheel protection: Maintained an approximately 10% penetration rate in Q1 2026, in line with Q1 2025 and up roughly 9% since 2020.

—Bundled product packages: Reached a nearly 7% penetration rate in Q1 2026, with penetration increasing more than 94% since 2020.

“As consumers finance larger balances across longer ownership cycles, products tied to vehicle protection and negative-equity exposure are becoming a more important part of the F&I conversation,” StoneEagle Colin Snyder chief product officer said in the news release.

“VSC and GAP continue anchoring dealership F&I performance, while broader product attachment trends reflect how financing conditions are reshaping the overall product mix,” Snyder went on to say.