Subprime lags behind Dealertrack Credit Availability Index climb of 5 straight months

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

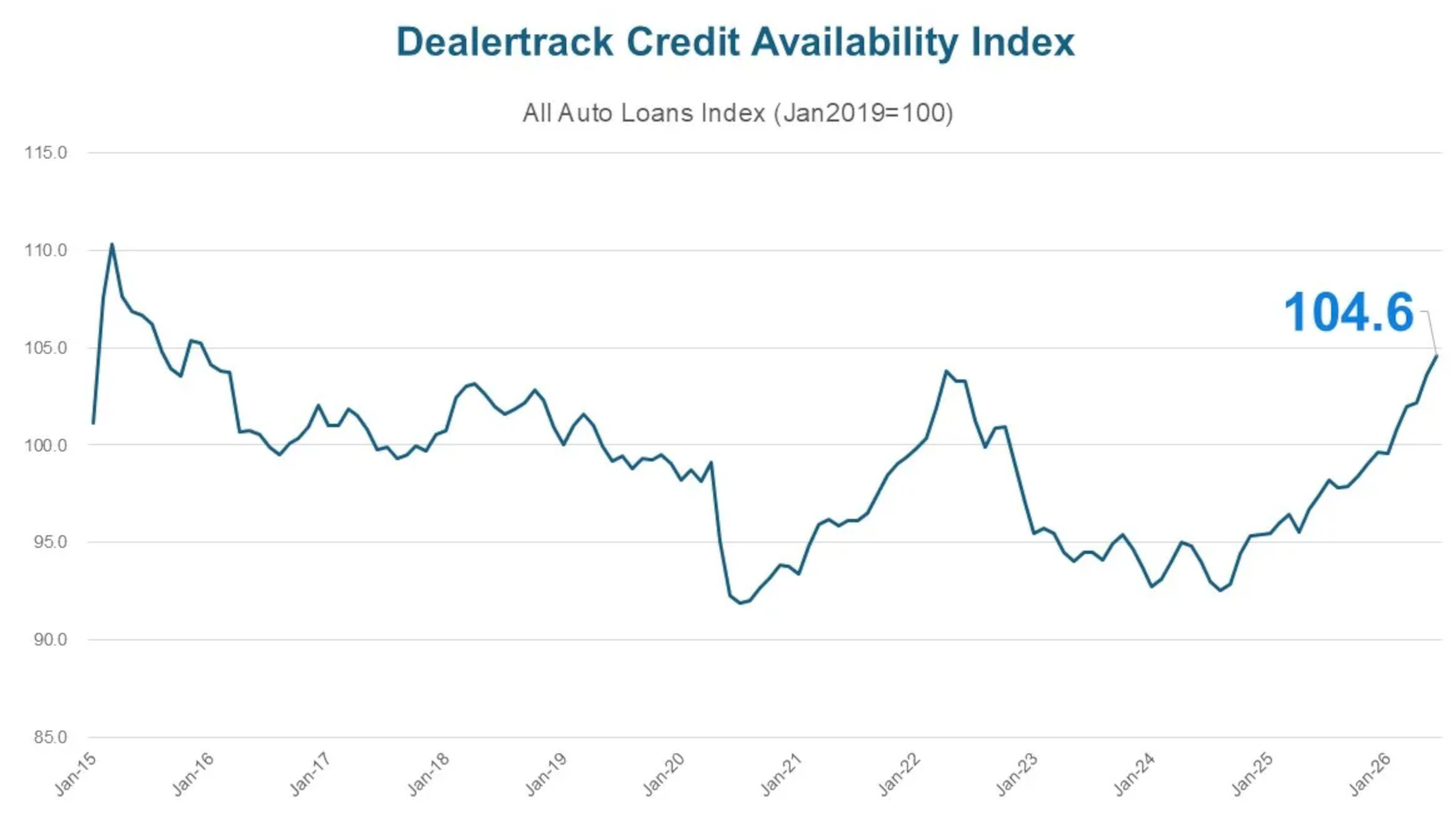

The June Dealertrack Credit Availability Index climbed to the highest level in more than a decade, but the subprime segment isn’t surging to that degree.

Cox Automotive reported that the share of loans to subprime borrowers in June declined 10 basis month-over-month to 16.6%. It marked the third consecutive monthly decline following March’s bump to 19.5%.

Despite three months of pullback, Cox Automotive senior director of economic and industry insights Jonathan Gregory pointed out that the subprime share remains 250 basis points higher year-over-year, “reflecting conditions that are still more positive for higher-risk borrowers than a year ago.”

Overall, Cox Automotive found the all-loans index increased 0.9% sequentially to 104.6, marking its fifth consecutive monthly increase. The index is also up 7.3% from June of last year.

The monthly gain was driven primarily by a sharp improvement in approval rates and a continued uptick in long-term loan share, with a modest widening in the yield spread. A further pullback in subprime share only partially offset those gains,” Gregory said in an analysis that accompanied the index update.

As Gregory mentioned, Cox Automotive reported the overall contract approval rate rose to 73.8% in June. That’s 170 basis points higher than May, representing the largest monthly gain of the year.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Gregory noted that the approval rate, the rate is up 150 basis points year-over-year, as “the significant jump made approval rates the single largest contributor to June’s index gain.”

Also noteworthy from the latest index update were extended loan terms rising to a new all-time high and elevated negative equity continuing to present risk potential.

Cox Automotive indicated the share of loans with terms longer than 72 months reached 31.1% in June, a new all-time high in the dataset and 110 basis points above the May reading.

Looking year-over-year, this term share is up 410 basis points from reading of 27% in June 2025.

Gregory explained long-term loan share was the second-largest contributor to June’s index gain, and “the increase suggests lenders and consumers continue to stretch loan length to make deals work.”

Meanwhile, Cox Automotive determined that the share of loans with negative equity declined 30 basis points in June to 57%, representing the third consecutive monthly decline following March’s record high of 59.2%.

“Despite the monthly easing, negative equity remains up 220 basis points year-over-year, with most borrowers starting their new loan with a balance that already exceeds their vehicle’s value,” Gregory said.

Two other trends to note touched on the yield spread and down payment percentage.

Cox Automotive calculated that the yield spread widened 5 basis points (from 6.72% to 6.77%), “doing little to reverse May’s sharp 53 basis point narrowing,” Gregory said.

Gregory added that the average contract rate rose 11 basis points to 10.98%, a bit faster than the five-year Treasury yield’s 6 basis point rise to 4.21%.

But Cox Automotive pointed out that down payments declined 30 basis points to 13.2%, after ticking up slightly in May. Gregory said that’s “consistent with the largely flat trend seen throughout 2026. Down payment percentage is now running below year-ago levels of 13.7%.”

Per usual, Gregory wrapped up his analysis by elaborating about the implications for consumers and lenders.

Beginning first with consumers, Gregory said, “June extended May’s gains, with financing becoming even more accessible on the strength of a further jump in approval rates. That improvement came alongside a slight uptick in borrowing costs: The average contract rate rose 11 basis points to 10.98%, and the yield spread widened 5 basis points. For consumers, this means more buyers gained access to financing in June, though at a marginally higher cost.

“The broader financing picture still carries the same cautions seen in prior months,” he continued. “The share of loans with terms beyond 72 months reached a new all-time high of 31.1% and negative equity remains above year-ago levels, even after three straight months of improvement. Down payments, at 13.2%, are running below year-ago levels as well. Longer terms combined with more negative equity and lower down payments increase total loan cost and risk exposure over the life of the loan.”

What do those metrics mean for lenders?

“The index reached its highest level since December 2015, and the gain was broad-based across lender types in June,” Gregory said. “The rise in approval rates points to a growing willingness among lenders to extend credit, reflecting looser underwriting standards and a broader risk appetite across the industry. The yield spread’s 5 basis point widening in June is a reversal from May’s sharp narrowing, offering lenders a modest amount of margin relief after that compression, though it recovers only a small fraction of what was lost in May and the spread remains far tighter than it was heading into May.

“The continued pullback in subprime share is shifting the loan mix toward less risky borrowers, though subprime remains meaningfully elevated relative to a year ago. Long-term loan share and negative equity levels are ongoing watchpoints, as writing longer-term loans to borrowers already carrying negative equity compounds duration and collateral risk in lender portfolios,” he went on to say.