Subprime share moving opposite of Dealertrack Credit Availability Index, which hits highest point in more than 4 years

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

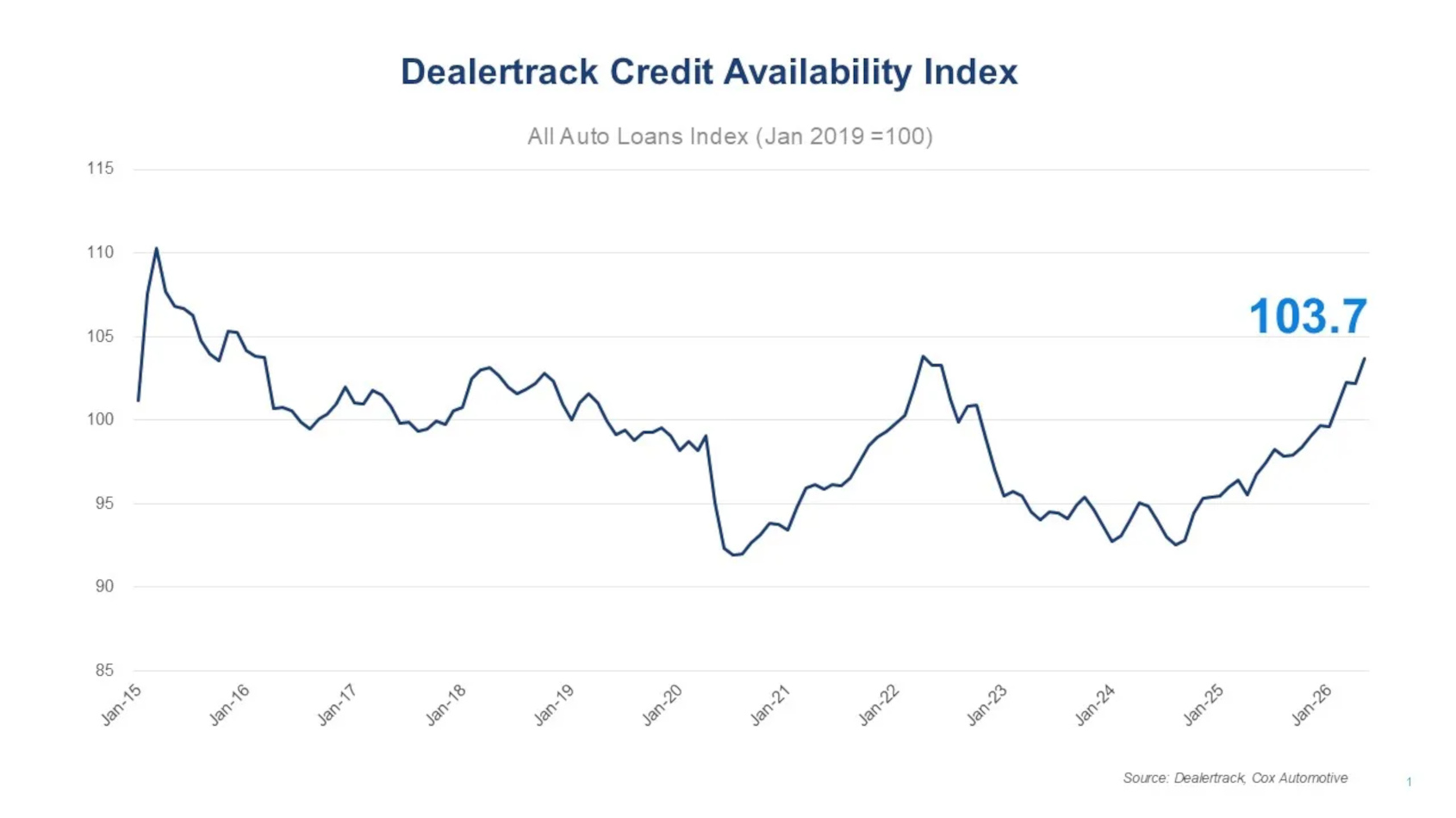

The Dealertrack Credit Availability Index for May rose sequentially for the second month in a row to land at its highest level since April 2022.

But the share of contracts to subprime consumers declined for the second consecutive month.

Cox Automotive data released this week showed the subprime share in May slid 70 basis points lower month-over-month from 17.4% to 16.7%. It was the second consecutive monthly decline following March’s jump to 19.5%.

“The continued pullback in subprime share for a second consecutive month is shifting the loan mix toward less risky borrowers, though subprime remains meaningfully elevated relative to a year ago,” said Jonathan Gregory, who is a senior director on Cox Automotive’s economic and industry insights team.

Despite two months of pullback, Gregory pointed out in his analysis that the subprime share remains 270 basis points higher than the May 2025 reading of 14.0%, “reflecting conditions that are still more positive for higher-risk borrowers than a year ago.”

Meanwhile, Cox Automotive reported the overall index rose in May by 1.5% sequentially and by 7.3% year-over-year to 102.2.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“Despite the total index reaching its highest level since April 2022, three of four lender type indices fell or were flat in May, a signal that portfolio-level dynamics varied significantly from the headline,” Gregory said. “Approval rates expanded and yield spreads narrowed in May, driving the overall index gain and indicating more favorable conditions for borrowers. However, the narrowing yield spreads also represents a narrowing margin for lenders, which adds stress.”

Here is more data showing how trends are pulling the overall index in different ways.

Cox Automotive indicated the overall contract approval rate rose to 72.4% in May, which is 180 basis points higher than April’s rate of 70.6%. It was also 50 basis points higher than a year earlier.

Gregory also pointed out the yield spread in May narrowed by 53 basis points from 7.25% to 6.72%, “accounting for the majority of May’s index gain.”

He continued that, “The narrowing reflected both modest rate declines across credit tiers and a modest shift in loan mix away from subprime borrowers,” with the average contract rate falling 32 basis points to 10.87% while the five-year Treasury rose 21 basis points to 4.15%.

Year-over-year, the spread is now down 50 basis points from 7.22% in May 2025, according to Cox Automotive.

The share of contracts with terms greater than 72 months reached 30% in May, a new all-time high in the dataset and 30 basis points higher than April’s reading of 29.7%.

“The higher share is a positive for the index, as it reflects lenders extending longer terms to support broader credit access,” Gregory acknowledged.

Gregory added the share of loans with negative equity declined 120 basis points from 58.5% to 57.3% in May. Despite the monthly easing, he said negative equity remains 250 basis points higher year-over-year.

“The broader picture, however, carries important cautions,” he said. “The share of loans exceeding 72 months reached 30% in May, a new all-time high, and remains nearly 370 basis points above year-ago levels. Negative equity still runs 250 basis points above May 2025 levels, and down payments are about 60 basis points below year-ago levels.

“The combination of longer terms, lower down payments, and more negative equity carried forward increases total loan cost and risk exposure over the life of the financing, regardless of how manageable the monthly payment appears. Consumers should carefully consider the full terms of any financing offer, particularly total loan length and overall cost,” Gregory went on to say.