VantageScore delves deeper into April auto-finance surge

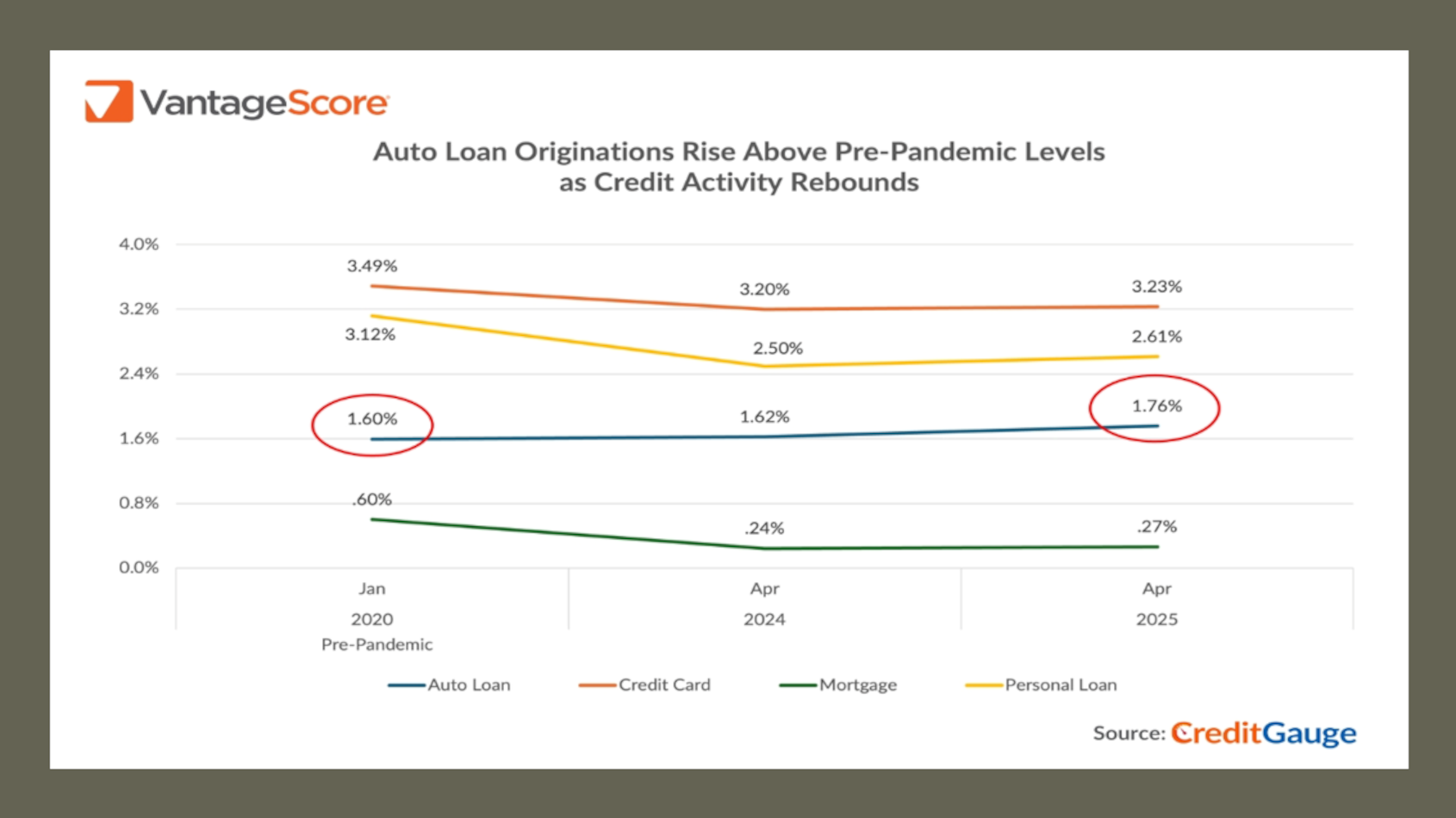

Chart courtesy of VantageScore.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

The newest data from VantageScore released this week showed that if you want to ignite auto financing, just create a global pandemic or launch tariffs among some of the world’s leading economies.

According to the latest edition of CreditGauge from VantageScore that also noted a short-term improvement in repayment activity, global reactions to the new U.S. tariffs pushed auto loans to their highest levels since January 2020.

Analysts found that auto-finance originations in April rose among all generations compared to March, with Gen Z showing the largest month-over-month gain of 0.5%.

“Economic uncertainty was a driver of consumer decisions across all age groups in April,” said Susan Fahy, executive vice president and chief digital Officer at VantageScore. “Buyers appear to have accelerated their car purchases in anticipation of higher sticker prices due to the recently implemented tariffs.”

Analysts also determined the average VantageScore 4.0 remained steady at 702 in April, edging down by just 0.1 points from the previous month.

Meanwhile, the update also showed the share of VantageScore superprime consumers (with scores between 781 and 850) rose from 30.3% in April 2023 to 31.3% in April of this year, signaling a continued gradual improvement in overall credit health.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Other key insights for the April edition of CreditGauge included:

Auto loans, personal loans lead year-over-year credit rebound

Analysts reported credit originations increased across all products compared to the prior year, with the highest growth among auto loans and personal loans. The uptick in Auto Loans likely reflects accelerated vehicle purchases ahead of potential economic volatility, along with seasonal factors like tax refund payments.

Early stage delinquencies improve

VantageScore indicated overall credit delinquencies declined across all days past due (DPD) categories on a month-over-month basis, indicating a short-term improvement in repayment activity.

Year-over-year, analysts said metrics remain elevated for both mid- (60-89 DPD) and late-stage (90-119 DPD) delinquencies, the latter likely due to the impact of resumed student loan delinquency reporting on consumer credit files.

Overall borrowing levels plateau

Average credit balances remain essentially flat month-over-month, rising just $14 (+0.01%) compared to March, according to VantageScore.

That said, analysts pointed out that the average balance-to-loan ratio has trended downward since January, decreasing to 50.81%.

“Consumers appear to be more discerning and focusing their spending on big-ticket items,” VantageScore said, while acknowledging that average balances sustained a five-year high for the fourth consecutive month, rising by $1,215 or 1.2%.