5 auto-lending headwinds FCAC found through recent research

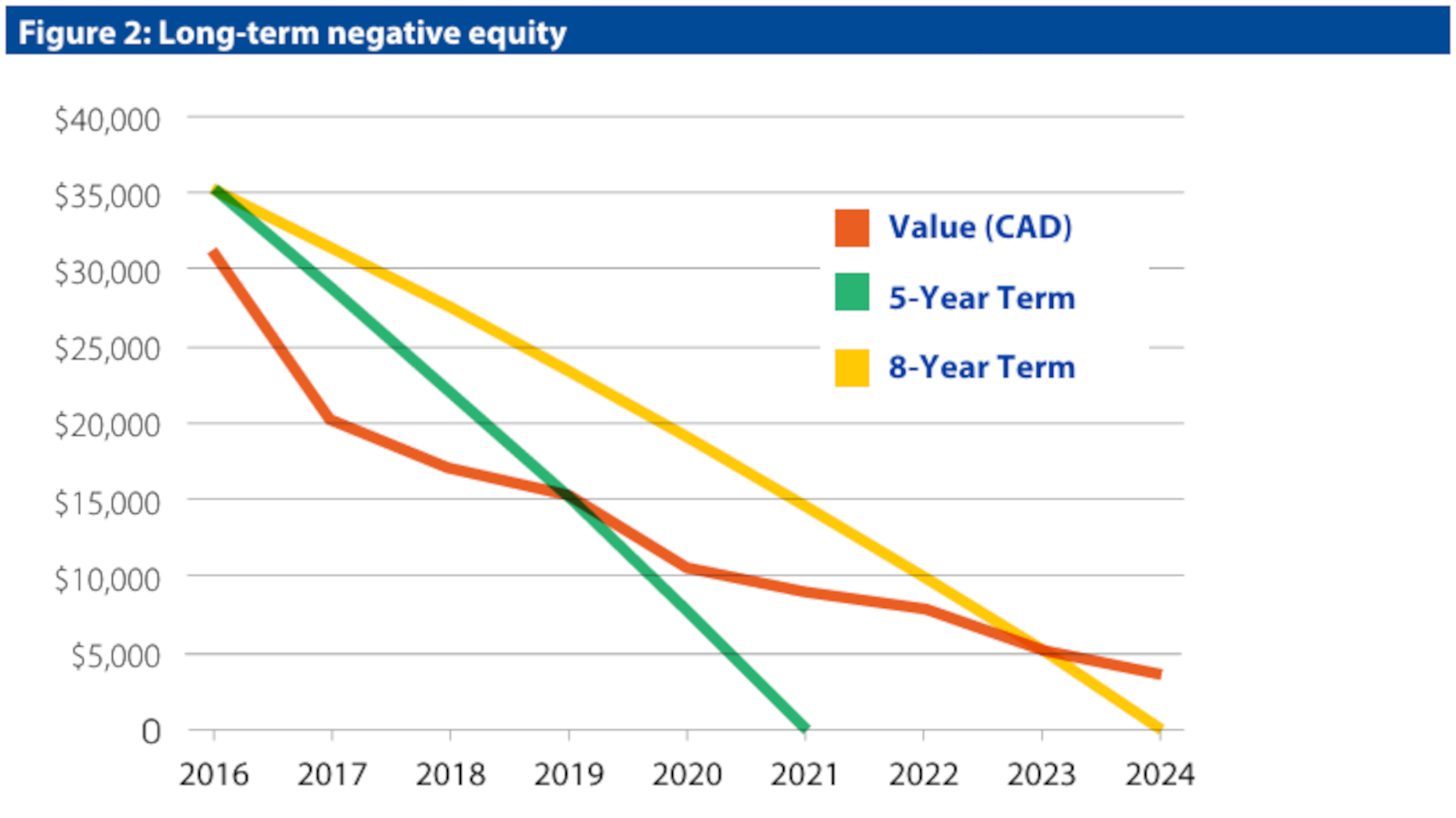

Chart courtesy of the Financial Consumer Agency of Canada (FCAC) .

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

The Financial Consumer Agency of Canada (FCAC) recently conducted research in the auto-lending space to better understand market conduct, the regulatory framework, and growing microeconomic risks.

What the agency discovered portrayed an industry that has five primary headwinds that are negatively impacting consumers, dealerships and lenders that are likely to be covered, as well, during Canada’s Used Car Week hosted by Cherokee Media Group next month.

According to the report, the first situation FCAC encountered was classified as “buying too much car.” The agency said it found the situation based on dialogue with consumer groups, market analysts, and a large automaker.

The entities suggested to FCAC, “that longer terms are encouraging consumers to buy more vehicle than they can afford. Consumers focus on monthly payments and neglect to compare the overall cost of different types of vehicles or different types of financing.

“This ‘new affordability’ has contributed to greater demand and record sales. Excessive outlays on vehicles could aggravate microeconomic risk (at the household level), especially since many households are already highly indebted,” the agency continued in the report.

Next, FCAC recapped the situation involving negative equity and extended-term loans (ETLs), which the agency defined as contracts with terms of six years or longer.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“There is a risk that a growing number of consumers will get caught on an ‘auto-debt treadmill,’ as they break their loans before they have accumulated positive equity and refinance negative equity positions into new ETLs,” FCAC said.

“This issue has been raised by analysts at Moody’s, consumer groups and the Ontario Motor Vehicle Industry Council (OMVIC). Consumers are opting for longer loan terms, but many have not adjusted by holding on to their vehicles long enough to begin accumulating positive equity,” the agency continued.

With longer terms becoming more prevalent, FCAC found the next factor, which is increased risk of loss for consumers and lenders.

“Lengthy periods of negative equity could increase microeconomic risk, particularly for consumers with larger auto loans or those who find themselves perpetually underwater. Consumers with negative equity usually have less financial flexibility if their economic situation changes,” FCAC said.

“It is worth noting that consumers who have purchased more vehicle than they can afford may not necessarily default or even fall behind on their payments, but it could jeopardize their ability to keep up with other credit obligations,” the agency continued. “Consumers whose budgets are stretched too thin by auto-loan obligations may be less resilient in the event of an economic downturn.”

Furthermore, FCAC also mentioned that these headwinds could negatively impact future financing, especially if there is a significant amount of negative equity.

“Several sources have suggested that the current trend towards more ETLs is unsustainable over the long term,” the agency said in the report. “There are limits on the number of times consumers can roll over negative positions before they begin exceeding lenders’ risk threshold.

“Lenders are comfortable with their ability to price the risk associated with financing several thousand dollars in negative equity from a consumer’s previous auto loan in a new loan. However, it is much more difficult to roll over negative equity positions a second time, and almost impossible to roll them over a third time,” FCAC continued.

And when consumers find themselves in a precarious position with their auto loan, FCAC fears that’s when fraud enters the market at an even higher rate.

“During phases in the credit cycle when consumer indebtedness is high, there is greater potential for fraud. Interest rates are low, and demand for credit is strong, but debt-to-income ratios are high, and many consumers will not meet their lender’s criteria,” FCAC said in the report. “This can create pressure to revise a borrower’s credit credentials to help close an automobile sale.

“Some observers have reported that ‘little white lies’ or ‘soft fraud’ are becoming more commonplace,” the agency continued. “Soft fraud refers to the practice of inflating a consumer’s stated income, underestimating their housing costs, or exaggerating the status of their employment by increasing the number of years they have been in the job or using a more prestigious job title (e.g., sales manager instead of sales associate).

“Soft fraud can have very serious impacts on consumers, jeopardizing their employment or saddling them with debts they cannot afford,” FCAC added.

Be it ‘soft fraud,’ negative equity or other factors, they’ll likely be covered during Canada’s Used Car Week on June 16-17 at the Delta Hotels Toronto Airport & Conference Centre.

In fact, Cherokee Media Group’s Bill Zadeits will moderate a panel focused on auto finance, featuring:

Scott Morrison, president of Nissan Canada Finance

Vincenzo Ciampi, vice president of dealer services and auto finance with iA Auto Finance

Matt Fabian director of financial services research and consulting with TransUnion Canada

Early bird registration discounts are available through May 19 by going to this website.

In the meantime, FCAC closed its auto-lending report with this pledge.

“FCAC will ensure that indirect auto loans from federally regulated banks comply with applicable federal consumer protection laws,” officials said. “In addition, the agency will work more closely with provincial and territorial authorities to provide consumers with the information they need to make responsible choices. Lastly, FCAC’s consumer education material will help consumers safely navigate the often complex market of automobile financing.”