Federal Reserve’s annual report on economic well-being of US households shows consistency

Charts courtesy of the Federal Reserve.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Perhaps there might be some turbulence in portions of your auto-finance portfolio or gas prices might be significantly pinching your business finances like they are for repossession agents.

But the overall scene might be OK for consumers, at least based on findings from the newest Economic Well-Being of U.S. Households report released on Wednesday by the Federal Reserve.

Results from the ongoing project that examines the financial circumstances of U.S. adults and their families showed that financial well-being was consistent with recent years.

Fed officials said survey results indicate that the labor market remained solid, despite some softening since the previous year’s survey.

The report also mentioned price increases remained the most common financial concern, though the share of U.S. adults saying it was a major concern declined slightly.

Results are drawn from the board’s annual Survey of Household Economics and Decisionmaking (SHED), which was fielded in October. It analyzes a wide variety of topics, including financial well-being, employment, income and expenses, and credit.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Here are more details courtesy of the Fed:

Overall financial well-being

—At 73%, the share of adults “doing OK financially” or “living comfortably” held steady in 2025, though certain demographic groups, including low-income, young, and Black adults, saw meaningful declines.

—“Price increases” remained the most common financial concern. Just above nine in 10 adults said “price increases” were a “minor” or “major concern,” unchanged from the prior year. That said, the share citing “price increases” as a major concern declined 3 percentage points.

—Concerns about “finding or keeping a job” became more common in 2025, consistent with other evidence of a solid but softening labor market. The Fed indicated 42% of adults said “finding or keeping a job” was either a “minor” or “major concern,” up from 37% in 2024.

—In contrast to people’s perceptions of their own financial situation, consumer views on the national economy worsened over the prior year and remained much more pessimistic than before the pandemic. About one-fourth of adults rated the national economy as “good” or “excellent,” down 3 percentage points from 2024 and 24 percentage points from 2019, before the pandemic.

Employment and job quality

—There was a small increase in layoffs and slightly fewer voluntary quits in 2025, indicating additional challenges for workers and job seekers. The report showed 15% of adults under age 30 were not working and said that not being able to find work contributed to them not working.

—One in four workers had used generative AI in the prior month as a part of their job. Workers with a graduate degree were more than four times more likely to use AI than those with a high school degree or less.

—81% of people who used generative AI agreed that it saves them time. Users of generative AI were also more likely to expect it to improve their career than to expect it to replace their jobs.

Economic hardships

—16% of adults did not pay all of their bills in the prior month, and 8 percent said members of their family sometimes or often did not have enough to eat. Both measures were similar to 2024.

—26% of adults skipped medical expenses because of cost in the prior year, down from 28 percent in 2024.

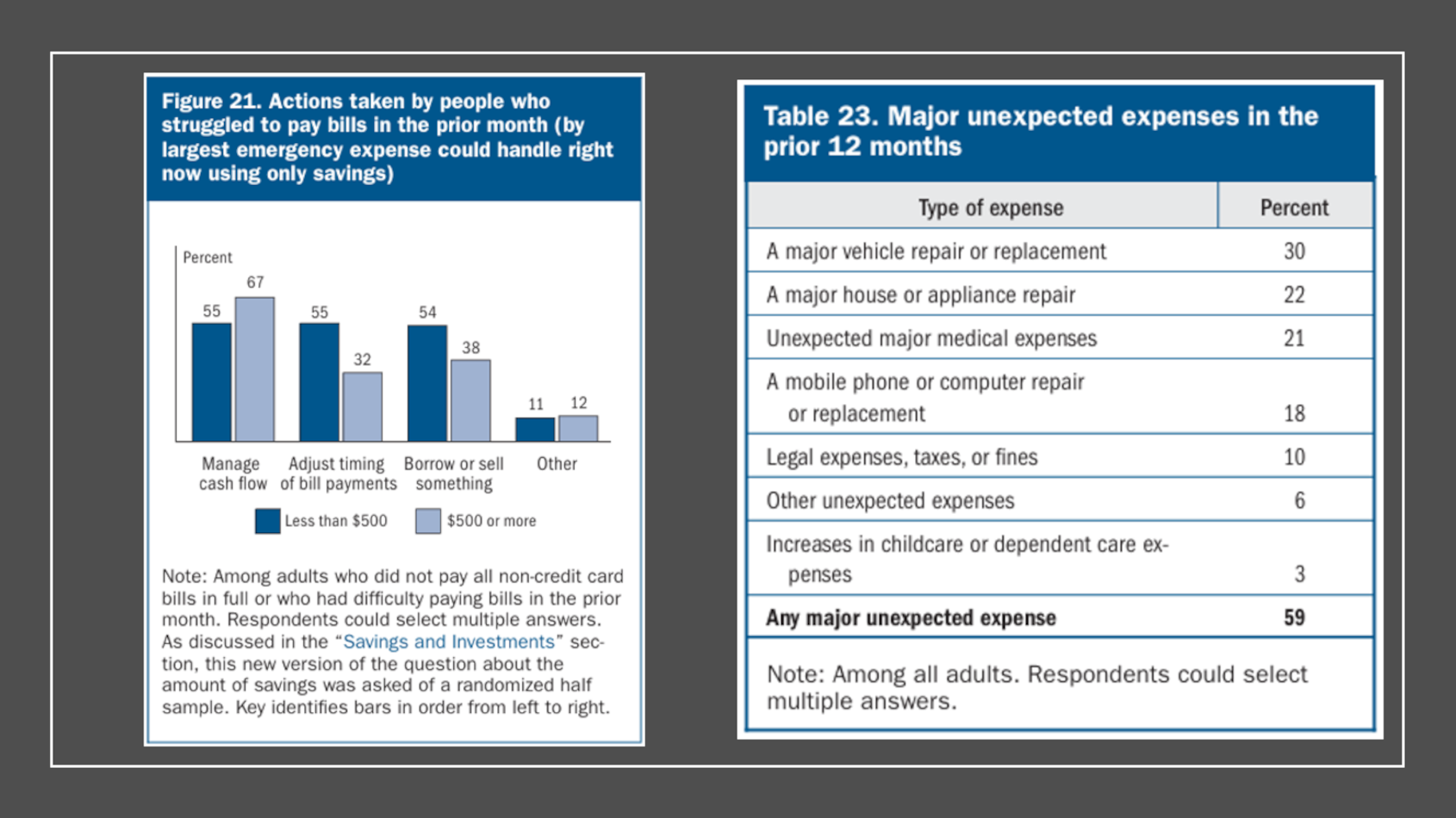

—59% of adults had at least one type of major, unexpected expense in the prior 12 months. The most common unexpected expenses were a major vehicle repair or replacement (30% of adults), followed by a major house or appliance repair and unexpected major medical expenses (22% and 21%, respectively).

Banking

—While 94% of adults had a bank account, differences by income remained large. Nearly all adults with income of at least $100,000 had a bank account, compared with 77% among adults with income less than $25,000.

—20% of adults said they experienced financial fraud or scams, similar to the prior year. As 16% experienced fraud involving their credit card, 8% experienced another type of financial fraud. Collectively, the total amount of non-credit-card fraud was an estimated $100 billion in 2025, with $56 billion borne directly by consumers.

—Low-income adults tended to lose smaller amounts of money from fraud, though those losses were meaningful. Among adults with income less than $50,000, the median loss from fraud was $400. Yet, four in 10 adults with this level of income said they could not cover even a $100 emergency expense with only their savings.

Credit

—Since 2023, total credit card balances increased more for individuals currently experiencing financial difficulty. Using merged credit bureau data, average balances increased by more than 35 percent among those who said they were “finding it difficult to get by.”

—Credit card ownership continues to be lower among Black and Hispanic adults; however, carrying a balance on a credit card was more common among these groups.

—Buy Now, Pay Later (BNPL) use edged up 1 percentage point to 16% of all adults. The report showed 11% of BNPL users had a payment trigger an overdraft or non-sufficient funds (NSF) fee from their bank in the prior year.

—23% of adults with student loans had recent payment difficulty. Slightly more than three-quarters of those experiencing payment difficulty said it was due to reasons related to affordability.

“As we work to support a strong and vibrant economy, it’s critical for the Federal Reserve to understand the economic experiences of families and communities,” Federal Reserve Board Governor Michael Barr said in a news release. “The SHED provides valuable data on how households are dealing with evolving financial opportunities and challenges.”

The entire report can be found via this website.