With additional insight about affordability, FICO watches average credit scores tick lower again

Chart courtesy of FICO.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

It probably doesn’t take a doctorate in economics to make the connection of affordability challenges to another drop in average credit scores.

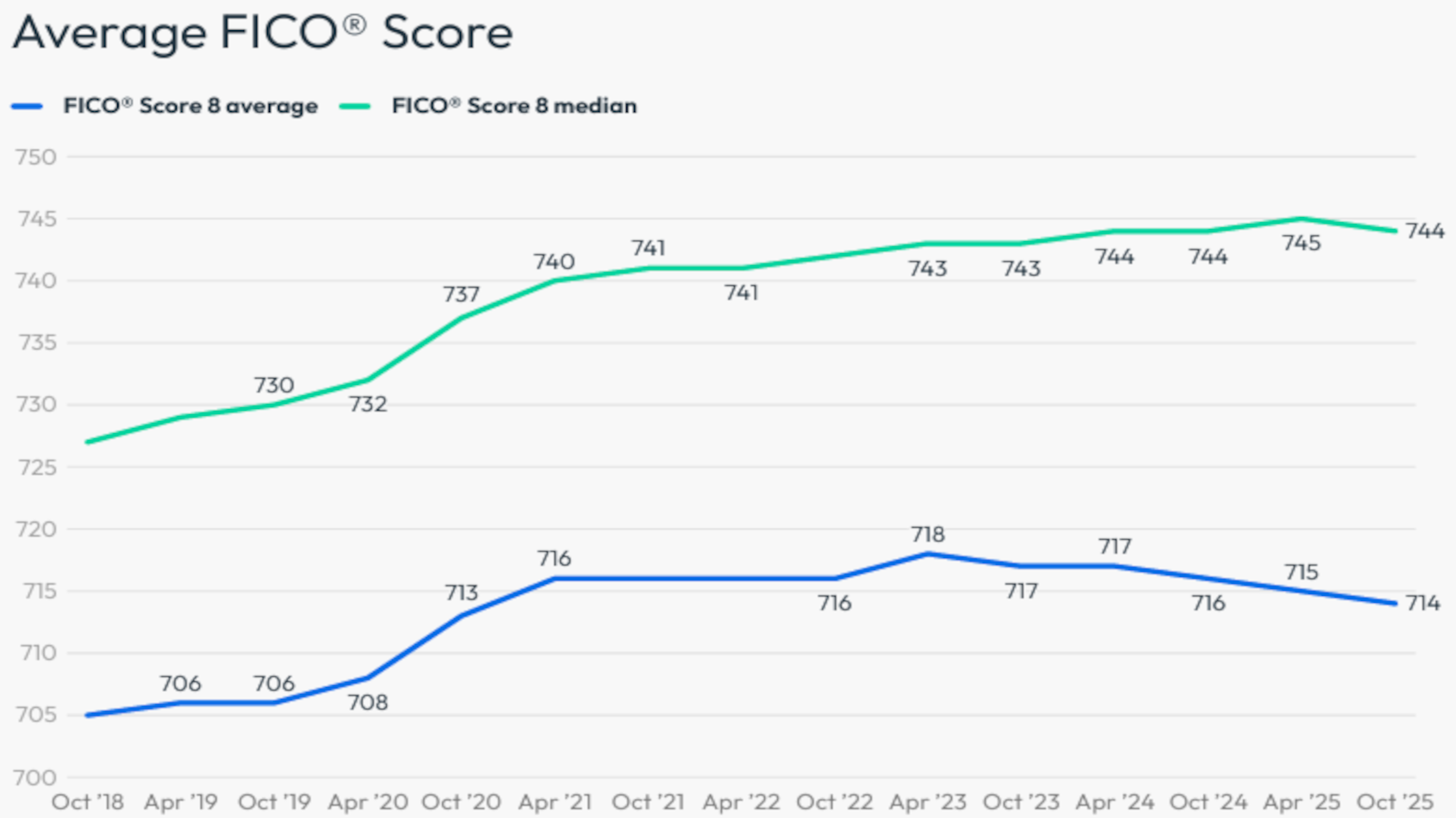

Those trends are among the findings included in the spring 2026 edition of the FICO Score Credit Insights report, which showed the average U.S. FICO score declined to 714, continuing a gradual downward trajectory since 2023.

But perhaps illustrating the slice of consumers who are doing well in this environment showing up in certain trends, FICO also said a record 48.1% of consumers now have FICO scores of 750 or higher.

FICO explained the findings point to an increasingly segmented credit market consistent with a K‑shaped economy, with a growing share of consumers maintaining strong credit profiles while challenges persist for lower‑scoring borrowers, particularly amid elevated inflation and higher interest rates.

“The resumption of required student loan payments and a continued, modest rise in mortgage delinquencies nudged the average score slightly lower,” said Ethan Dornhelm, head of scores analytics at FICO.

“What makes this particularly interesting is that we’re simultaneously seeing a record share of consumers demonstrating strong, consistent credit behaviors,” Dornhelm continued in a news release. “The result is a credit market that’s both more challenging for some and more rewarding for others — a dynamic that requires more nuanced strategies from lenders.”

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Other key findings from the spring 2026 report that’s available online included:

—Average FICO score slips to 714: The national average FICO score continued a downward trend, falling 2 points in the last year, driven primarily by resumed student loan delinquency reporting and a modest increase in mortgage delinquencies.

—Delinquencies stabilize across most products: Auto, credit card, and personal loan delinquency rates leveled off or improved, while mortgage delinquencies continued to rise to pre-pandemic levels.

—Student loan delinquency growth slows: After a sharp increase earlier in 2025 coinciding with the resumption of student loan delinquency reporting, student loan severe delinquency rates rose only marginally between April and October.

—Score distribution reflects a K-shaped economy: As mentioned, 48.1% of U.S. consumers now have FICO scores of 750 or higher, up from 43.3% in 2019. The share of consumers in the middle score ranges continued to decline as both high-score and lower score segments expanded, reflecting divergent credit outcomes.

—Gen Z leads credit card openings: More than 25% of Gen Z consumers with a valid FICO score opened at least one credit card in the past year, the highest rate of any age group.

Along with those findings, FICO shared new consumer research conducted by The Harris Poll on behalf of the company.

The research determined Americans are highly focused on improving their financial health, with 83% saying maintaining or improving their credit scores is a priority for them this year.

However, FICO pointed out that affordability challenges exist, with nearly one in four — 24% to be exact — reporting they made less than their minimum payment or skipped a credit card or loan payment in the past 12 months due to inflation.

Despite these financial challenges some are experiencing, the research found that consumers are thinking strategically about credit decisions, with more than three-quarters (77%) factoring interest rates into the timing of credit applications and 29% saying they won’t apply unless rates drop to a certain point.

Yet while consumers demonstrate sophistication in timing applications around rates, FICO discovered fundamental knowledge gaps remain about the credit behaviors that actually qualify them for those better terms.

The research showed 67% of participants either incorrectly believe income directly affects credit scores or acknowledge they are unsure whether it does. Experts explained that’s a misconception that could prevent consumers from recognizing that credit improvement is achievable through behavioral changes rather than higher paychecks.

FICO added this knowledge gap underscores continued demand for transparency and education, particularly as 77% report that being able to continuously monitor their credit scores provides them peace of mind.

“The findings point to a shift in how consumers relate to credit. It’s no longer passive, it’s intentional,” said Jenelle Dito, vice president of consumer empowerment programs and partnerships at FICO.

“People are monitoring their credit and thinking strategically, but many still lack clarity on the fundamentals. Closing that knowledge gap is critical because consumers aren’t just seeking better financial outcomes. They’re seeking peace of mind, making this as much about emotional well-being as credit health,” Dito went on to say.