JD Power explains the ‘delicate balancing act’ & possible ‘day of reckoning’

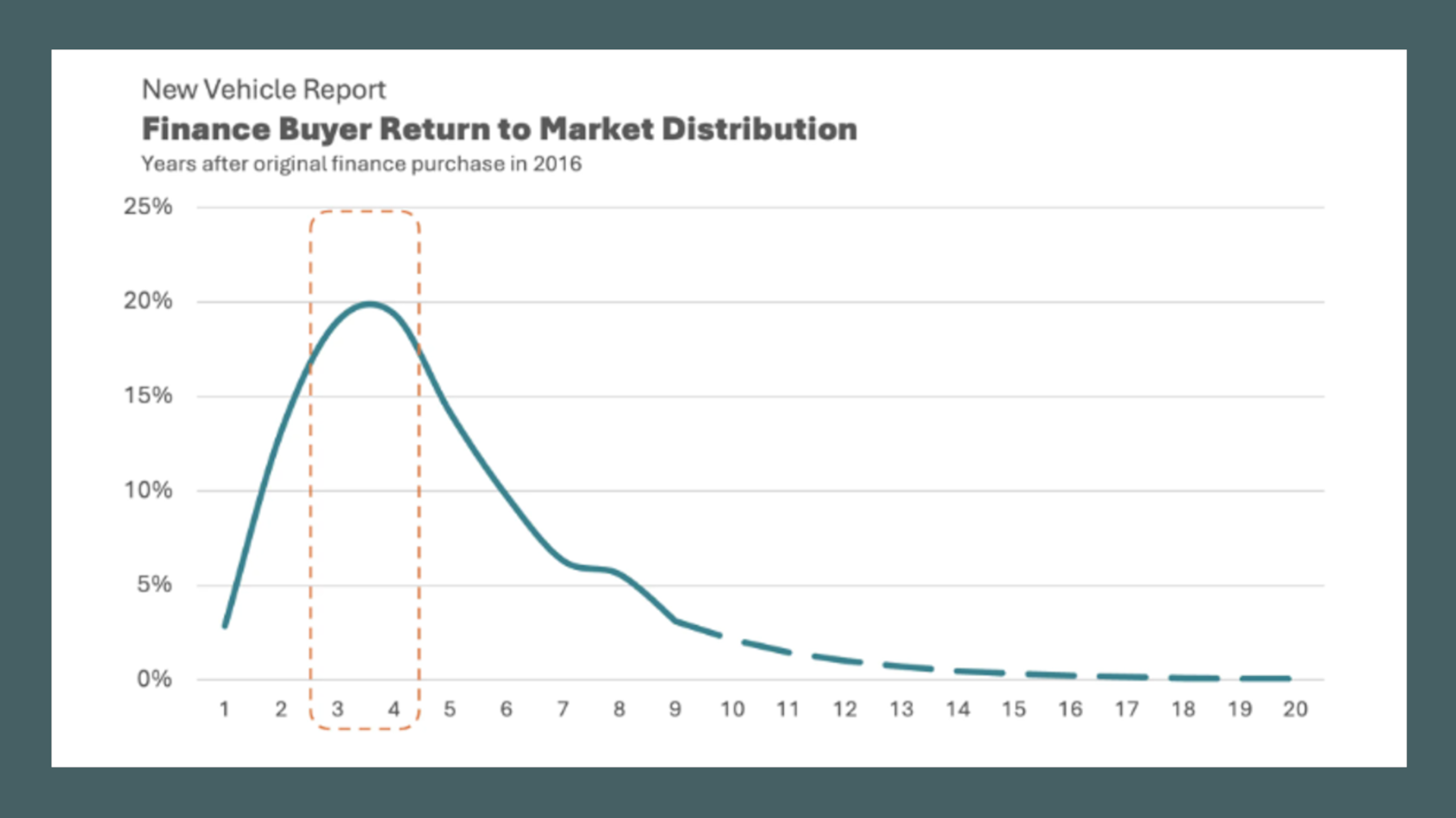

Chart courtesy of JD Power.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Perhaps few would fault you if you read this auto-finance story recapping the newest Automotive OEM Intelligence Report based on insights gathered from JD Power intelligence and proprietary market data and that booming movie trailer narrator voice comes into your mind.

Especially since authors Tyson Jominy and Srini Rajagopalan used terms such as a “delicate balancing act” and a possible “day of reckoning.”

Jominy, who is senior vice president of OEM customer success, and Rajagopalan, who is vice president, OEM customer success, arrived at those potentially ominous phrases after collecting new-car finance data associated with contract terms and negative equity.

In introducing that “delicate balancing act,” Jominy and Rajagopalan wrote, “Longer loan terms are both a necessity and a signal. They help sustain sales volumes in the face of high transaction prices. Without them, many consumers would be priced out of the new-vehicle market. At the same time, their continued prevalence signals underlying affordability stress. Extended terms are compensating for higher prices rather than resolving the root cause.

“For the better part of the last two decades, extended-term financing and cash incentives have helped the auto industry navigate a tricky balancing act between volatile swings in supply and demand,” they continued. “From the 2008 financial crisis to the COVID-19 pandemic, where aberrant trends in vehicle supply warped traditional patterns of vehicle sales, consumers have become increasingly reliant on these synthetic forms of liquidity to keep buying new cars, trucks and SUVs.”

And now for that potential movie-trailer crescendo that prompted Jominy and Rajagopalan to mention “a day of reckoning.”

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

They wrote, “While the auto and consumer financing industries still have plenty of tools at their disposal to keep this cycle going for the near-term, the extended buildup of longer-term loans, increased negative equity and liberal use of incentives could eventually create a day of reckoning where it is impossible to keep engineering a soft landing.”

Whew, that sounds like a summertime box-office thriller for the industry, huh? Perhaps not for dealerships and finance companies who need to keep things churning to keep cars rolling over the curb and profitable loans in the portfolio.

So how did we get here? Let’s get into the auto-finance movie plot that JD Power explained with its data through this report.

Through March, JD Power reported the average monthly new-vehicle loan payment is $806, up $40 from March of last year.

Furthermore, 18.4% of all finance customers have a monthly payment of more than $1,000, according to JD Power, which pointed out this market segment is dominated by premium and pick-up truck customers.

JD Power data also indicated that contracts of 84 months or longer accounted for 12.8% of all sales in March, climbing steadily from 7.3% in March 2019.

Similarly, JD Power said 72-month loans now account for 40.5% of all sales, up 4.1 points since March 2019.

“These longer terms are no longer niche offerings. They are a core affordability tool in a high-price environment,” Jominy and Rajagopalan wrote.

And are these buyers keeping that vehicle for the duration of that contract? (It’s OK if a movie laugh track popped into your mind.)

JD Power said 20% of all new-vehicle buyers return to market within three to four years of their original purchase. Among those with 84-month loans, JD Power noted that percentage jumps up to 44.6%.

“This suggests clearly that buyers opting for longer loan terms are monthly payment shoppers, seeking a monthly outlay that fits within their budgets,” Jominy and Rajagopalan wrote.

And, of course, trading a vehicle before its paid off creates the conundrum dealers and lenders have had to solve for decades. In 2025, JD Power said 26% of used-vehicle trade-ins carried negative equity, up from 24% in 2024.

Jominy and Rajagopalan acknowledged negative equity is often rolled into the next transaction, also at a cost to affordability.

“A potential saving grace for these buyers are promotional incentives that may periodically aid their financial position,” they wrote. “Cash-back incentive offers are beneficial in relieving the negative equity pressure on customers returning to market. Some customers can perceive the zero-percent offers such as those seen on EVs as a panacea and return early to market.

“However, these offers do not resolve the negative equity problems, and, depending upon the level of incentive offered on new vehicles, it could become difficult for buyers to secure financing if they have too much negative equity in their trade-in vehicle,” Jominy and Rajagopalan went on to state. “Here again, the cash incentive is wildly popular in the pick-up segment, helping to drive those buyers into longer-term financing, but if those cash incentives were to go away, new-vehicle buyers could face serious challenges securing financing.”

How might this auto-finance movie unfold for the rest of the year? Might there be another notable plot twist? (Like the ongoing conflict in the Middle East pushing gas prices higher).

No matter how this installment unfolds, it sounds like sequels are already in the works.

“Extended loan terms have moved from the margins of auto finance to the center of the affordability conversation, a conversation that is now dominating the industry,” Jominy and Rajagopalan wrote.