Fitch: Stress in subprime surfaces through auto ABS trends

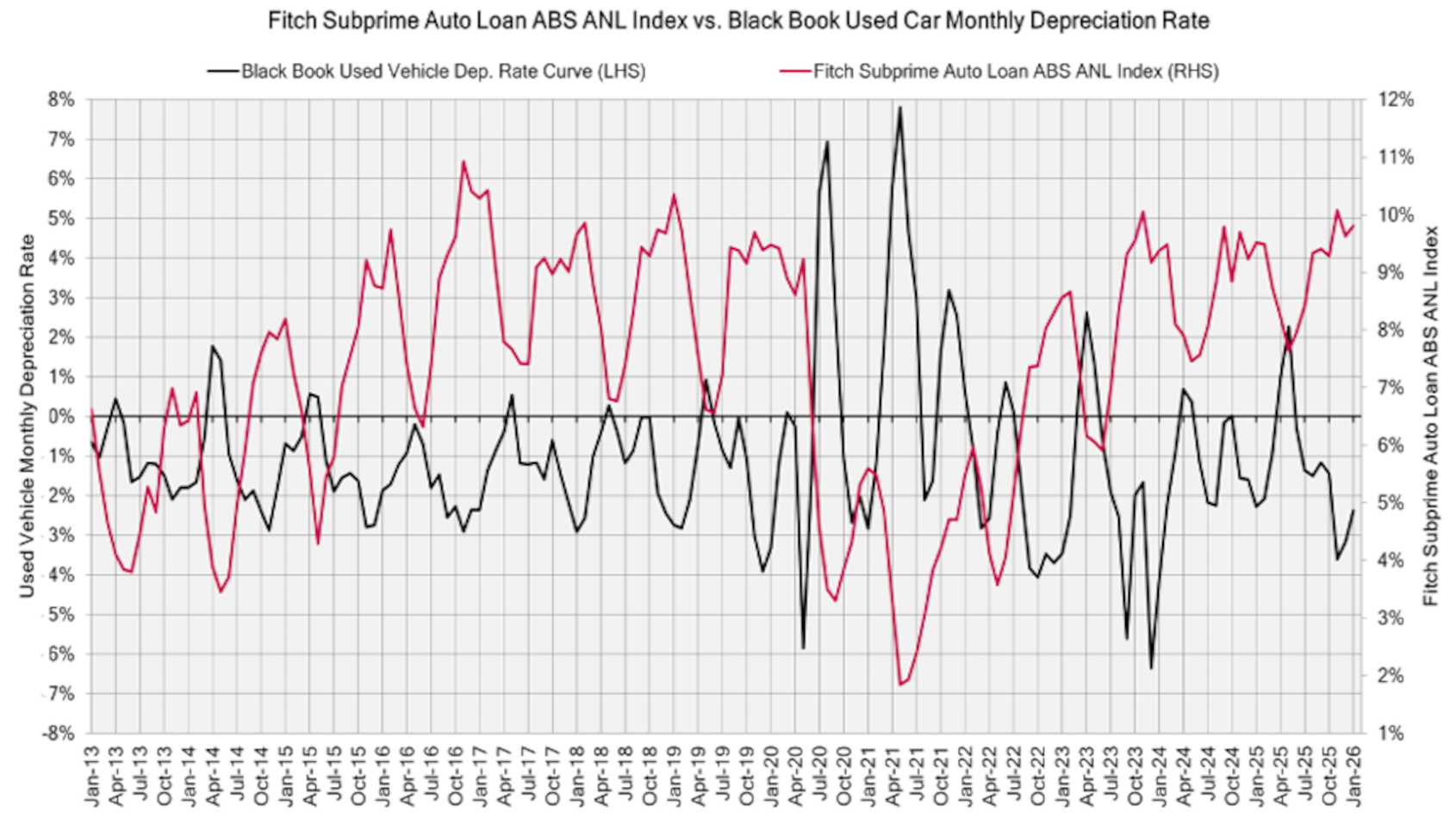

Chart courtesy of Black Book and Fitch Ratings.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Fitch Ratings took a close look at the subprime auto loan securitization space as part of the Vehicle Depreciation Report compiled in collaboration with Black Book.

Analysts used words such as stress and shocks when recapping subprime auto loan ABS performance that “remained an area of heightened focus in 2025, with deterioration more pronounced than in prime transactions.

“Subprime borrowers proved more vulnerable to economic shocks, reflecting elevated inflation, higher interest rates, and generally limited savings buffers to absorb payment stress,” Fitch continued in the report.

Analysts indicated that stress became clear through Fitch’s 60-day delinquency index, which reached a record high of 6.90% as of the January index reading, which cover the December 2025 collection period. That’s up from 6.45% a year earlier and well above the pandemic trough of 2.58% in May 2021.

Fitch indicated the trailing 12-month (TTM) delinquency rate average increased to 6.25% from 5.98%, driven by collateral deterioration and composition effects as stronger pre-pandemic vintages amortized and were replaced by weaker post pandemic cohorts.

“Performance weakness was most acute in the 2022–2023 vintages, which were originated during a period of market expansion and comparatively looser underwriting standards,” analysts said in the report.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

“These cohorts were later exposed to rising debt servicing burdens, elevated cost of living pressures, and declining used vehicle values. In response, lenders tightened underwriting beginning in late 2022 through higher minimum FICO thresholds, lower loan to value caps, and enhanced income verification, with some platforms pausing or curtailing originations,” analysts continued.

Fitch pointed out that performance in the 2024–2025 vintages has improved, although credit metrics remain elevated relative to pre-pandemic cohorts.

“Losses continued to rise alongside delinquencies in 2025, though at a slower pace, consistent with elevated delinquency churn in which a meaningful share of borrowers cured rather than progressed to default,” analysts said.

Fitch determined annualized net losses reached 9.81% as of the January 2026 index, up from 9.51% a year earlier, while the TTM average rose to 9.00%, representing a post pandemic high and the upper end of the historical range for the index.

Analysts went on to mention that recovery rates remained weaker than pre-pandemic norms and materially below those observed in prime. They explained the rates benefited from tariff related used vehicle demand in early 2025, “as collateral pools typically consist of older, higher mileage vehicles with limited secondary market appeal.”

Fitch’s recovery index ended 2025 at 32.64%, up from 31.84% at the close 2024 but well below the pre-pandemic average of 43.73%.

Analysts added the TTM average declined slightly to 37.02% from 37.92% a year earlier.

Fitch wrapped up the discussion with another notable trend in 2025. Analysts spotted accelerating deterioration within deeper subprime cohorts, which underperformed the broader subprime auto ABS index.

“Transactions with higher exposure to thin file and undocumented immigrant borrowers experienced greater stress, reflecting income disruption and payment discontinuity following immigration related borrower departures from the U.S.,” analysts said.

“High profile lender bankruptcies, including Tricolor Holdings (not rated by Fitch) driven by idiosyncratic governance and fraud issues, together with additional subprime lender bankruptcies and origination pauses in the second half of 2025, intensified investor scrutiny of subprime collateral quality and servicer continuity risk,” they continued.

Fitch also indicted seasonal tax refunds supported a temporary improvement in March, with delinquencies declining to 6.11%, annualized net losses easing to 8.80%, and recoveries increasing to 37.48%.

“This improvement is expected to be short lived, as subprime borrowers remain exposed to elevated cost of living pressures, high debt servicing costs, and a cooling labor market, contributing to renewed performance deterioration through 2026,” analysts said.

“Rating upgrades of subordinate notes are expected to persist for most transactions, supported by performance within initial loss expectations, continued credit enhancement build, and rapid amortization,” they added.