Reviewing FICO & FSA data to see how much student loans could be impacting your auto-finance portfolio

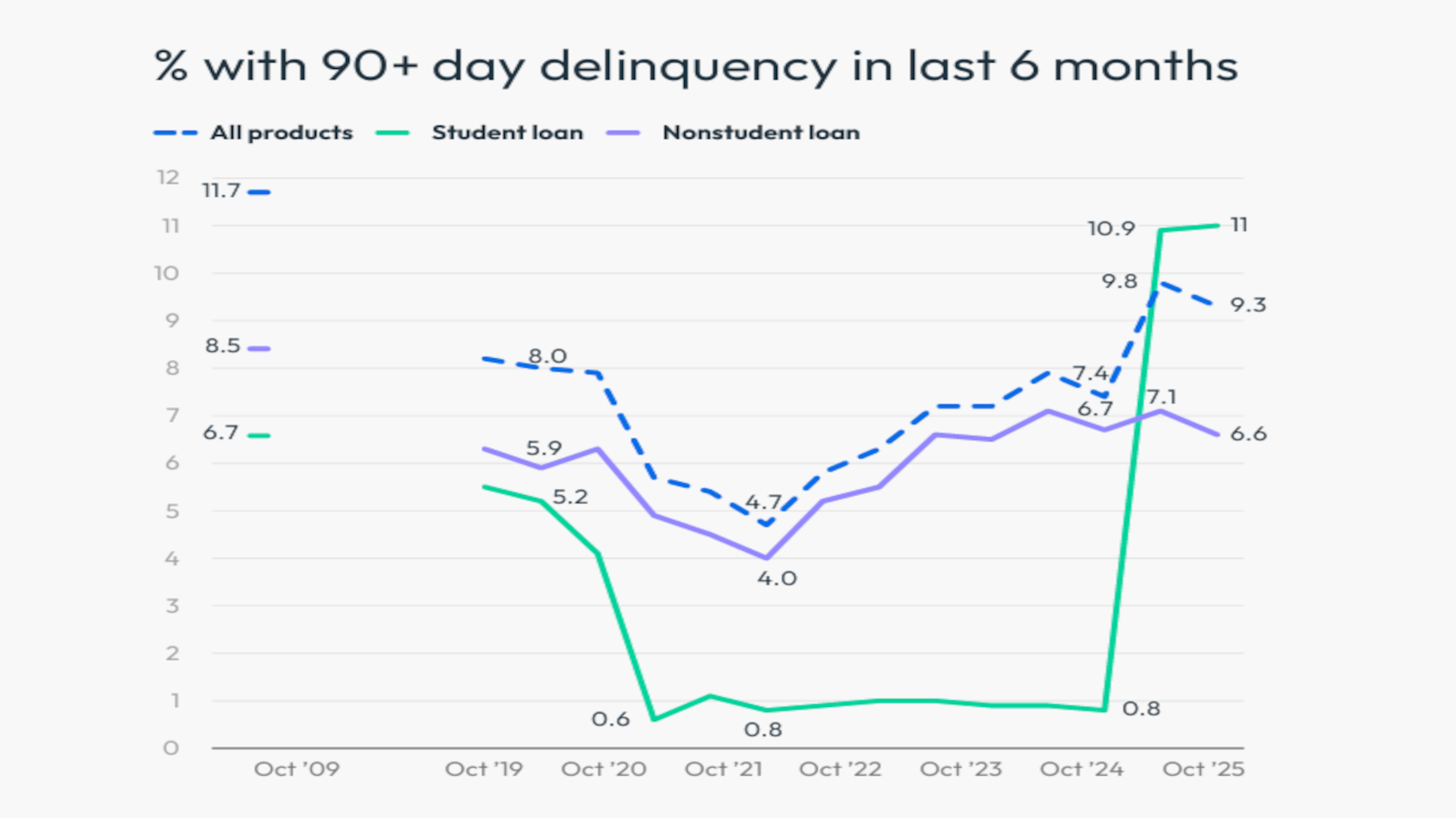

Chart courtesy of FICO.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Information from FICO and the Federal Student Aid Data Center showed how much student loans could be impacting your underwriting as well as your outstanding auto-finance portfolio.

According to a spring update, the FSA Data Center indicated that the outstanding federal student loan portfolio includes 42.8 million recipients with outstanding loans totaling $1.7 trillion, as of the end of 2025.

What’s perhaps more concerning for auto lenders is the default data connected with student loans.

Federal officials pointed out the fourth quarter of 2025 was the first time that many borrowers’ accounts could potentially become 360 days delinquent, following the payment pause created by the pandemic. Officials explained that although the payment pause ended in September 2023, the on-ramp program continued to regularly cure delinquent borrowers’ accounts through October 2024.

As a result, the FSA Data Center showed approximately 7.7 million recipients with $180 billion in outstanding federal student loans are in default, representing 11% of the total $1.61 trillion portfolio as of December.

With those metrics in mind, FICO discussed the implications in spring edition of FICO Score Credit Insights, noticing student-loan delinquency is leveling after initial jump in early 2025.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Analysts discovered nearly one-third of student loan borrowers with a payment due (7.1 million consumers) have a new delinquency reported on their credit file, causing a 62-point drop in their score on average since January 2025.

FICO said approximately 5% of student loan borrowers (1.1 million consumers) are still in an in-between status: No new delinquency has been reported on their credit file, but payments are due.

“Some of these consumers could be waiting for approval for income-based repayment plans or some other type of deferment,” analysts said in the report, mentioning that the remaining population of student loan borrowers (13.8 million consumers) have no delinquency and made at least one student loan payment in the last year.

Looking for a positive element to this situation?

After severe delinquency on student loans took a big jump in April 2025 due to resumption of delinquency reporting, FICO noted that there was only a 0.1% increase in student loan delinquency between April and October 2025.

Severe delinquency on non-student loan products decreased in October 2025 to 6.6% from 7.1% in April 2025, according to FICO.

“Many consumers may not have prioritized student loans over the last two years, because the forbearance and on-ramp periods meant that many borrowers hadn’t made payments since 2020 (or ever, if they opened their student loan after 2020) and were unfamiliar with the process of paying, the lack of consequences of nonpayment, and servicing issues,” FICO said in its report.

“With the federal government potentially beginning collections and wage garnishments on defaulted student loans in the future, we will be monitoring whether student loans remain at the bottom of the payment hierarchy going forward,” analysts added.

Here’s likely why FICO is watching student-loan activities.

The FSA Data Center showed that more than 76% of student-loan recipients with loans in active repayment are current (on time or less than 31 days delinquent) on their federal student loan payments, as of December.

Officials pointed out active repayment considers only those whose loans are in a repayment status and excludes borrowers in other statuses that would not require a monthly payment.

However, officials also acknowledged 23.2% of recipients, or more than four million individuals with student loans, are more than 30 days delinquent on their accounts. This includes approximately 1.8 million recipients in late-stage delinquency who are at risk of defaulting in the next six months.

Furthermore, the Federal Trade Commission is monitoring nefarious activities associated with consumers who are having trouble making student-loan payments.

The FTC recently obtained a temporary restraining order against an alleged student loan debt relief scheme and its operators over allegations they pretended to be affiliated with the U.S. Department of Education or loan servicers and falsely promised student loan debt relief that did not exist in exchange for illegal upfront fees.

The FTC’s complaint against NERD Solutions, ED REF, and their operators, Natalie Rodriguez and Pablo Ortiz, alleges that, since at least February 2022, the defendants illegally marketed student loan debt relief services by cold calling consumers, thousands of whom are on the National Do Not Call list, and pretending to be affiliated with the U.S. Department of Education or consumers’ actual loan servicers.

The complaint said that the defendants then used false claims of student loan forgiveness to lure consumers into paying illegal upfront monthly fees as high as $1,400.

The complaint also alleged the operators of the scheme have collected at least $8.8 million from consumers that are already burdened with student loan debt.

According to a news release, the defendants are charged with violating the FTC Act, the Telemarketing Sales Rule, the Impersonation Rule, and the Gramm-Leach-Bliley Act.