Subprime share pushes Dealertrack Credit Availability Index to highest reading in nearly 4 years

Chart courtesy of Cox Automotive.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

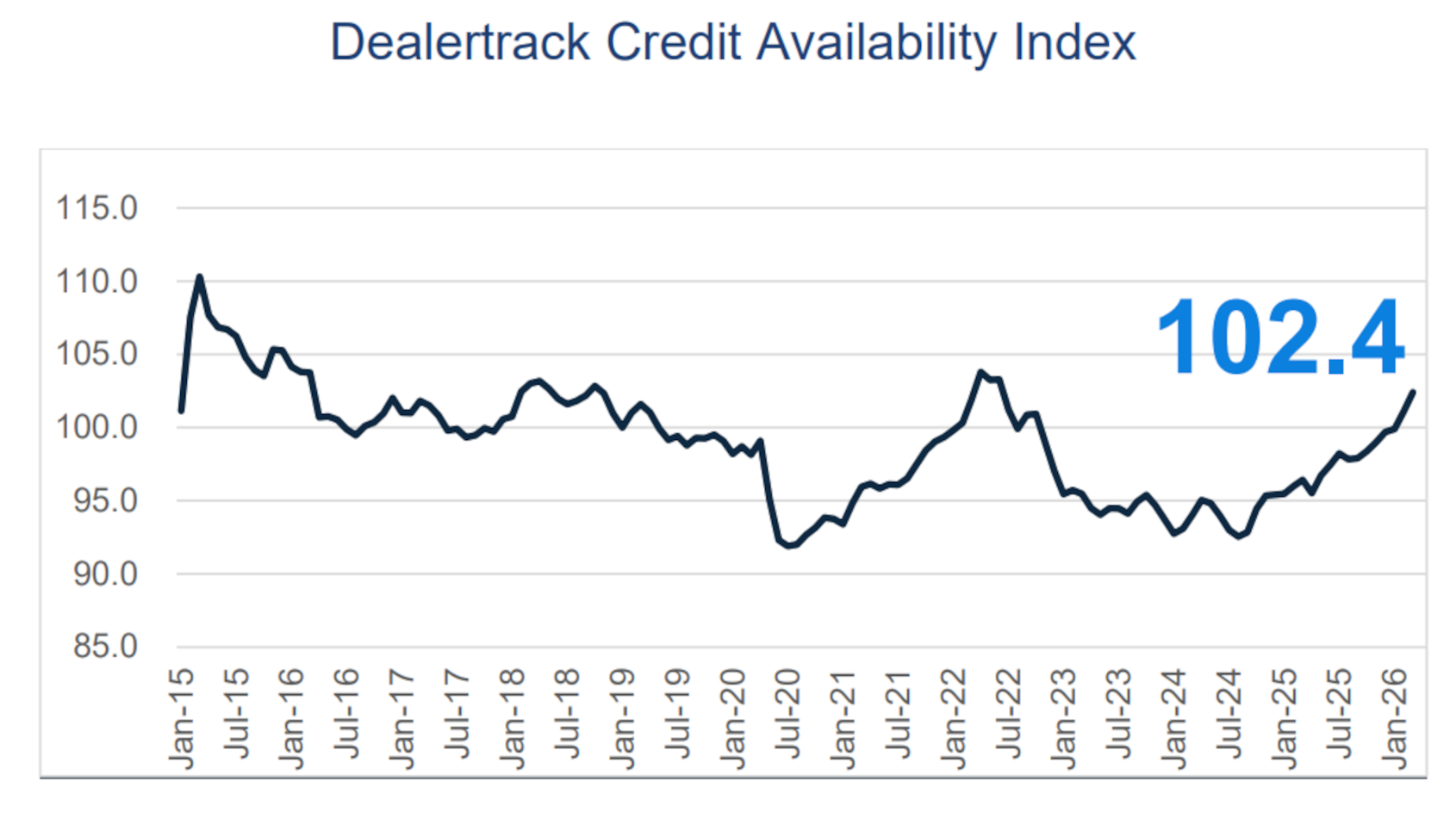

Cox Automotive reported last week that the Dealertrack Credit Availability Index rose to 102.4, which is the highest reading since June 2022.

And Jonathan Gregory pointed to the subprime share as one of the primary catalysts.

The senior director on Cox Automotive’s economic and industry insights team said the share of financing to subprime consumers in March increased by 200 basis points month-over-month from 17.5% to 19.5%. Gregory added the share has spiked 300 basis year-over-year to land at the highest level in the Cox Automotive database since March 2020.

“This sustained expansion suggests lenders are increasingly comfortable extending credit to higher-risk borrowers,” Gregory wrote in an analysis that accompanied the Dealertrack Credit Availability Index, which tracks six factors that impact auto credit access.

To reiterate, the six factors that contribute to making it cheaper and easier for consumers to obtain financing or more expensive and harder include:

—Contract approval rates

—Subprime share

—Yield spreads

—Term length

—Negative equity

—Down payments

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

While the subprime share rose both sequentially and year-over-year, Cox Automotive noticed mixed approval-rate movements.

Gregory reported the approval rate in March jumped 40 basis points from February to 70.8%, stopping a streak of two consecutive months of declines. But he said the rate is still 180 basis points lower than a year ago, “even as most lenders continued to expand access broadly.”

Turning next to yield spread, Cox Automotive calculated it widened by 31 basis points (from 7.53% to 7.84%), while the average contract rate rose 50 basis points (from 11.2% to 11.7%). And Gregory noted the five-year U.S. Treasury yield increased by 17 basis points (from 3.68% to 3.85%).

“This widening spread represents less favorable pricing for consumers and may reflect lenders charging a premium to offset the increased risk from higher subprime lending and elevated negative equity,” Gregory wrote.

Speaking of negative equity, similar to findings recently shared by Edmunds, Cox Automotive also spotted how much this metric is deteriorating.

In fact, analysts saw negative equity in March hit an all-time high for the third month in a row, rising 120 basis points month-over-month and a whopping 620 basis points year-over-year to 59.2%.

Gregory acknowledged negative equity is “signaling increased risk as more borrowers carry loan balances that exceed their vehicle’s value.”

And consumers aren’t necessarily bringing more funds to the delivery table to offset potential negative equity.

Cox Automotive indicated the average down payment percentage in March increased by 30 basis points but decreased by 80 basis points year-over-year, coming in at 13.9%.

“This modest increase may reflect lenders requiring slightly more upfront capital or consumers voluntarily putting more down, though down payments remain below year-ago levels,” Gregory wrote.

Finally, while the share of contract with terms longer than 72 months decreased by 50 basis points in March, Cox Automotive determined the metric soared 510 basis points higher year-over-year to 28.8%. That’s second-highest reading in the company’s database “and continues to reflect ongoing affordability pressures as consumers opt for longer terms to manage monthly payments,” Gregory wrote.

Gregory wrapped up his commentary by reviewing the March data through the prism of both consumers and lenders, beginning first with the individuals taking on the financing commitment.

“Credit access continued to broaden in March, with improvement across all channels and lender types offering financing opportunities in both new and used markets,” Gregory wrote, “However, the underlying picture carries increasing caution.

“Record negative equity, a sharply rising subprime share, and widening yield spreads all point to elevated borrowing costs and greater long-term financial risk. Consumers should carefully consider the full terms of any financing offer, particularly total loan length and overall cost,” he continued.

And here are the views germane to credit providers.

“Banks led the market in March, posting the strongest monthly gain among lender types,” Gregory wrote. “Captives also continued to improve, with their index reaching its highest level since April 2022, while credit unions reversed their prior month’s decline.

“With negative equity reaching a new all-time high, lenders increasing exposure in this environment face growing collateral risk, and balancing volume growth with disciplined underwriting will be increasingly important as these risk indicators continue to build,” he went on to note.