Uncertainty permeates newest auto-finance & economic projections

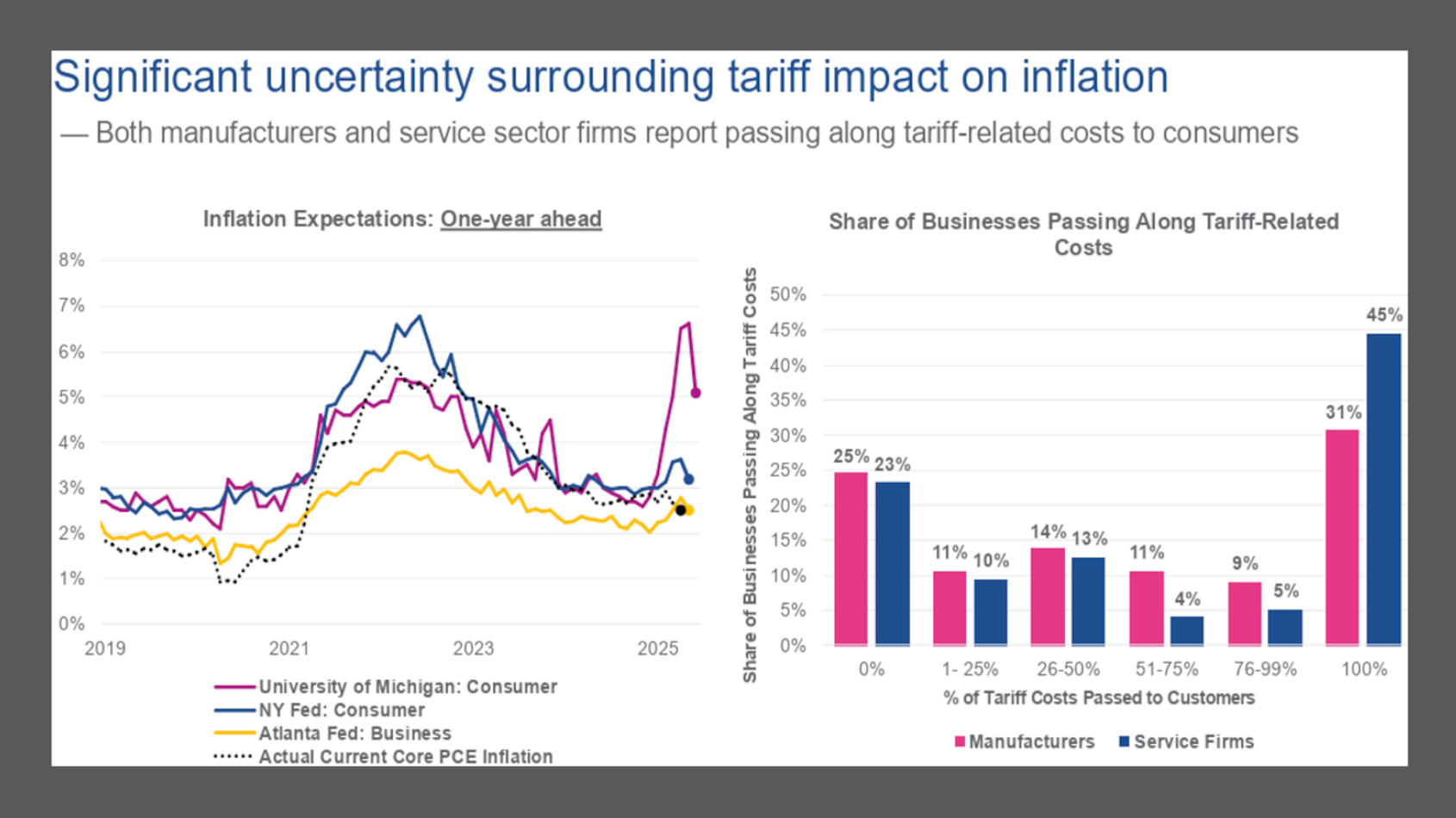

Chart courtesy of Experian.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

Economic experts from Cox Automotive, Experian and S&P Global Ratings keep using a word that might not reassure dealerships and finance companies about their roads ahead.

Uncertainty.

Four separate reports from the three firms discussed some cracks forming in the labor market, the unlikelihood of an interest rate cut coming before this ongoing heat wave subsides, and the possibility of other changes in the credit market.

“The Fed remains on hold as it monitors inflation and labor data,” Cox Automotive chief economist Jonathan Smoke wrote in his weekly update. “The Fed’s updated forecasts reflected a more pessimistic outlook: slower economic growth, higher inflation, and rising unemployment. Policymakers are unlikely to cut rates before year-end, especially as they await clearer inflation signals and labor market trends.

“Auto loan rates are unlikely to ease anytime soon as the Fed holds steady amid a more pessimistic economic outlook,” Smoke added.

Meanwhile, S&P Global Ratings indicated tariff-related concerns continue to cloud the outlook for North American credit conditions, with the reconciliation bill working its way through Congress, adding to uncertainty.

Subscribe to Auto Remarketing to stay informed and stay ahead.

By subscribing, you agree to receive communications from Auto Remarketing and our partners in accordance with our Privacy Policy. We may share your information with select partners and sponsors who may contact you about their products and services. You may unsubscribe at any time.

At the same time, S&P Global Ratings pointed out this week that U.S. involvement in the Israel-Iran conflict — and the fragility of a ceasefire — heightens the risk that tensions will escalate and disrupt the capital and global energy markets and economic activity.

“Against this backdrop, market volatility could return and push investors into a ‘risk-off’ stance that would raise borrowing costs and disrupt the typical flow of capital,” said David Tesher, S&P Global Ratings’ head of North America credit research. “Borrowers at the lower end of the credit spectrum have the most to lose in the event of an economic slowdown.”

In another update, S&P Global Ratings Economics forecasted below-potential U.S. real GDP growth of 1.7% in 2025 and 1.6% in 2026 as growth is restrained by slower population growth, tariffs, and the federal government’s cost-cutting initiatives.

Analysts said tariffs will settle below their April peak in the coming months but still materially higher than 2024. Therefore, S&P Global Ratings Economics anticipates core consumer price inflation of 3.0% to 3.5% by the end of the year.

S&P Global Ratings Economics also expects the Fed funds rate will be 3.75% 4.00% by end of this year and will reach its nominal neutral of 3.00% to 3.25% by end of 2026.

“We expect weaker growth in the near-term to soften the labor market further in the next 12 months, with the unemployment rate rising to 4.6% by the first half of next year before gradually returning to its long-run average of 4.1% by mid-2027,” said Satyam Panday, S&P Global Ratings chief economist for the U.S. and Canada.

And consumers are already carrying a record amount of debt.

According to the new CreditGauge published this week by VantageScore, the average credit balance for an individual — including auto finance, credit cards and mortgages — rose to $106,000 in May.

That figure represented an increase of $249 or 0.24% from April, marking the fifth straight month at a five-year high. Year-over-year, balances grew by $1,479 or 1.4%.

What does it all mean?

Experian chief economist Joseph Mayans and economic analyst Josee Farmer offer their assessment and projections in their newest Lending Conditions Chartbook.

“Despite early concerns over a tariff-induced recession in 2025, the U.S. economy has so far resisted a broader slowdown and significant inflationary impulse. However, the outlook remains highly uncertain, and the full impact of policy changes may still be ahead of us. In their latest set of projections, Fed officials reduced their growth forecast for 2025 while at the same time lifted their forecast for unemployment and inflation. Officials continue to see two 25bp rate cuts in 2025,” Mayans and Farmer wrote.

“Unemployment remains low, but there are ongoing signs of softening in the labor market,” they continued. “Early layoff (WARN) notices have risen, and employment gains for higher-wage industries have continued to weaken. Higher-wage, white-collar workers, along with recent college graduates are likely to continue facing headwinds as companies deal with an uncertain economic environment and increasingly take up the use of AI to replace some tasks.

“Real incomes have improved somewhat after softening for most of 2024, which may continue to support consumer spending. However, while overall spending remains solid, there are signs that higher-income consumers — which are the primary drivers of spending — are starting to pull back,” Mayans and Farmer went on to say.