Working with customer disputes isn’t an unfamiliar situation to most buy-here, pay-here operators. Dealers have become accustomed to smoothing out situations about repairs, payments and a host of other issues.

Another customer concern happening more often stems from individuals who had their vehicle repossessed and the loan balance forgiven (or discharged under state law). That process forces operators by federal law to file with the IRS and send to the borrower Form 1099-C showing that the discharged balance is considered income potentially subject to tax. These customers are notified by the Form 1099-C that they may have a significant tax liability when they file their individual return, despite losing ownership of their car.

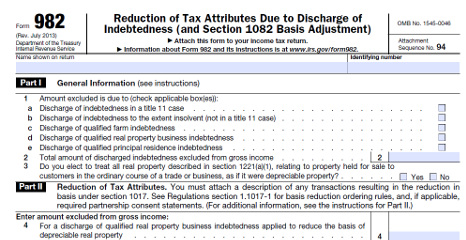

However, there is an IRS form that may brighten the day for both the upset customer and the BHPH operator — Form 982 titled, “Reduction of Tax Attributes Due to Discharge of Indebtedness.” If the customer is insolvent immediately before the debt is cancelled and the car is repossessed, the amount reported on the Form 1099-C is not taxable. For this purpose, a customer is insolvent if all of his/her liabilities were more than the value of all assets (including the repossessed car) immediately before the debt was cancelled.

Ken Shilson, founder of the National Alliance of Buy-Here, Pay-Here Dealers who spent decades as a practicing certified public accountant, recently mentioned Form 982 to some veteran operators who were unaware of the potential impact of customers utilizing this process.

“When they hear about it, they say, ‘That’s genius.’” Shilson said.

Potential of Form 982

McGladrey’s Scott Ruby explained to BHPH Report what Form 982 is in a nutshell.

“The income tax law has an insolvency exclusion that says that if your liabilities exceed your assets, you are probably excused from paying tax on cancelled debt,” Ruby said.

Especially in deep subprime where many BHPH customers reside, insolvency might be extremely common. Ruby shared information from the Taxpayer Advocate Service, which is an independent organization within the IRS aimed at making sure that every taxpayer is treated fairly. Each year the Taxpayer Advocate makes a report for Congress that lists changes that the IRS should consider.The 2010 Annual Report to Congress indicates that many taxpayers overlook the

benefit of the insolvency exclusion.

“Based on a study done by the Taxpayer Advocate Service, 47 percent of the taxpayers that received a Form 1099-C would likely qualify for the insolvency exception,” Ruby said. “Our expectation, because this is deep subprime, is that we’re probably talking about an insolvency figure much higher than 47 percent. I expect in deep subprime the level may be as high as 90 percent.”

The bottom line, customers who receive a Form 1099-C probably do not have to pay additional income taxes.

Shilson agreed with Ruby’s estimation.

“When I mentioned the exception to a couple of dealers, they responded by saying nearly everyone in deep subprime is insolvent,” Shilson said.

However, an accounting professional as experienced as Ruby cautioned about the potential pitfalls of Form 982.

“I think that the form is unbelievably confusing” Ruby said. “Customers probably want to talk to their tax accountant to help them compute the amount of their insolvency. If they are insolvent, some or all of the income may be excluded from taxable income. Their tax savings are probably going to far outweigh the cost of the tax preparation.”

Ruby suggested that operators can include Form 982 (and its instructions and worksheets) to customers along with the Form 1099-C, or instruct customers on how they Can obtain it from the IRS.

“You can have a simple handout at the dealership saying, ‘We can’t provide tax advice, but ask your tax advisor and if the Form 1099-C amount can be excluded from income under the insolvency rules.’ Tax preparers are generally pretty busy this time of year and it can be easy to overlook this exception. Sharing this simple phrase ‘please check the insolvency rules’ will be a helpful clue your tax advisor.” Ruby said.

Helping Customers in Financial Trouble

As explained in previous installments in this BHPH Report series, operators who have a related finance company are required by federal tax law to send Form 1099-C when an uncollectable balance has been discharged.Shilson described how BHPH operators can Point to Form 982 to potentially help a customer who experienced an extreme financial hardship such as divorce or mounting medical expenses, causing the repossession and eventual charge-of .

“That’s the customer you want to have this exception,” Shilson said.

And at the same time, Shilson pointed out that operators also can use the power of Form 1099-C. For example, it might be beneficial when some customers default on their installment contract and skip with the vehicle or if a competing dealer sells them a different vehicle and encourages them to abandon the old obligation.

Shilson said these “abandonment” situations have happened more frequently in the current highly competitive environment where deep subprime buyers are being offered newer vehicles by competitors.

“They deserve to get a Form 1099-C.That’s the customer you want to have a tax liability,” Shilson said.

The National Independent Automobile Dealers Association made sure to craft a detailed response when the Consumer Financial Protection Bureau allowed time for comments regarding possible changes to federal rules governing debt collection. Regulators sought the input as they consider the option of changing rules that enforce the Fair Debt Collection Practices Act.

NIADA regulatory counsel Shaun Petersen expressed the association’s opposition to rules designed to regulate creditors such as buy-here, pay-here dealers in the same way as third-party collectors. Petersen noted that when Congress passed McGladrey the FDCPA in 1977, he said lawmakers deliberately excluded creditors from the law’s requirements.

“In November the CFPB released what they call an advanced notice of proposed rule making (ANPR). In essence, what the ANPR is the agency is alerting the world, ‘We’re thinking about doing rules in the arena, and here are some of the questions that we’re asking internally and externally.’ They ask for interested parties to respond back based upon these questions relative to them,” Peterson said in an interview with BHPH Report.

“There were certainly things included in that group of information that wasn’t germane to us as buy-here, pay here dealers, but there were other things being said that were very much of interest to us,” he continued. “Our process, certainly we get input from our board.We get some of their thoughts. We talked to other members of the association, in particular buy-here, pay-here folks, on this particular issue.

“We got some good input from dealers that would be affected by any change that the CFPB would make if they started to change things that impacted creditors collecting on their own debts. That was our primary concern,” Petersen added.

Addressing Specific CFPB Questions

NIADA’s comments covered nearly a dozen specif c questions offered by the CFPB. Petersen of en referenced language contained in the FDCPA to articulate the association’s concerns.

“Congress believed the risk of reputational harm to the creditor is sufficient to deter the creditor from engaging in the types of debt collection practices the FDCPA intended to prohibit,” Petersen wrote to the CFPB. “NIADA believed then and continues to believe that Congress’s logic is sound. Dealers collecting their own debt are deeply concerned about their reputation." Petersen explained that BHPH dealers “will often go to great lengths to ensure a positive customer experience,” including spending their own money to repair customers’ vehicles because “experience has shown that often, if a customer’s car breaks down at any point while a loan balance exists, the risk that the customer ceases to make the required installment payments increases dramatically.Thus, dealers invest heavily in the postsale customer relationship as an incentive to repayment.”

In addition, Petersen said the CFPB provided no evidence or statistics that showed first-party auto loans — or any auto loans — are a source of debt collection concerns, or even a significant source of debt collection activity.

NIADA provided input on other issues, as well, opposing unnecessary burdens such as a debt verification process for first-party auto lenders, who have a direct relationship with the customers from which they are collecting.

Meeting with Bureau Officials

Along with the comments, Petersen along with NIADA executive vice president Steve Jordan visited with CFPB officials earlier this month. Petersen described the encounter as quite positive.

“We were very clear that we’re very much interested in working with them in anything that they do in the debt-collection sphere, in the military relations sphere and the hot issues that were communicated at (the Vehicle Finance Conference hosted by the American Financial Services Association) with the fair lending issues and disparate impact,” Petersen said.

“We want to be a tool and a resource for the bureau and what they’re doing to gather information about the industry and certainly as they make decisions that would impact the regulations of the industry and especially the enforcement of those regulations on the industry.We want to be abreast of those issues and to let them know we can be a resource for them,” he went on to say.

Signal of What Might Be Ahead

At the same time, while no official rule change proposal has been made by the CFPB, Petersen is hoping BHPH dealers will maintain current practices and be aware that they might have to be altered depending on what federal regulators do.

“I feel confident that the buy-here, pay-here industry is aware of the ‘common-sense’ things you could do when collecting on your own debt that could be construed as abusive, things like threatening people with criminal action. I would hope that the vast majority of them would understand those are practices that nobody condones,” Petersen said.

“What we are hopeful for and what we’re spending a lot of time as an association is to educate and this response to rule making,” he continued. “Look, this is something the CFPB is just collecting comments on right now.There’s been no proposed rule. There’s been no statutory change in regulation. They’re just gathering information. But this is the first step.

“This should be the blinking light on the horizon saying here’s where we’re going and it’s something to be aware of,” Petersen went on to say. “I guess I almost liken it to that this is the lighthouse and the ship in the ocean sees the lighthouse. The details aren’t there until you get a little closer. Then you get the light along the shore to point out the details of the rocks. But certainly the advanced notice of proposed rule making is that lighthouse where I can see something on the horizon is coming. The next step is to see if the CFPB decides to go down that road and propose specific rules in very detailed language to say this is how they’re going to regulate.

Petersen indicated to BHPH Report that There is no specific timetable as to when the CFPB may propose rules changes regarding the FDCPA. For now, he is waiting just like the rest of NIADA and the BHPH industry.

“I’m sure the CFPB will take whatever appropriate time they feel they need to consider comments that have been submitted,” said Petersen, who added that more than 300 comment submission were made by consumers, industry groups, service providers and other interested parties.

“They certainly have some study time.We’ll see if they make any proposed rule changes. We certainly hope they don’t,” he added.