Andy Koblenz, executive vice president and general counsel for the National Automobile Dealers Association, heard leaders from the Consumer Financial Protection Bureau speak last week and again left with questions about how the new regulatory agency intends to oversee vehicle financing.

Koblenz indicated during a panel session of an event hosted by the U.S. Chamber of Commerce that two points struck him during earlier remarks from CFPB deputy director Steve Antonakes.

“He talked about their commitment to providing clear rules of the road. And yet when you look at the indirect auto lending area, every indirect auto lender that I’ve spoken to when I asked them if they understand what the methodology that the CFPB is using for their disparate impact analysis, whether it’s the proxy methodology of the statistical controls methodology, they all say no and they’re still guessing at it,” Koblenz told attendees at the eighth annual Capital Markets Summit orchestrated by the chamber’s Center of Capital Markets Competitiveness.

Koblenz acknowledged that Antonakes stated the bureau intends to be more forthcoming on how it plans to exercise its methodology. Koblenz offered an analogy to show the quandary finance companies face nowadays.

“It’s almost like the cop standing by the side of the road and pulling people over for speeding. Someone says I want to comply and the cop says I’m not going to tell you. I’ll look back after the fact and tell you if you were speeding or not. That’s not fair and it’s ultimately going to drive credit out of the market,” Koblenz said.

With last Friday marking the one-year anniversary since the CFPB issued its guidance into how indirect auto lending operations are supposed to operate, Koblenz noted that he perked up again when Antonakes insisted the CFPB is an evidence-based organization

“They’ve chosen to address issues in the indirect auto lending model through the issue of guidance. Yet they didn’t conduct any rulemaking. They didn’t take any public comment. They didn’t receive any input from the industry from any of the players in the industry and I think it’s led to some bad outcomes,” Koblenz said.

“Their solution to the indirect lending model and to address concerns if they exist in the fair lending world is to drive the industry to an indiscretionary, flat-fee model. But had they conducted rulemaking, they would have received comments saying that flat fee doesn’t eliminate discretion because the dealers don’t have the choice of which lender to work (with), so you would have interlender discretion not intra-lender discretion. You simply can’t eradicate discretion if that’s the cause of the problem by going to a flat fee,” he went on to say.

Koblenz’s fellow panelist raised issues not only with how the CFPB’s guidance arrived but also how the bureau is taking enforcement actions against only a small handful of institutions. Those points came from Andy Navarrete, senior vice president and chief counsel at Capital One.

“There are 5,000 auto lenders in this country. Tackling individual institutions via supervision enforcement may change behaviors at those individual companies but it’s not going to move markets in a way that produces consistent rules of the road for the industry, clear expectations of dealers and clear results and predictable outcomes for consumers,” Navarrete said.

Koblenz closed by reiterating NADA and other associations contend there are solutions available “that both address fair lending risk and retain competitive and flexibility in the marketplace but the bureau’s guidance approach seems to be turning down the opportunity.”

The NADA legal expert added, “There are reasonably reliable studies that show in the auto lending arena the ability to get an auto loan is clearly a step up the ladder of economic progression. The difference between having a car and not having a car means the jobs that are available to you are the ones on the public transportation grid. With a car, the universe of jobs expands dramatically. During the financial crisis we heard stories from people who gave their mortgage back to the bank but paid on their car loans because ultimately they could sleep in their car but couldn’t drive their house.

“The access to credit in our industry is really a step up the economic ladder. It’s a point we need to remind people to overcome this demonanization that has happened over the last few years,” Koblenz went on to say.

To mark “Sunshine Week,” a national initiative launched by the media to promote open government, U.S. House Financial Services Committee chairman Rep. Jeb Hensarling is calling on Consumer Financial Protection Bureau director Richard Cordray to end the bureau’s closed-door meeting policy for its four advisory councils.

Hensarling, a Texas Republican, said earlier this week, “Instead of operating behind closed doors, it’s time for the CFPB to live up to its oft-stated commitment to transparency and openness.

“In the interest of true, genuine transparency and open government, director Cordray can and should use ‘Sunshine Week’ to take immediate steps that bring the CFPB into the sunlight,” Hensarling continued.

The committee chairman pointed out the Bipartisan Policy Center also criticized the CFPB for closing its advisory group meetings to the public.

The CFPB claims on its website that “Transparency is at the core of our agenda …You deserve to know what we’re doing for the American public and how we are doing it.”

However, Hensarling noted four advisory groups created by the CFPB conduct “virtually” all of their business behind closed doors — refusing requests by members of the public and even a member of Congress to attend them.

The meetings are also closed to the press.

For example, Hensarling mentioned the agenda for the CFPB’s Consumer Advisory Board’s last meeting shows only two hours out of two days’ worth of meetings were open to the public.

Rep. Sean Duffy, a Wisconsin Republican and a member of the Financial Services Committee, requested to attend the Consumer Advisory Board’s February meeting. The CFPB’s advisory groups — which include the Community Bank Advisory Council, the Credit Union Advisory Council, and the Academic Research Council in addition to the Consumer Advisory Board — are made up of industry representatives, consumer activists and academics.

“What goes on at these meetings? If the CFPB is as committed to transparency as it claims,” Duffy said, “then why was I denied entry when I asked to attend?”

Duffy and Hensarling recounted that Cordray has said the meetings are closed to the public because the Federal Advisory Committee Act, a sunshine law passed in 1972, does not apply to the bureau.

Yet, by law, the congressmen said, all federal agencies are subject to the act with the exception of the Central Intelligence Agency, the Director of National Intelligence, and the Federal Reserve’s Federal Open Market Committee.

“The CFPB is an independent agency housed within the Federal Reserve, but the Fed exercises no control over the CFPB or its advisory groups,” the lawmakers said.

Yet another Republican lawmaker, Rep. Robert Pittenger of North Carolina, insisted the Dodd-Frank Act that created the CFPB also does not exempt the bureau from the federal sunshine law.

In fact, Pittenger contends nothing prevents the CFPB director from opening the meetings up to the public.

Pittenger asked Cordray at a January hearing “Why deny the public the right to observe these meetings?”

During the session, Cordray replied that the advisory group meetings are closed to the public so “we can speak candidly about matters that are not yet public that the bureau is working on, including things like enforcement actions and the like.”

In a Feb. 4 letter to Cordray, Hensarling described that response as “deeply troubling.”

Hensarling went on to tell Cordray, “Confidential information related to pending investigations or enforcement actions is potentially market moving and could be used for financial gain. Consequently, I am concerned that the bureau would release confidential information to persons who do not work for the bureau and could be competitors or future legal adversaries of the party subject to the enforcement action.”

Hensarling said Cordray has yet to respond to his earlier letter.

In addition to closing the meetings to the public, Hensarling believes the CFPB instructs its employees to keep details about agency events on their work calendars to a minimum in order to shield information about their activities from the press and public.

More than eight months after Rick Hackett left the Consumer Financial Protection Bureau, the agency tapped a replacement regulator on Wednesday whose main jurisdiction is the auto finance market.

Joining the CFPB as the assistant director of installment and liquidity lending markets in the bureau’s research, markets, and regulations division is Jeffrey Langer, who most recently served as senior counsel at Macy’s in Mason, Ohio.

Langer also has served as a partner in several law firms, including Jones Day and Dreher Langer & Tomkies. He is a founding fellow and treasurer of the American College of Consumer Financial Services Lawyers and is a former chair of the Consumer Financial Services Committee of the American Bar Association Business Law Section.

Hackett spent two years at the CFPB before departing the bureau last summer. Hackett arrived at the CFPB in 2011 after being a founder of the banking and financial services group at Pierce Atwood in Maine.

“I have no hesitation in saying that my work with CFPB has been the most rewarding, most challenging and most physically tasking assignment I have had in 35 years,” Hackett said in his farewell message obtained by SubPrime Auto Finance News last year.

“Of particular importance to me are the relationships I have been privileged to develop with bureau stakeholders, who have taught me critical information about the relationship of government and its stakeholders, the complexity of policy formulation, and the importance of frank and transparent exchange of ideas,” he continued.

Hackett now is a partner at Hudson Cook, a role he started in earlier this month. Hackett is set to be one of the keynote speakers during the upcoming National Conference hosted by the National Alliance of Buy-Here, Pay-Here Dealers in May in Las Vegas.

Langer’s appointment to the CFPB post was one of three announcements the bureau made this week.

Christopher Carroll also joined the CFPB as the assistant director and chief economist for the office of research in the bureau’s research, markets, and regulations Division.

Carroll is a professor of economics at Johns Hopkins University, from which he has taken a leave of absence while serving at the bureau. He also is a member of the board of directors of the National Bureau of Economic Research, and the co-chair of the NBER Research Group on Consumption. Carroll has served as a senior economist for the Council of Economic Advisors on two separate occasions, and as an economist for the Board of Governors of the Federal Reserve System.

The bureau also announced Daniel Dodd-Ramirez joined the agency as the assistant director of financial empowerment in the bureau’s consumer education and engagement division.

Dodd-Ramirez previously served as the executive director of Step Up Savannah in Savannah, Ga., from 2005 to 2014. Prior to Step Up, Dodd-Ramirez served as education project director and community organizer for People Acting for Community Together (PACT) in Miami.

From 1998 to 2000, Dodd-Ramirez was the human resources director for Families First, a social services agency in southern Vermont.

“I’m pleased that these incredibly talented individuals have joined the bureau,” CFPB director Richard Cordray said. “All three offices play an essential role in making sure that consumers are being treated fairly. These experts will lead the teams that help us monitor the marketplace and provide tangible benefit to consumers.”

In response to dealer demand, the Association of Finance & Insurance Professionals announced the introduction of AFIP Certification Boot Camps, which include two days of accelerated preparation for the federal and state regulation-based AFIP certification exam.

The first boot camps are being offered in Cleveland, Kansas City, Mo., Scottsdale, Ariz., and Trenton, N.J., in April.

The AFIP certification course are designed to address the laws that apply to in-dealership vehicle funding and leasing and aftermarket product sales.

“As a result of recent high-dollar penalties and enforcement actions, we’ve been inundated with calls from dealers who want their people AFIP certified, but don’t want to wait the six to eight weeks it typically takes to complete the course,” AFIP executive director David Robertson said.

“The boot camp allows dealers to certify their people in a much shorter time period. We recommend that attendees spend about three weeks of independent study before the sessions,” Robertson continued.

The first day of boot camp is devoted to an intensive review of the key state and federal regulations. The second day begins with a final exam review and culminates in administration of the proctored exam.

The boot camp fee is $150, plus the cost of the AFIP certification course. Boot Camps are open to first-time, senior- and master-level candidates in AFIP’s three-tiered continuing education program.

Onsite boot camps are available to dealer groups. Managers can contact AFIP for pricing and availability.

Robertson noted the boot camp concept was originally developed to assist a national dealer group’s personnel who were having trouble completing the course.

“The methodologies implemented with this group turned out to be highly successful,” he said. “The scores and passing rates were higher than those typically achieved through the traditional course of study.

“When we started getting calls from dealers who wanted their people certified yesterday, we already had an accelerated program in place that we knew would ultimately benefit all candidates and expedite the certification process,” Robertson went on to say.

For more information about AFIP, visit www.afip.com.

AFIP Announces $1,000 Scholarship Winner

In other news, Christina Robertson, AFIP’s corporate counsel and director of education said the recipient of the $1,000 Jakob Murray Lange Memorial scholarship went to Luke Flannery, a Northwood University automotive marketing major from Bad Axe, Mich.

Robertson noted Flannery earned the scholarship for his exemplary achievement as a dealership intern last summer.

Flannery interned at Bill Marsh Automotive Group in Traverse City, Mich. The full service dealership operates on four campuses and sells new and used Buick, GMC, Chrysler, Dodge, Jeep, Ram, Hyundai and Ford vehicles.

According to general sales manager Dan O’Connor, “We first connected with Luke in a roundtable discussion on campus. I was very impressed with his professionalism and knowledge of the business. He later approached us about internship opportunities. We’d never had an intern, but decided to take Luke on last summer.

“Luke spent time in every department on all four campuses — sales, service and parts, the body shop, centralized reconditioning, marketing, accounting and J.D. Byrider — plus time on the job shadowing me,” O’Connor continued.

“Our experience with Luke went beyond our expectations,” O’Connor went on to say. “He was always prepared, conducted himself in a very professional manner and was a ‘sponge’ to all things Bill Marsh. He not only became a part of our team, by the end of the summer Luke was contributing in leadership meetings and truly had an understanding of our philosophy and culture.

“I’d like to thank Elgie Bright for his dedication to the young students coming out of Northwood. He’s a great role model and example to the next generation of automobile professionals,” O’Connor added.

This is the second year AFIP has awarded the scholarship, recently named to honor a gifted AFIP staff member, Jakob Murray Lange, who died in a car accident last year.

A plaque recognizing the scholarship recipients is on display in the NADA building on the Northwood University campus.

In addition to the scholarship funds, Flannery will receive a crystalline obelisk in recognition of his achievement.

Bright emphasized that internships have been an important component of Northwood’s automotive marketing and management program for many years.

“The experience students gain working at dealerships has proven invaluable to their success in moving from the classroom to the showroom,” Bright said. “Having AFIP support our efforts through their scholarship program raises the prestige of the experience and helps boost interest in internship opportunities.

“We are grateful to Dave Robertson and the AFIP staff for all they do to support our program here at Northwood,” Bright went on say.

And David Robertson added, “As I've learned firsthand working with dealers throughout the U.S., Northwood interns are highly prized for their ability to apply the lessons learned in the classroom to the real world challenges they encounter in the dealership."

The same methodology utilized by the federal agency to levy enforcement actions against vehicle financing companies might be what could be used against the regulator, as well.

A trio of Republican House members gave the Consumer Financial Protection Bureau until Thursday to provide answers and other details to 14 different questions all stemming from recent reports of potential racial disparities in how bureau employees are treated.

Lawmakers sent the demand letter to CFPB director Richard Cordray in response to a story published last week by American Banker that cited confidential bureau documents and unnamed sources that revealed data showing that the agency’s white employees had a greater likelihood of receiving the highest rating in performance evaluations — which determine salary increases and bonuses — than minorities.

Rep. Jeb Hensarling, a Republican from Texas who is the House Financial Services Committee chairman, authored the letter that also was signed by two fellow House members, Rep. Shelley Moore Capito of West Virginia and Rep. Patrick McHenry of North Carolina.

Along with concerns stemming from the published report, these lawmakers raised questions to the CFPB in response to the most recent No Fear Act disclosure released by the bureau for the period ending Dec. 31. That disclosure revealed a number of formal discrimination claims filed by bureau employees against the agency on the basis of race, age, religion, sex, disability and national origin.

The representatives also noted concerns about the bureau stemming from its 2013 annual employee survey that indicated fewer than half of agency employees are satisfied with the policies and practices of senior leaders, that fewer than half of bureau employees agree that promotions and pay raises at the bureau are based on merit, and that fewer than three in five employees agree that they understood what they had to do to be rated at different performance levels based on their most recent performance appraisals.

Furthermore, the lawmakers goes on to mention problems identified by the bureau’s employee union, including the need for fair and transparent performance appraisals as an area of focus for ongoing bargaining between the union and the bureau.

Among the specific 14 requests, the letter asks for:

—Records depicting the aggregate number of employees receiving a rating within each category of the bureau’s five-point performance rating scale.

—Records depicting the distribution of employee performance ratings by any demographic factor/

—The number of complaints, whether formal or informal, filed by bureau employees with the agency’s Office of Equal Employment Opportunity or the Equal Employment Opportunity Commission

—The number of employee grievances that the bureau has denied and the number of employee grievances that the Bureau has denied without providing written justification for its denial.

In an opinion piece published on Sunday in the Wall Street Journal, former CFPB official Ronald Rubin traveled on the same questioning track as the Republican lawmakers who are seeking more information from the bureau.

“It seems inconceivable that CFPB’s management could be discriminating against its workers. But disparate-impact statistics equal discrimination. Or at least that’s what the CFPB tells the businesses it regulates,” Rubin wrote in the column posted here.

While with the regulator, Rubin drafted the CFPB’s enforcement action process, which governs how enforcement collaborates with other components of the bureau prior to taking steps such as opening investigations, issuing civil investigative demands, and suing suspected law violators.

Rubin closed his piece in the Wall Street Journal by stating, “Are the CFPB’s managers discriminating based on race, despite the agency's best intentions? Were the statistical disparities caused by cronyism, elitism or some other problem? A thorough inquiry should be conducted, and CFPB director Richard Cordray has already ordered one. The more important question is whether the bureau will reconsider its commitment to the disparate-impact doctrine after witnessing its flaws firsthand.”

During the same week the Consumer Financial Protection Bureau “strongly urged” companies to make credit scores more readily available, a bill passed through the U.S. House aimed at limiting the authority of the bureau, which the measure’s author called, “a dangerously powerful and dangerously unaccountable agency.”

As currently constructed, Rep. Sean Duffy, a Wisconsin Republican who authored H.R. 3193 — known as the Consumer Financial Freedom and Washington Accountability Act — indicated the bill would accomplish four objectives, including:

— Replaces the single, “unaccountable” CFPB director with an “accountable,” five-member commission appointed by the president and confirmed by the Senate to ensure that a diversity of viewpoints inform the CFPB’s regulatory and enforcement agenda, and to conform the CFPB’s governance to that of other federal agencies charged with consumer or investor protection.

— Subjects the CFPB to the regular appropriations process and makes the CFPB a stand-alone independent agency rather than a bureau within the Federal Reserve System.

— Prohibits the CFPB from using a consumer’s private, personal financial information without the consumer’s knowledge and consent. The CFPB is currently engaged in a massive, multi-million dollar data collection effort of consumers’ financial information.

— Prevents the CFPB from undermining the safety and soundness of U.S. financial institutions through regulatory overreach.

— Sets the basic rates of pay for CFPB employees in accordance with the General Services (GS) scale.

“This is a bill about accountability and transparency,” Duffy said. “CFPB director Richard Cordray claims that in order for the agency to do their job, they must monitor 80 percent of all credit cards in circulation, or nearly 1 billion credit cards. One provision in this bill would require the CFPB to first ask the American people’s permission before accessing their personal information.

“If you are here to protect the consumer, why don't you ask the consumer for permission and consent to take their information? “This is the right thing to do. Let’s empower Congress and the American people. Let’s reform the CFPB and actually make it work,” Duffy went on to say.

Duffy’s House colleague, Rep. Jeb Hensarling, a fellow Republican from Texas, cheered the developments associated with H.R. 3193. Hensarling also is the House Financial Services Committee chairman.

“We are now into the sixth year of the Obama administration and probably the two most common comments I hear from my constituents are, ‘I just can’t make ends meet in this economy,' and ‘Washington has become arrogant, unaccountable, and out of touch,’” Hensarling said last week. “And at the apex of these sentiments lies the newly minted, Dodd-Frank government agency known as the CFPB. Although many have yet to hear of it, the CFPB is perhaps the single most powerful and least accountable Federal agency in all of Washington.

“When it comes our credit cards, our auto loans, our mortgages, the CFPB has unbridled, discretionary power not only to make them less available and more expensive, but to absolutely take them away,” he continued.

“The Consumer Financial Freedom and Washington Accountability Act, whose primary author, Mr. Duffy of Wisconsin has done excellent work along with many other members of our committee, is a package of common-sense reforms designed to make the CFPB more accountable and more transparent to the American people,” Hensarling went on to say.

Along with approval from House Republicans, the bill was cheered by the National Automobile Dealers Association. In a letter to House members, NADA vice president of legislative affairs Ivette Rivera reiterated the association’s issue with the CFPB’s guidance for indirect auto lending.

“The CFPB has not studied the impact of its indirect auto finance guidance on consumers despite the fact it is likely to increase costs for consumers. Specifically, the bureau recently acknowledged that it never studied how eliminating a dealer’s ability to discount credit would affect the cost of credit paid by consumers,” Rivera said.

“According to Fitch Ratings, the CFPB’s drive to eliminate or severely limit ‘meet or beat’ financing offered by auto dealers ‘will likely raise lender regulatory costs in 2014.’ Higher regulatory costs would result in higher credit costs for consumers. As recognized by a bipartisan group of House and Senate members, lower income consumers could be priced entirely out of the credit market because of these new costs,” she continued.

If the CFPB, like other agencies, were subject to customary congressional oversight, Rivera claimed it is doubtful the bureau would have attempted to fundamentally change and regulate the $783 billion auto loan market via guidance without three components, including

— Prior public comment or hearing

— Answering direct and specific questions by Congress for nearly a year

— First assessing the impact of its guidance on consumers

“Oversight by Congress of the executive branch is an integral part of the checks and balances of our democratic system. On behalf of America’s franchised auto dealers, we urge Congress to pass H.R. 3193 to provide that needed oversight and accountability,” Rivera said.

If the Consumer Financial Protection Bureau gets it way, potential buyers who have a credit card account will already know their credit score before they walk on the lot or enter the F&I office looking to complete vehicle financing.

On Thursday, the CFPB called on the nation's top credit card companies to make credit scores and related content freely available to their customers. Before this week's announcement, bureau director Richard Cordray sent letters to this institutions, beginning with some language that triggered a pointed retort.

"I am writing to bring a matter to your attention and strongly urge action on your part," Cordray said. "We need to get more Americans to pay closer attention to their credit standing, which would benefit lenders, consumers and the national economy. You can now, relatively easily, help us achieve this goal."

Richard Hunt, president and chief executive officer of the Consumer Bankers Association, doesn't think the call for banks to "strongly consider" providing customers with FICO scores on a monthly basis is quite so simple.

"CBA supports relevant efforts to expand consumer financial awareness and understanding, but it must be both understandable and useful for the consumer," Hunt said.

"There are numerous factors considered in weighing a consumer's credit portfolio — not just a credit score," he continued. "The CFPB rightly points to the value of credit information and appears to be approaching this issue informally in order to allow each financial institution to create a workable solution. However, no institution that receives a letter from its regulatory agency ‘strongly encouraging' an action views the request benignly."

The new developments stem from a report released by the CFPB that found accuracy issues top the list of credit reporting complaints the bureau received from consumers.

The CFPB also warned companies that provide information to credit reporting agencies not to avoid investigating consumer disputes.

"Credit reports and scores can determine the terms of people's mortgages, whether they qualify for auto loans, or if they are eligible for different credit cards," Cordray said. "Making consumers' credit scores freely available on their monthly statement or online makes it easier for them to spot problems with their credit report. We will continue to work to ensure that credit report disputes are fully investigated, errors are fixed, and consumers are treated fairly."

Cordray contends a regularly available credit score may prompt more Americans to review their credit standing and pull their free annual credit report.

The bureau believes fewer than one in five Americans check their credit report in any given year.

Cordray's letter also articulates a potential reward for companies that provide credit scores regularly.

"We will consider this to be a ‘best practice' in the industry," Cordray said. "Doing so through existing channels, such as including credit scores with other online account information and on monthly statements, is likely to yield positive returns that outweigh the limited effort involved.

"Customers who monitor and manage their credit standing may be less likely to become delinquent or to default," he continued.

The bureau insisted most Americans have a credit file. Because of the significance of these reports, consumer reporting agencies have been a major focus for the CFPB.

Regulators acknowledge the three biggest credit reporting companies — Equifax, Experian and TransUnion — each maintain files on more than 200 million consumers. These files are based on information supplied by thousands of providers also known as data furnishers.

"This financial score keeping exerts a tremendous and growing influence over consumers' lives," Cordray said in remarks to the CFPB's Consumer Advisory Board. "The amount of data collected and exchanged in the credit reporting industry is astounding. Each year, approximately 36 billion updates are made to consumer credit files at the three largest credit reporting companies alone. Assuring that such personal financial information is updated timely and accurately, and that it is maintained securely, is a critical responsibility."

Cordray closed his commentary by reiterating how regular access to credit scores will make the situation better for consumers and finance companies.

"At the bureau, we are dedicated to fostering a marketplace for financial products and services where sensible practices benefit both industry and consumers alike," Cordray said. "As the American economy continues on its path to recovery, we need to have confidence that consumers enjoy the full benefits of credit reports that are accurate and reliable. Consumers bear their own share of responsibility to monitor and manage their credit standing. As we have discussed, however, there are some steps that can be taken to put them in a better position to succeed in protecting themselves."

Accuracy Issues Top Credit Reporting Complaints

Between October 22, 2012 and Feb. 1, the bureau handled roughly 31,000 complaints from consumers frustrated with credit reporting companies. The majority of those complaints have been about the accuracy and completeness of credit reports.

The top three concerns include:

• Incorrect information on a credit report: Almost three-quarters of the credit reporting complaints the bureau received related to consumers believing that their credit reports contained incorrect information. Over one-third of these complaints were about incorrect account statuses — such as a debt being reported as delinquent when it was already paid. Other consumers reported having information in their credit report that did not belong to them. One consumer reported having a mortgage placed in his credit report when he was only a sophomore in high school. Other consumers found that their date of birth was listed incorrectly or a bankruptcy filing was misreported.

• Frustration with the credit reporting company's investigation: When consumers find this incorrect information, they can file a dispute directly with the credit reporting company. About 11 percent of complainants were frustrated with how the company handled a dispute they filed. Consumers expressed concern about the depth and validity of dispute investigations. Other consumers felt that the documentation they provided to dispute an item was not used in the company's investigation. The CFPB said it heard from consumers who were reported as deceased by a credit reporting company, and even after they filed a dispute, the company did not fix the report.

• Difficulty obtaining a credit report or score: About 9 percent of credit reporting complaints were about consumers who said that they were unable to obtain their free annual credit report or another copy of their credit report or score. Consumers say they feel as if they have reached "dead ends" when trying to obtain their credit reports. For example, one consumer claimed that she twice tried and failed to obtain her credit report from the three nationwide credit reporting companies.

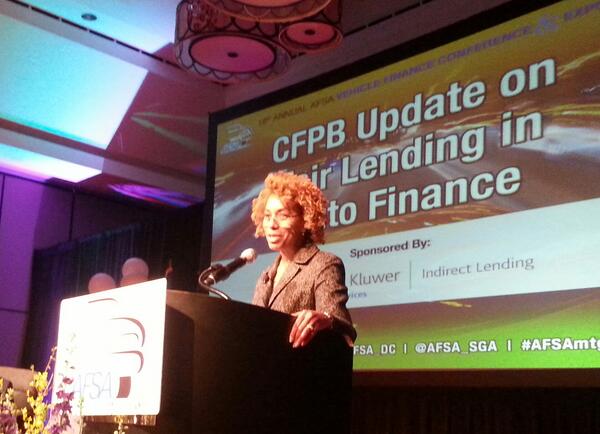

The Consumer Financial Protection Bureau reiterated its uneasy assessment of how the dealer participation system operates when one of the agency's top officials made prepared remarks and answered a handful of submitted questions during the American Financial Services Association's Vehicle Finance Conference on Thursday.

Patrice Ficklin spoke to a spillover gathering of more than 600 finance company executives, service providers and dealers about the bureau's concerns regarding how F&I managers can mark up a sales contract after the sales price, trade-in value and lender buy rates are all established.

Ficklin, the bureau's assistant director of the office of fair lending and equal opportunity, said that dealers should be compensated for arranging vehicle financing, better known as indirect lending. But Ficklin stressed that other avenues should be pursued, including finance companies switching to flat fees to compensate dealers rather than allowing stores to mark up contracts anywhere from 100 to 200 basis points.

"We have been approached by lenders about the types of compensation systems that will be acceptable to the bureau," Ficklin said in prepared remarks that lasted close to 30 minutes. "The answers really depend on the specifics of each lender's business. But we believe one factor to consider in term of evaluating compensation systems is that compensation be based on non-discriminatory terms rather than terms that require discretion to modify.

"As we've indicated, it's been our experience that permitting discretion and tying compensation to the exercise of that discretion often significantly increases fair-lending risk," she continued. "Potential alternative compensation systems could vary in design and sophistication, depending the needs of the individual lender's business."

Much of Ficklin's prepared remarks also recapped the settlement the CFPB recently reached with Ally Financial, a package of enforcement actions that included $98 million in penalties and instruction on how the company should revamp its compliance department to prevent future alleged discriminatory activities.

Following her prepared remarks, AFSA president and chief executive officer Chris Stinebert whittled down a stack of submitted questions written on index cards from attendees. Stinebert asked if the bureau's goal is to eliminate discretion altogether or to make sure it's exercised under certain parameters. Ficklin responded by citing the Equal Credit Opportunity Act.

"You raise an important point that ECOA does not outlaw discretion," Ficklin said. "There are situations where discretion can be valuable. There are times where individual determinations might be valuable to the borrower. But we don't have a specific system to tell you what you should do."

In closing the hour-long panel session that was one of the highlights of AFSA's annual gathering ahead of the National Automobile Dealers Association Convention & Expo, Ficklin again reiterated four elements as to how a finance company can organize a compliance department to ensure dealerships are not being discriminatory.

Those four points first came from the bureau last March when it released its guidance on auto financing.

"Those four components are the bureau's position as well as the Department of Justice's position about what are the essential elements of appropriate compliance," Ficklin said.

The bureau official also made reference to a concern AFSA is looking to address in a year-long study that's being orchestrated beginning this month. Ficklin maintained that much of what drive bureau action is data.

"I will say that while we've certainly heard the assertion that consumers pay less in an indirect scenario, we have still not seen solid studies showing that. And we would welcome that. That's something of interest to the bureau more broadly," Ficklin said.

"But the specific area we're focused on right now is the fair lending risk created by the discretion and the markup policies," she went on to say.

A high-ranking official from the Consumer Financial Protection Bureau is among the speakers on tap to be a part of American Financial Services Association’s 18th annual Vehicle Finance Conference and Exposition set to begin on Jan. 22 at the Sheraton New Orleans.

AFSA highlighted Patrice Ficklin, assistant director of the CFPB’s office of fair lending, will discuss the bureau’s approach to regulation and compliance based on the bureau’s fair lending bulletin issued last March.

The three-day conference will kick off with a macro-level examination of industry trends by:

—John Gray, president of Experian Automotive

—Michael Buckingham, senior director of automotive finance at J.D. Power & Associates

—Sarah Watt House, economist at Wells Fargo Securities

Experts from top-notch research, strategy and vehicle finance firms will delve into technology innovations, how to connect with younger generations, relationship management, and risk management, in line with the conference theme “Navigating the New Normal.”

Bob Lutz, retired vice chairman of General Motors, will share key lessons that he learned over his 47-year career and identify best practices during the keynote address.

A candid panel discussion among vehicle finance chief executive officers will feature:

—Dan Berce, president and CEO of General Motors Financial

—Thasunda Brown Duckett, CEO of auto and student loans at Chase Auto Finance

—Mike Groff, president and CEO of Toyota Financial Services.

In addition, four leaders from the National Automobile Dealers Association will share the dealer perspective in the “Top Issues for Dealers in 2014” session.

The conference will close with a look forward as Sheryl Connelly, global consumer trends and futuring manager at Ford, shares probable shifts in consumer values, attitudes, and behaviors.

View the complete schedule and register for AFSA’s 2014 Vehicle Finance Conference and Exposition at www.vehiclefinanceconference.com.