Coming on the heels of Automotive Intelligence Council member MBSi Corp. making a move involving the firm, Recovery Industry Services Co. (RISC) announced it has joined forces with recently acquired Vendor Transparency Solutions (VTS) to unite compliance services and provide comprehensive vendor vetting, lot inspection and education services to the collateral recovery industry.

For years as independent companies, RISC and VTS stressed that they have advocated for a more professional repossession industry. By integrating the compliance solutions, RISC insisted that it now offers the best of both companies to the industry.

“We are proud to partner with RISC to provide a repossession training and vetting solution that has been embraced by both vendors and lenders, and we thank those who have supported our efforts,” said Max Pineiro, president of Vendor Transparency Solutions.

“With the recent acquisition of the VTS software platform, we looked to partner with the industry standard CARS program to add value to the VTS training curriculum and vetting services. Additionally, the involvement of Hudson Cook solidifies it as the industry standard,” Pineiro continue.

In the weeks and months ahead, RISC will announce new product offerings that combine the best of RISC and VTS curriculum and technology solutions.

“With this partnership, we continue to work towards improvement and unification of the industry,” RISC chief executive officer Stamatis Ferarolis said.

“It will take some time to integrate our curriculum and vetting services, but we believe together we now deliver the only comprehensive compliance and education solution to the collateral recovery industry,” Ferarolis went on to say.

Experian’s Q4 2018 State of the Automotive Finance Market report showed that seven states closed this past year with 60-day delinquency rates of at least 1 percent.

Overall, analysts pinpointed the 60-day delinquency rate at 0.78 percent in Q4, which represented an uptick of 3 basis points year-over-year.

What Experian defines as finance companies — institutions that do not hold commercial deposits but fund vehicle installment contracts — had the highest rate for 60-day delinquency among the four categories of providers. Finance companies — which also often cater to subprime customers — saw its rate improve 10 basis points year-over-year to settle at 1.87 percent.

Experian also mentioned the 60-day delinquency rate for banks came in at 0.70 percent (up 14 basis points). For captives, it was 0.73 percent (down 2 basis points) and for credit unions, it was 0.26 percent (down 1 basis point).

Along with those seven states at or above 1 percent, Experian also highlighted the Top 10 states for 60-day delinquency as of the fourth quarter. That rundown included:

1. Maryland: 1.68 percent

2. Mississippi: 1.68 percent

3. Louisiana: 1.36 percent

4. Georgia: 1.03 percent

5. New Mexico: 1.03 percent

6. Alabama: 1.00 percent

7. South Carolina: 1.00 percent

8. Nevada: 0.92 percent

9. Texas: 0.90 percent

10. Arkansas: 0.89 percent

More consolidation in the recovery space arrived late on Tuesday as Automotive Intelligence Council member MBSi Corp. increased its collection of resources.

The provider of compliance-enabled repossession assignment management software and vendor management software announced the acquisition of My Recovery System and Vendor Transparency Solutions’ platforms. The company highlighted this acquisition allows MBSi to offer a single software ecosystem for repossession assignment management and vendor compliance management to recovery agents, forwarders and auto-finance companies.

The integration of My Recovery System’s back-office platform and Vendor Transparency Solutions’ web-based compliance management system with MBSi’s assignment volume, operating excellence and talent formalized what the company described as a “game-changing component” of MBSi’s overall solutions strategy.

“We are thrilled to be working with the My Recovery System and Vendor Transparency Solutions platforms and teams to provide a seamless software solution for the recovery industry,” MBSi president Cort DeHart said in a news release.

“By capitalizing on these easy-to-use platforms, we will be able to bring new efficiencies to the industry with a seamless software solution that includes routing, full back-office and compliance management. This, coupled with the talent of the teams, sets us apart to deliver real results,” DeHart continued.

Two leaders from My Recovery System and Vendor Transparency Solutions also described what the transaction means.

“I’m excited to be part of a growing company where designs and strategies bring efficiency and transparency to the auto finance recovery industry,” said Jeff Koistinen, founder and president of My Recovery System. “MBSi’s commitment to the recovery agents ties back to our collective mission to exceed the needs of agents.”

Vendor Transparency Solutions founder and president Max Pineiro added, “I couldn’t be happier to join the MBSi team as we work together to deliver next generation compliance management platforms for recovery agents, forwarders and lenders.”

MBSi indicated its teams will immediately begin working to integrate the platforms to provide data and secure access of sensitive consumer information. MBSi also said it will continue to partner with RISC, which provides vendor vetting, compliance training and lot inspection services.

MBSi is hosting a recovery agent user conference and appreciation event on April 17 at Texas Live!, an entertainment venue in Arlington, Texas, starting at 3 p.m. CT. The user conference is exclusive to recovery agents to learn more about the new platform, pricing and how to get started.

Recovery agents can register for the event here.

Dumb question: Who wants to make more money? We all do, of course. But is opening your business to more credit-challenged consumers worth chasing more delinquencies and repos? Good question; and one that becomes problematic if you don’t take the right steps to minimize your risk. But, can I reduce risk and make more money without spending more? Great question.

Traditionally, the industry’s approach to managing risk involves manual processes that are tedious and time-consuming. Maintaining and following up on exhaustive consumer records of everything — phone numbers, addresses, employment — requires time and manpower you simply don’t have. As a result, taking on the operational cost of expanding your subprime business could be a nonstarter. One look at the consumer contact and employment statistics for this market segment underscores the burden.

The information chase

According to the FactorTrust Underbanked Index: Consumer Stability report, a borrower who has changed his or her mobile phone number four or more times over a 90-day period has a 77 percent higher default risk than a borrower who has done so only twice. Additionally, a borrower who has had three or more ZIP codes over a 90-day period has a 63 percent higher default risk than a borrower with one ZIP code. Further, among the underbanked, 16 percent applied with a different employer within 30 days, 20 percent within 60 days, 23 percent within 120 days and 34 percent within one year.

Remember the Wayne Gretzky quote, “I skate to where the puck is going to be, not where it has been?” Keeping up with subprime consumers is like trying to predict where that puck will be, which is nearly impossible without the tools to help.

If cars could talk

There is an option for managing risk in the subprime market that supplements a dealer’s ability to vet these consumers: gathering vehicle intelligence. With advances in aftermarket telematics and driver analytics, the latest technology can provide customer insights far beyond the standard vehicle location data associated with early GPS systems.

When it launched onto the buy-here, pay-here scene more than 15 years ago, GPS made it much easier to find a vehicle for repo. Over the years, the technology has evolved to look at location data over time, with the ability to predict where a vehicle will likely be at any time of the day or night with incredible accuracy. For example, the technology can now identify a change of job or home address through deviations in driving patterns. Let’s face it, unless they’re the James Bond type, most people have a set daily routine bouncing back and forth between home and work. Modern GPS solutions can detect major life changes by analyzing location data in relation to time of day, day of week, and pattern frequency.

Similarly, these same algorithms can automate and expedite loan stipulations that typically require hours of calling to verify addresses and workplace information. It’s also useful in preparing agents for repossession, when needed, to better target the right place and time for recovery. Accurately predicting vehicle location under specific circumstances (such as during Monday night football) leads to easier, less costly and less risky recoveries.

Smart solutions combine vehicle intelligence with proactive alerts to further reduce operational costs. Cars that aren’t driving, aren’t paying, so automated alerts for “non-driving” scenarios, such as vehicles impounded to tow lots, abandoned vehicles, and battery disconnects save dealers thousands of dollars each year. The ability to set geo-fences — virtual boundaries around key locations like tow lots, state borders and ports of entry — can help you keep your finger on the pulse of your assets without any effort on your part.

As with any technology purchase, reliability should be one of the main evaluation criteria. Leading GPS providers have always-on platforms (ask about uptime and availability rates) and wide-reaching network support that keeps vehicles connected no matter where they roam. You should ask any provider you’re vetting about the quality and quantity of the data its devices track. It’s no longer enough to monitor vehicle location every 24 hours, as was the industry standard. You need near real-time visibility that can only come from telematics devices that report data at 5-minute intervals or less, giving you the confidence to act when action is warranted.

Finally, the unique value of modern telematics is its ability to drive increased payments. Gone are the days when “starter interrupt” was the only way to get the attention of a delinquent customer. With 85 percent of the U.S. population carrying smartphones, the key to customer engagement is mobile. If the GPS technology you’re considering (or currently using) doesn’t offer a mobile component that opens up a soft-touch but high visibility communication channel between you and your customer, keep shopping.

Ask and ye shall receive

To thrive and survive in this hyper-competitive business, dealers must look beyond their current constraints in servicing this segment. Advanced vehicle intelligence offers not only a safer path to do business with the subprime consumer, but also the operational efficiency necessary to improve the bottom line. If you’re thinking about GPS as a recovery tool, think again, and remember what your teacher said back in grade school: “there are no dumb questions” — except the ones you don’t ask your suppliers.

Brian Deeley is a director of product management at Spireon. He can be reached at [email protected].

Anyone who has been involved with the repossession industry over the past several years knows that the world looks very different today than before the Consumer Financial Protection Bureau arrived. Most of the focus during this period has been on third- and fourth-party oversight. Given the CFPB’s official position on vendor management, it is no longer acceptable to rely solely on the agent or repossession management company to keep their shops in order.

Today, extensive vetting, on-site visits to every storage lot, proper contracting, performance/compliance score cards and broader insurance coverage are the norm. As a result, lenders and regulators can be comfortable that the agents recovering cars on their behalf have been well vetted and are closely monitored. Indeed, the CFPB has expressed general satisfaction on this aspect of vendor management

At this point, there are two primary areas the CFPB is focused on when it comes to repossession:

1. Fees that consumers are charged for retrieving personal property, and to a lesser extent redeeming their vehicle

2. Repossessions made in error

Adequately addressing these issues will pretty much squeeze out the remaining regulatory concern and legal exposure.

The “fees” issue has largely been addressed, especially by major lenders. Most have either mandated that any consumer charges be billed back to the lender (and posted to the customer’s account) or the allowable charges have been capped at defined and reasonable levels. There is still the issue of ensuring that agents follow the requirements, but we will save that for another post.

This leaves the issue of repossessions in error as the final major area to be addressed. Indeed, the CFPB has referenced the matter in its last two bulletins.

The vast majority of repossession in errors occur due to communication breakdowns. We see two types:

1. Internal communication breakdown within the lender’s operation where the auto repossession management company or agent was not notified when a repossession order was put on hold or closed. As a repossession management vendor for lenders, there is not much we can do to impact their internal processes/operations.

2. Vendor(s) communication breakdowns when a hold/close has been issued properly by the lender but the proper communication and systems updating by all involved parties did not take place.

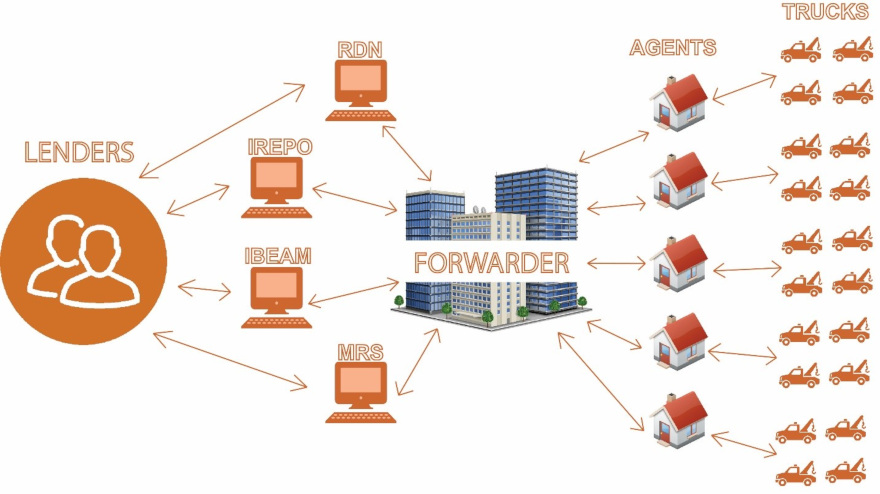

The latter is largely a technology issue. The lenders, management companies (forwarders) and agents generally operate on different platforms and degrees of sophistication. And for each of these players, there are multiple platform options. Breakdowns can occur at each point along the way and these breakdowns account for a large percentage of repossession in errors. The diagram at the top of this page illustrates the challenge and the components/integrations that must be in place to solve the problem.

To address the challenge, there must be close to real time communication from lender to forwarder to agency system of record to repo truck driver. Fortunately, recent improvements in systems integrations and the emergence of mobile platforms supporting repossession agency operations, provide solutions to the challenge, for the first time.

Today, there are two primary mobile platforms that, if integrated properly, can support the data exchange requirements. These are RDN/Clearplan and the Recovery Compliance Mobile (RCM) platform provided by MBSi. While each takes a somewhat different approach, both are solid systems that are designed to provide compliance functionality at the truck level. The recent acquisition of Clearplan by RDN and KAR Auction Services does offer some additional functionality and efficiencies made possible by the fact that the vast majority of repossession agencies use these two platforms as their systems of record.

If your institution relies on repossession management companies (forwarders) to coordinate the repossession activity, deep integrations with these platforms must be in place. Due to internal constraints, very few have the capability to facilitate the data between the various parties regardless of the source. At ALS Resolvion, we have invested heavily in these integrations and by mid-February, we will be only utilizing repossession agencies that deploy this type of mobile technology in the field.

Our expectation is that more and more lenders will be mandating real time “two-way” communication all the way down to the truck level. Doing so will bring us all very close to meeting both regulator and lender senior management expectations for squeezing out repossession made in error.

Mike Levison is the chief executive officer of ALS Resolvion. More details about the company can be found at www.alsresolvion.com.

Just ahead of the American Financial Services Association’s Vehicle Finance Conference, Allied Solutions announced the restructuring of its claims and recovery product, REPOPlus & Track.

The provider of insurance, lending and marketing products to financial institutions in the U.S. for more than 35 years, explained what’s new with REPOPlus & Track on Monday. In addition to claims and recovery services provided with REPOPlus, four distinct insurance monitoring options are available in an effort to offer flexibility to lenders seeking a cost-effective, efficient insurance tracking solution. They include:

— Auto Match

— Basic Track

— Active Track

— Advanced Track

After years of offering REPOPlus as a recovery service to finance companies, Allied Solutions indicated that it utilized this experience to develop value-added tracking options to maximize cost benefit.

The company highlighted each track offers a variety of support for electronic insurance notifications, loan files, paper insurance documents and borrower communications. These options can provide insurance monitoring and tracking support for a myriad of finance companies, including small to large volume and prime to subprime markets.

Allied Solutions insisted the combination of REPOPlus & Track with insurance monitoring options can provide finance companies a comprehensive loss and recovery and optimization program. Track solution options range from basic to full coverage of service monitoring.

“Allied Solutions recognizes that our clients have a diverse set of needs when it comes to their monitoring and optimization programs,”, CEO, Allied Solutions chief executive officer Pete Hilger said.

“We have created a comprehensive solution that ensures lenders receive the information they need to best measure and assess risk, protect their collateral and ensure optimization of insurance recovery claims,” Hilger went on to say.

Allied Solutions will share additional information about REPOPlus & Track during AFSA’s conference, which begins on Tuesday in San Francisco.

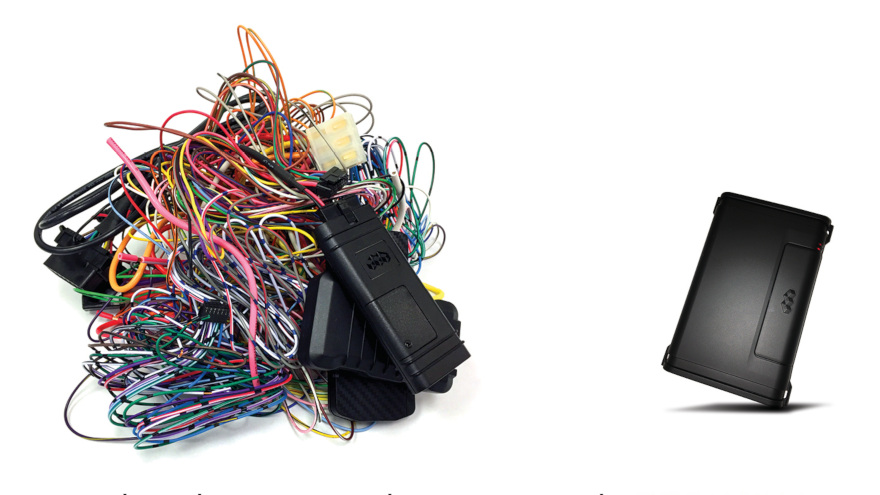

Some smartphones no longer need a cord to recharge, and now Advantage GPS has a unit that doesn’t need wires to function in a vehicle connected with a retail installment sales contract held by an auto finance company.

On Wednesday, the Procon Analytics company that captures and translates raw data into actionable business intelligence, launched its suite of wire-free GPS tracking devices aimed at solving one of the most common problems with using these units to mitigate risk. The company believes Revo is a game-changing, wire-free family of GPS vehicle tracking devices that is designed to revolutionize the way buy-here, pay-here dealers and subprime auto finance companies protect their collateral and gain valuable automotive analytics.

“Over the past 10 years battery technology has steadily improved and has now reached a level of long-term, stable dependability,” said Bill Cheney, chief technology officer and managing partner for Procon Analytics. “This in conjunction with the advancements in 4G LTE cellular and GPS receiver technologies have made our Revo family of products practical and affordable.

“We believe these Internet of Things innovations will revolutionize the GPS tracking industry,” Cheney continued.

The company highlighted Revo’s sophisticated, battery-powered technology can be secured almost anywhere in a vehicle in five minutes or less. Because of Revo’s revolutionary technology, battery life and ease of installation, Advantage GPS contends the device can reduce the No. 1 reason for device failure — improper installation — to near zero.

“It was important to design battery-operated devices would hold up for the duration of long-term finance contracts to protect our customers’ vehicle assets,” said David Meyer, president of Advantage GPS.

“Working side-by-side with leading experts in battery technology, we did it. We developed three new wire-free devices that provide more flexibility, control and, in the end, reduce costs and the hassles of installation for our customers,” Meyer continued.

The company explained all three Revo devices — SmartStop, 3000 and 4000 — take only about 10 seconds to activate and are immediately connected to the platform via 4G LTE wireless technology. The three different Revo models can give dealers and finance companies the flexibility to match device to loan terms or risk factors.

Other capabilities of the units include:

• Revo SmartStop: Collects a continuous stream of data for all start and stop events of a vehicle up to 3,000 events or approximately one year.

• Revo 3000: Provides auto finance companies with flexible operating modes that gives them more control and help preserve the battery life of the unit. The unit is designed to capture 3,000 events just like the SmartStop, but this device has a life span of approximately three years.

• Revo 4000: Includes the three flexible modes and captures at least 4,000 events for at least four to five years.

The company went on to mention the discovery, standby, and recovery operating modes are an integral part of the Revo 3000 and 4000. Here is a further explanation:

• Discovery mode: Provides a detailed history of the vehicle for the first 250 events. This sets up the vehicle’s routine. Much is learned during this period, but once completed downshifts to the less power-consumptive standby mode.

• Standby mode: Reports a vehicle’s location and device health (such as battery life and tamper alerts) twice each day. Finance companies, when they see a need, can change to the third recovery mode. Despite the low-power consumption of standby mode, the company said valuable data is collected every day.

• Recovery mode: With a simple keyboard click, Revo reports a vehicle’s movement every five minutes and also sends stop events. To preserve battery life, Revo will automatically revert to standby mode (after seven days or 500 events) or SmartStop mode based on the customer’s product choice.

Importantly, the company added that Revo devices also have many of the same features that hard-wired devices do, including:

— Drive reports

— Stop reports

— Repo mobile tool

— Geofencing

— Tamper alerts

— Battery life indicator

— 4G LTE service

Meyer pointed out that what it has doesn’t come with is the average $55 installation fee, extra cables and accessories and a device service plan. He said the company has already started shipping Revo devices to auto lenders across the country.

“We also guarantee the number of events for each Revo device,” Meyer said. “That guarantee, along with the savings from not having to pay for hard-wire installations will save dealers thousands of dollars during the course of a year, with nearly no installation failures.”

With the federal government shutdown clash involving President Trump and Congressional leaders already lasting longer than any impasse in history, policymakers, banking leaders and finance companies are all collaborating to help impacted federal workers who are not being paid their wages.

Following a statement by five federal and state financial regulators, Consumer Bankers Association president and chief executive Richard Hunt shared strategy similar to what’s been offered by an array of finance companies who have contract holders with interrupted incomes. It is estimated that more than 800,000 workers are not getting paid during the shutdown.

First, here is what policymakers said in a joint statement that included Consumer Financial Protection Bureau, the Federal Deposit Insurance Corp., the Office of the Comptroller of the Currency, the Federal Reserve Board and the Conference of State Bank Supervisors.

“While the effects of the federal government shutdown on individuals should be temporary, affected borrowers may face a temporary hardship in making payments on debts such as mortgages, student loans, car loans, business loans or credit cards,” the policymakers said. “As they have in prior shutdowns, the agencies encourage financial institutions to consider prudent efforts to modify terms on existing loans or extend new credit to help affected borrowers.

“Prudent workout arrangements that are consistent with safe-and-sound lending practices are generally in the long-term best interest of the financial institution, the borrower and the economy. Such efforts should not be subject to examiner criticism,” they continued.

“Consumers affected by the government shutdown are encouraged to contact their lenders immediately should they encounter financial strain,” they went on to say.

Hunt replied to regulators outlining the assistance programs banks are proactively offering customers impacted by the shutdown. Hunt’s letter that’s available here also thanked regulators for offering guidance similar to that issued during previous shutdowns.

“Consumer Bankers Association member institutions work with customers facing hardships — whether manmade or natural — every day. Banks are working with customers on a one-on-one basis as the partial government shutdown continues and federal employees, through no fault of their own, begin missing paychecks and small businesses are not able to access Small Business Administration loans,” Hunt wrote.

“We know federal employees had no role in this shutdown, neither did banks. As with so many other issues ranging from wildfires, floods and hurricanes to data breaches at retail giants, banks are the ones on the front lines helping make it right for their customers,” he went on to state.

Hunt also appreciated the regulatory guidance, noting it “will enable banks to do more for their customers impacted by this partial shutdown.”

Since the partial shutdown began on Dec. 22, banks have offered furloughed federal workers a variety of assistance, including:

— Deferments

— Temporary hardship programs

— Automatically waiving or refunding overdraft and monthly service fees

— Increasing overdraft limits

— Offering access to certificates of deposit without penalty

— Providing loan payment assistance

— Suspending collection calls

— Streamlining unsecured loans

Along with banks, finance companies are also helping impacted federal workers who have vehicle installment contracts.

For example, Hyundai has relaunched its Assurance program like the automaker did in 2013. Under the plan, the OEM will extend all Hyundai Capital auto loan and lease payments for 30 days for current Hyundai owners who are federal government employees furloughed during the shutdown.

“We recognize that there are many federal employees who are Hyundai owners and are not receiving their normal pay check," said Brian Smith, chief operating officer of Hyundai Motor America. “Hyundai is a brand that aims to make things better for its customers, and this is our way of showing customers ‘We have your back’ during this uncertain time.”

Meanwhile, other captives such as GM Financial and Ford Motor Credit each have alerts at the top of their websites, directing furloughed federal workers who have been impacted to contact them as soon as possible to make payment arrangements.

When the shutdown will end probabaly can’t be predicted based on what been shared via Twitter.

Speaker of the House Nancy Pelosi posted late on Monday, “It’s day 24 of the #TrumpShutdown. 800,000 Americans are losing paychecks. The health & safety of countless more are in jeopardy.”

And Trump retorted on the social media platform on Tuesday morning, “Why is Nancy Pelosi getting paid when people who are working are not?”

On Friday, KAR Auction Services announced an addition to the management team for one of its business units, Recovery Database Network (RDN).

Joining the provider of specialized software and data solutions to customers across the repossession and disposition value chain as vice president of business development is John Sibbitt.

The company highlighted Sibbitt brings eight years of management, operations and asset recovery experience to RDN.

“John has a proven track record of success in the repo industry with strong leadership and customer relationship building skills,” KAR president Peter Kelly said.

“As part of what is now an integrated management team for RDN and Clearplan, John will help us expand our customer base and footprint as we deliver the most powerful software platform in the industry,” Kelly continued.

In his new role, Sibbitt will be responsible for managing current RDN client relationships, identifying opportunities for growth and expanding the client network.

Sibbitt previously served as vice president of operations at PAR North America, a leading U.S. provider of vehicle transition services with coast-to-coast solutions for recovery management, skip-tracing, remarketing and title services — also a KAR business unit.

Sibbitt was part of the team that launched PAR Platinum Compliance; the culmination of a year-long project to roll out a compliance, due diligence and transparency tool. He managed all of PAR’s vendor network, overseeing compliance and managing the relationships of more than 700 recovery vendors.

Before joining PAR in 2012, Sibbitt oversaw a large specialty portfolio for Liberty Recovery Services.

BillingTree named a new chief executive officer on Thursday.

Coming aboard as the new leader of the supplier of financial technology and payment solutions is Christine Lee. The company indicated in a news release that former CEO Edgars Sturans will remain as a BillingTree board member.

BillingTree highlighted Lee’s hiring comes at an opportune time for the rapidly growing payment solution provider, supplying a wealth of payment industry and banking experience as the company expands deeper within new verticals. Her expertise will complement the company’s success in ARM, auto finance, banking, credit unions and healthcare.

The company described Lee as a highly accomplished industry veteran having successfully lead teams at Moneris, Vantiv, NPC and Bank of America and is currently the president elect for the Electronic Transactions Association (ETA). She’s also served as the Women’s Network in Electronic Transactions (WNET) president and 11-year board member participant.

BillingTree, headquartered in Phoenix with offices in Toledo, Ohio, processes more than $4 billion in payments annually for clients from multiple industries. The company was most recently recognized as one of the Top Revenue Cycle Management Solutions for 2018.

“I am pleased Christine accepted the CEO position here at BillingTree. Her outstanding resume and experience are the perfect fit to build on our 15-year sustained track record of success, innovation and client service excellence,” Sturans said.

Lee added, “I’m thrilled to join BillingTree, a proven payments company with innovative technology solutions including Payrazr and CareView, which position us for rapid growth within our current and future target verticals.

“The payments industry is rapidly changing, and my career history will serve us well as we continue to scale BillingTree’s revenue growth and software solutions to clients,” Lee went on to say.

Lee plans to be part of BillingTree webinar set for Jan. 30 at 1 p.m. ET, where the company plans to discuss a variety of topics, including a compliance update as well as developments regarding the alert notification process.

To sign up for the free webinar, go to this website.