Compliance experts and industry advocates have been trying to project what might happen to the Consumer Financial Protection Bureau since President Trump was elected back in November.

Two developments arrived this week that perhaps might give auto finance companies and other service providers a bit more clarity.

First, U.S. Senator Deb Fischer, a Nebraska Republican, and two of her GOP colleagues from the upper chamber reintroduced legislation that would make changes to the structure of the CFPB, replacing the single director with a bipartisan board of directors comprised of five individuals.

Then multiple online reports appeared early Friday indicating Trump was set to sign another executive order; this time calling for a significant review of the Dodd-Frank Act with the aim of considerably scaling back the regulatory structure the legislation enacted.

The CFPB declined to comment about the reported Trump order when reached by SubPrime Auto Finance News on Friday morning. However, CFPB director Richard Cordray made a clear point about the bureau’s objective through his prepared remarks when the agency released its study on debt collection early last month.

“The Consumer Bureau has the authority and the duty to enforce the law to protect consumers, and we will not tolerate those who harm them by violating the law. Our work to ensure that all consumers are treated with dignity and fairness will continue,” Cordray said.

No matter that pledge, Fischer highlighted the changes her proposal — the Consumer Financial Protection Board Act — would bring, including:

— Each board member would be appointed by the president and confirmed by the Senate.

— The president would appoint one of the five members of the board to serve as chairperson of the board.

— Board members would each serve staggered five-year terms, and no more than three members would be from the same political party.

— The legislation would take effect on the date on which not less than three persons have been confirmed by the Senate to serve as members of the board of directors.

Co-sponsors of the bill included Sen. John Barrasso of Wyoming and Sen. Ron Johnson of Wisconsin.

“For years, the bad decisions made by a single director at the CFPB have kept families locked out of economic opportunity,” Fischer said. “My bill would prevent this misconduct by divesting the authority from one director to a five-member bipartisan board.

“This much-needed structural adjustment would bring accountability to the bureau and give more Americans a chance to build their own businesses and provide for their families,” she continued.

This proposed measure is the sort of action experts predicted might happen; authorities who participated in a nearly hour-long panel discussion during last week’s Vehicle Finance Conference hosted by the American Financial Services Association. One of those experts was Frank Salinger, who now operates his own firm, Public Policy Law Practice, but also served with AFSA during the 1980s.

“When you think about it, for 236 years of our republic, people managed to make loans without the CFPB. Somehow it all functioned. Then this agency is created. What is the Republican answer? Let’s make it better. Let’s make it a commission, not abolishing it,” Salinger said.

At the start of the panel session, AFSA vice president Bill Himpler asked the audience about whether Cordray would remain through the end of his term that’s set expire next summer. Using electronic polling equipment, more than 80 percent of participants said Cordray would not finish his term.

Those results triggered a wide array of observations from another expert on the panel, Mark Calabria is director of financial regulation studies at the Cato Institute. Before joining Cato in 2009, he spent six years as a member of the senior professional staff of the U.S. Senate Committee on Banking, Housing and Urban Affairs.

“I think there will be a push by this administration to replace Cordray,” Calabria said. “I would emphasize that this crowd might not have the anger toward Cordray that some others do. But almost to a person, everyone who works on financial policy in Washington really dislikes the guy.

“You could have someone put in that agency who could have made it a bipartisan, generally liked agency,” Calabria continued. “Cordray decided not to do that. He decided to be extremely partisan, and I think that’s kept the issue alive in a way that would not have been the case now.”

Calabria’s assessment of the feelings about Cordray went even further, suspecting that about a third of CFPB’s staff “would be happy to see Cordray go.”

If the CFPB remains under the controls of a single director, Calabria also has a hunch who the replacement would be — Randy Neugebauer, a former Texas Republican who was chairman of the U.S. Financial Institutions and Consumer Credit Subcommittee and chose not to run for reelection last year.

“There’s just too much for the president to do right now if he didn’t think this was a priority. The tea leaves say to me that Neugebauer will be the nominee, and we’ll hear his name within the next month,” Calabria said.

And what would happen to Cordray? Salinger addressed that question.

“We must remember that Cordray is a politician,” Salinger said recapping the director’s time as an elected state lawmaker and treasurer as well as time as attorney general in Ohio along with his failed attempts to secure spots in both the U.S. House and Senate.

“When he took the job, the conventional wisdom in Washington was he would be here and go back and run for governor,” Salinger continued. “But by the time the election came around, (current governor) John Kasich’s numbers were off the charts and he won in a landslide. So if Cordray wants to go back, he doesn’t have many options. If he wants to run for governor, that won’t be until 2018.”

So whether Cordray eventually is replaced with another single director or a five-member board, Calabria added one more assessment of what his CFPB legacy might be.

“A Republican could come in and be very aggressive,” Calabria said. “Because Cordray has decided he does not want to do this through the appropriate way through regulation, but just do it off the top of his head very discretionary, has left himself open to much of what he’s done simply being undone the next day.”

Repossession and skip-tracing services provider Loss Prevention Services (LPS) announced on Thursday that the company has chosen MBSi Corp. as its assignment and compliance management solution.

Throughout the year, LPS said it will transition its assignment management platform to Recovery Connect (RC), MBSi’s next generation assignment platform.

In addition to adopting Recovery Connect, LPS also has chosen to adopt MBSi’s Compliance Made Easy (CME) suite of compliance platforms, as well as MBSi’s full vendor compliance management services.

The company explained this decision allows LPS to integrate assignment and compliance management into one system so clients can gain added transparency and analytics for improved results.

LPS said it strives to maintain the highest compliance standards in the industry, both internally and with its national vendor base. With this announcement, the company added that goal has been taken to a new level.

LPS highlighted the combination of RCM and CME not only provides line-of-sight into the compliance status of each agent, but also ties compliance standards down to the assignment level to ensure that vetted, trained, and qualified agents service each assignment.

In addition to improving compliance for its vendors, LPS will now be able to provide its clients with real-time transparency and data analytics. With RCM Recovery data, condition reports and client updates will be instantly available to LPS clients, providing the critical information and analytics necessary to make timely decisions regarding collateral.

“We have partnered with the MBSi team and their RCM & CME products to move Loss Prevention Services and the industry forward,” said David Cowlbeck, president and chief executive officer of LPS who noted that he has spent more than 20 years in the industry using every system, including proprietary internal systems.

“MBSi’s progressive solutions facilitate our vision of utilizing the latest technology to make the collateral recovery process more productive for our clients and vendors,” Cowlbeck said. “We look forward to continuing our quest to be a consultative resource to lenders and the agencies we work with to provide excellence in service, compliance and growth.”

Cort DeHart, manager of corporate strategy for MBSi, elaborated more about the background between the two companies.

“I have had the good fortune to work with David for many years, and am very excited to be able to offer these products to LPS,” DeHart said.

“David and his team at LPS understand and appreciate the vital role that technology can play in running a recovery business,” DeHart went on to say. “We look forward to providing LPS with the right set of tools to do the job they do best.”

In addition to adopting the MBSi solutions, LPS also has chosen to increase training and education for all of its internal employees and vendor network. LPS picked Recovery Industry Services Co. (RISC).

RISC offers CARS (Certified Asset Recovery Specialist) training program that can allow LPS to provide its agents with continual education on the ever-changing compliance requirements of the vehicle repossession industry.

Because MBSi is fully integrated with RISC, LPS said it will be able to verify CARS certification in real time on every assignment.

Formed through thousands of conversations with the nation’s leading dealership principals and finance companies, EFG Companies finalized four predictions and recommendations for 2017.

President and chief executive officer John Pappanastos summarized the results on Tuesday, saying these insights reflect an air of cautiousness for the F&I market.

But Pappanastos added there are many options for the industry to successfully navigate an uncertain business climate for a prosperous year.

“Even though the election is over, we continue to see a murky forecast for the F&I market moving forward,” Pappanastos said. “Consumers clearly want a new — and at least partially online-buying process. This trend has significant impact for the F&I industry across retail and lending channels.

“We also expect to see credit tightening on the consumer side and a foreshadowing of reduced auto manufacturer incentives for dealers, which will impact their margins,” he continued.

“Finally, we don’t believe federal regulatory oversight will diminish to the level that is being hyped. So, we strongly believe compliance will continue to challenge dealers and lenders,” Pappanastos went on to say.

“All that being said, we believe that the changes transforming the auto industry will create unique opportunities for dealers and lenders to leverage as they look to expand their business,” he added.

Four other executives from EFG Companies elaborated about the thoughts Pappanastos mentioned.

1. Flat volumes, compliance, and customer retention for retail automotive

While Consumer Financial Protection Bureau (CFPB) authority may be up in the air, John Stephens, executive vice president of dealer services, noted that dealers will need to stay the course on compliance for 2017.

“Remember, the Federal Trade Commission (FTC) has jurisdiction over dealers and its operations are not impacted by any potential changes within the CFPB,” Stephens said.

“Analysts are predicting flat unit sales volumes, pushing dealers to maximize their investment by squeezing more profitability out of their F&I operations,” he continued. “Customer retention efforts will increase, prompting dealers to shore up their service drive and fixed operations to deliver the ‘luxury car’ level of service.

In addition, an influx of off-lease vehicles will increase used-car inventory while putting pressure on pricing. Whether purchasing new or used, the customer will be king in 2017,” Stephens went on to say.

2. Return on investment and shorter transaction times key for F&I agents

With dealerships feeling increased pressure, Adam Ouart, vice president of agency services, projected that F&I agents will also experience a trickle-down effect to clearly demonstrate a return on investment for the F&I products they place at a dealership.

“Agents will also feel pressure to help dealers shorten transaction time and pivot their operations to support online transactions,” Ouart said. “Agents will closely monitor their own businesses to keep production levels high and begin focusing more on acquiring new dealership business. “

3. Rising interest rates and portfolio evaluations will challenge finance companies

Regardless of what happens with the CFPB, Brien Joyce, vice president of specialty services, said finance companies will also need to stay the course.

“You don’t stop treating customers right on the off chance that the government might not see your good behavior,” Joyce said. “Increasing interest rates will pressure lenders to tighten lending standards and evaluate other options to protect their loan portfolio outside of APR and loan terms. The same can be said for credit unions and other lenders that offer auto loans directly to consumers.

“I expect more lenders to evaluate how consumer protection products can benefit them from the standpoint of differentiating their institutions from the competition, protecting their loan portfolio, increasing loan volume, and controlling compliance,” he continued.

“In addition, dealers will re-evaluate their lender roster, confirming a broad spectrum of partners that specialize in different credit tiers, and help dealers meet their profitability goals,” Joyce added. “This will put pressure on lenders to evaluate their service model for dealerships and make adjustments to tackle mutual dealer and lender challenges.”

4. Growth and finance company challenges continue for powersports dealers

Although unit sales fell in the second half of 2016, Glenice Wilder, vice president of powersports, is anticipating volume will pick up in February when early income tax refunds arrive.

“There will be a slight growth in the powersports market overall in 2017 with dealers putting greater emphasis on increasing aftermarket income through the sale of F&I products,” Wilder said. “Lenders that remain in the powersports market will want to insulate their loans and may look to offering their own complimentary F&I products.

“As powersports dealers continue to be starved for lenders, up-to-date technology resources, and committed employees, they will pressure their vendors and product administrators to provide outside the box solutions for these obstacles, such as digital F&I services,” Wilder added.

Advocates for more regulation by federal agencies over the auto finance industry and other financial services providers might describe the latest executive order by President Trump as “one step forward and two steps back.”

The White House released the latest order involving regulations on Monday, saying that whenever an executive department or agency publicly proposes a new regulation, that department also must identify at least two existing regulations to be repealed.

“It is the policy of the executive branch to be prudent and financially responsible in the expenditure of funds, from both public and private sources,” the executive order said beneath the purpose heading. “In addition to the management of the direct expenditure of taxpayer dollars through the budgeting process, it is essential to manage the costs associated with the governmental imposition of private expenditures required to comply with federal regulations.

“Toward that end, it is important that for every one new regulation issued, at least two prior regulations be identified for elimination, and that the cost of planned regulations be prudently managed and controlled through a budgeting process,” the order continued.

The order, which is available here, also said that for fiscal year 2017 that’s currently ongoing that the heads of all agencies are directed that the total incremental cost of all new regulations, including repealed regulations, to be finalized this year should be no greater than zero, unless otherwise required by law or consistent with advice provided in writing by the director of the Office of Management and Budget.

Regulatory moves like this one by Trump were predicted at least to a degree during last week’s Vehicle Finance Conference hosted by the American Financial Services Association. During a nearly hour-long panel discussion, two experts faced the difficult challenge of trying to project what this administration might do in terms of how finance companies to navigate regulatory oversight and potential changes.

“Watch the media because we know this administration is all about the media,” said Frank Salinger, who now operates his own firm, Public Policy Law Practice, but also served with AFSA during the 1980s.

Moments later, Mark Calabria, who is director of financial regulation studies at the Cato Institute, added his thoughts. Before joining Cato in 2009, he spent six years as a member of the senior professional staff of the U.S. Senate Committee on Banking, Housing and Urban Affairs.

“We just don’t know yet with this administration whether it’s going to be populist, open market and pro-business. How it’s going to balance out is not clear,” Calabria said. “He’s a Republican, some might say not much of one, but he’s a Republican. What you see is not necessarily what you’re going to get out of the White House.

“Just as Trump has gone on Twitter and beat up on companies, I would see no reason to think any industry or agency would be exempt from that,” Calabria added.

The regulatory moves coming out of the White House on Monday arrived a little more than a week after Trump took his first action soon after being inaugurated. Reince Priebus, who is assistant to Trump and his chief of staff, released a memorandum that contained the subject line “Regulatory Freeze Pending Review” to outline six specific steps the heads of executive departments and agencies are to follow, including the halt of new regulatory actions for at least 60 days.

Two members of the legal team at Mayer Brown took a deeper look at what Priebus outlined and partner Laurence Platt associate Joy Tsai explained their findings through this blog post.

Platt and Tsai said the Consumer Financial Protection Bureau. the Federal Reserve Board, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corp. and the Securities and Exchange Commission are classified as “independent regulatory agencies” and may be excluded from that moratorium.

“Financial services companies that hoped for immediate regulatory relief when the Trump administration assumed control may have to wait a bit longer, because the newly announced freeze on federal regulations does not appear to apply across the board,” Platt and Tsai said.

“Although the memorandum appears sweeping in scope, banks and other financial service providers are not necessarily relieved from new regulations, as the regulatory freeze does not appear to apply to independent agencies,” they continued.

“However, the CFPB and other independent agencies remain subject to the Paperwork Reduction Act of 1980, which provides that an agency must not conduct information collection activities without the prior approval of the Office of Management and Budget director. This means that while the Office of Management and Budget may not be able to prevent an independent agency from issuing a new rule, it can stop the agency from requiring the public to submit filings to comply with the rule,” they went on to say.

“It is too soon to tell if any particular ‘independent regulatory agency’ believes that it is exempt from the freeze or, even if it is, it nevertheless will honor the memorandum’s spirit,” Platt and Tsai added.

Meanwhile back at the Vehicle Finance Conference, AFSA executive vice president Bill Himpler recapped a published report by The Wall Street Journal that quoted CFPB director Richard Cordray. Himpler noted the Cordray reportedly said when discussing the order associated with the 60-day moratorium that, “We believe the congressional mandate to protect consumers outweighs the executive order by president.”

Himpler asked the gathering in New Orleans, “How many of you think that got the attention of the president? I think it will be very interesting to see how that plays out.”

Editor’s note: More of the dialogue from the regulatory panel discussion during the Vehicle Finance Conference will be included in future reports from SubPrime Auto Finance News.

American Financial Services Association president and chief executive officer Chris Stinebert shared some of the details on Wednesday regarding how the organization has modified and bolstered its strategy now that President Trump is in the White House and Republicans control both segments of Capitol Hill.

During a 10-minute state-of-the-union-style address to a packed room at AFSA’s annual Vehicle Finance Conference, Stinebert outlined how the association modified staff that specializes in GOP leanings that now hold the majority in the U.S. Senate and House. Stinebert reflected back on both the Obama administration and recovery from the Great Recession, how AFSA immediately responded to Trump’s election victory in November and how the association now has what he called a “rare opportunity.”

“It’s going to be an exciting six months,” Stinebert said during his closing moments on stage at the Sheraton New Orleans where a record turnout of finance company executives and other industry players gathered ahead of the National Automobile Dealers Association Convention & Expo that opens later this week.

“I don’t want to say we’re thrilled in Washington, but we were anticipating a different ending,” Stinebert continued. “We were looking at basically playing defense for at least the next four years. We had been dealt that hand and were hoping we could draw new cards and make some changes.

“Now we have a whole new dynamic. We have major change. We have a new opportunity, and what I would say is truly a rare opportunity that’s unexpected,” he went on to say.

While closing with those thoughts, Stinebert opened by emphasizing how the finance community should “use the lessons that we’ve learned since the Great Recession to make our industry better, more responsive to consumers, while at the same time modifying regulatory and legislative requirements that make no practical sense that restrict our industries, that hurt the accessibility of credit and its affordability.”

In order to bolster those efforts, Stinebert explained AFSA needed to make changes. The association is about to hire a professional who will serve in the newly created position of vice president of Congressional affairs. AFSA already selected the individual who will be its manager of Congressional affairs, moving Susan Sullivan over from her previous post in state government affairs.

“With the makeup of Congress, we thought this was very important. Now we feel we soon will have the people and resources in place to move our agenda,” Stinebert said after shifting away from AFSA staff that specialized in how the Obama administration operated.

While AFSA is adjusting its personnel, Stinebert noted the organization also is keeping watch of the moves made by other associations and lobbying groups within the Beltway, describing how the past eight years often made representatives work closely together.

“As challenging as the last eight years have been, the financial services industry has been united. All of the sister trades — many of you belong to other associations — we were all in singular fight, somewhat united and together,” Stinebert said. “Put it this way, everybody played well in the sandbox for the last eight years.

“But now that’s changed. Everybody wants their priority, their issue to move to the top of the list, the front of the line and be No. 1,” he continued.

“We have priorities, too. We handed out those priorities and the board of directors has approved what we want to do,” Stinebert added.

While AFSA plans to maintain its drive toward planned objectives, Stinebert is hoping alliances strengthened during the past few years suddenly do not become compromised.

“We also recognize we can’t do this alone. We need help in Washington,” he said. We are working on forming a coalition with other groups. It’s sometimes strange bedfellows that you wouldn’t expect because we need allies and we need friends.

“To build momentum in Washington, seldom can you do it as one organization. We count on a lot of other groups that have similar priorities,” Stinebert went on to say.

So AFSA members know what’s happening, Stinebert pledged to maintain strong communications. A product that highlighted developments associated with the transition from Obama to Trump now will pivot its focus on what the new administration does during its first 100 days, which has included a hold on regulatory moves for at least 60 days.

Furthermore, AFSA plans to host conference calls for members since as Stinebert jokingly put it in light of scandalous stories, “as we all know, sometimes email is not the best way to communicate safely.”

Stinebert used an array of analogies to describe Trump’s style.

“We have a new president who I would say is more tilted toward improvisation and Twitter than set programs and policies,” Stinebert said.

“President Trump, he’s a change-up pitcher. He throws curveballs, and we don’t expect a lot of pitches down the middle of the plate,” Stinebert added.

While Trump and other lawmakers might be throwing the unexpected on the financial services industry, Stinebert is hopeful for what could percolate out of the White House and Congress to benefit auto finance companies and related participants.

“This opportunity, whether it’s two years, or four years or eight years, we know it is short-lived. And with hope with the ability to change and we’re looking at lasting change,” he said.

While the American Financial Services Association firmly is entrenched within the Capitol Beltway in Washington, D.C., the organization strives to represent the entire industry, not just a select group of players. AFSA president and chief executive officer Chris Stinebert reinforced that reasoning when describing the AFSA Vehicle Finance Board.

Stinebert said that board “features a broad cross section of companies: banks, captive finance companies and independent finance companies. Each member uses the indirect channel to finance new and used cars, trucks and motorcycles — meaning they purchase the loans from dealers and do not make auto loans directly to consumers.

“Indirect lending has proven to be the most cost effective and convenient way for consumers to finance a vehicle,” he continued. “Although each company competes fiercely for business, they all have common interests and concerns. This is the glue that binds.”

Those fierce competitors will be gathering together this week in New Orleans as AFSA hosts its annual Vehicle Finance Conference beginning. As usual, the gathering of auto finance company executives, legal experts and other service providers comes just ahead of the National Automobile Dealers Association Convention and Expo, also being conducted in the Big Easy.

“We have a wonderful working relationship with NADA,” said Stinebert, who again incorporated NADA leadership into the Vehicle Finance Conference program.

“Our relationship with NADA has been so productive because we look at the industry from the consumer’s point of view,” he continued. “We’re really talking about the same transaction.

“Both of our organizations represent members who have the same responsibility — to provide consumers with a smooth, transparent, and easy-to-understand vehicle purchase and financing process,” Stinebert added.

This year’s conference theme asks the provocative question, “Are we there yet?”

Stinebert said, “Our theme may remind you of a long road trip with your kids and sounds a bit odd. But it raises an extraordinarily important question. It provokes our members to ask themselves if their companies are 'there yet' on issues like compliance, cyber security, customer satisfaction and technology.

“We’re attempting to answer that question — sessions are focused on giving our members the tools and knowledge to make that journey,” he continued.

Josh Linker, an entrepreneur and hyper-growth CEO who has spent his career harnessing the power of disruptive change, will present the conference keynote. He will deliver a clear call to action for members — it is better to innovate and disrupt your organization before your competition does. The riskiest move companies can make today is embracing the status quo — believing the future will be like the past is the fast road to obsolescence.

Another important session will feature the three major credit bureaus coming together “to set the record straight” on the health of the subprime auto finance market. The experts scheduled to be a part of that discussion are:

— Denise Brown, chief risk officer Veritas Auto Finance and chair of the AFSA Vehicle Credit Risk Committee.

— Amy Crews Cutts, senior vice president and chief economist at Equifax Automotive Services

— Jason Laky, senior vice president and auto business lead atTransUnion

— Melinda Zabritski, senior director at Experian

David Paul (Vehicle Finance Division chair and senior vice president, financial services at American Honda Finance Corp.) and Mark Scarpelli (incoming NADA chairman and President of Raymond Chevrolet and Kia) will kick off the final day of the conference with a frank discussion about the important relationship between dealers and financing sources.

AFSA’s CEO Panel will feature key industry executives sharing best practices, compliance hurdles, and critical opportunities in the fast-moving marketplace of auto finance. That executive group is set to include:

— Jason Grubb, chief executive officer at Exeter Finance Corp.

— Dale Jones, executive vice president, Americas with Ford Motor Credit

— Mark O’Donovan, chief executive officer of Chase Auto Finance

— Vince Rice, executive vice president and consumer finance division head with Bank of the West

Organizers highlighted registration for the conference has grown steadily over the last decade. AFSA added that attendance at the 2017 conference has set a new record as more than 600 attendees will gather in The Big Easy to network, learn from the experts, and visit the conference’s more than 55 exhibitors.

Not only collaborating for this annual event, Stinebert touched on how else AFSA and NADA are working together so the financing of vehicle transactions goes well for all parties involved.

“One of AFSA’s core competencies is to educate politicians, regulators and most importantly, consumers, about the benefits of the auto financing process and the industry,” Stinebert said.

“This past year, in conjunction with the Federal Trade Commission and NADA, AFSA updated the Understanding Vehicle Financing brochure. This publication is a must read for anyone who wants to finance a car, including regulators and politicians,” he continued.

“Today, more than ever, consumers are going online to not only research certain vehicles in certain segments, but also to research the best way to finance and pay for their vehicles,” Stinebert went on to say. “In addition to constant dialogue with Capitol Hill staffs and regulators, this year AFSA and NADA are updating and modernizing the website for AWARE, an acronym for Americans Well-informed on Automobile Retailing Economics. This is a joint project shared by the two trade associations and their members. It is devoted to educating consumers about auto financing.”

As the industry descends into New Orleans, Stinebert shared his assessment of how the auto finance market behaved in 2016.

“We entered the year with concerns about The New York Times editorial on the pending subprime auto bubble and we ended 2016 with a huge sigh of relief,” he said. “Instead of disaster, we have enjoyed a very successful year of record sales.

“More importantly, the credit bureaus recently reported improved data on average credit scores and delinquencies, so no bubble and no crisis,” Stinebert continued. “This does not mean, however, we do not have many challenges going forward. But the looming regulatory and compliance issues facing the used-car market should see promised relief with the election of Donald Trump.”

Editor's note: Watch for updates from the Vehicle Finance Conference on our website as well as our Twitter feed at @SubPrimeNews.

Hudson Cook’s legal team spotted an announcement from Reince Priebus, who is assistant to President Trump and his chief of staff, that appears to have been released within moments after this past Friday’s inauguration.

Priebus used the memorandum that contained the subject line “Regulatory Freeze Pending Review” to outline six specific steps the heads of executive departments and agencies are to follow.

“The president has asked me to communicate to each of you his plan for managing the federal regulatory process at the outset of his administration,” Priebus wrote in the memorandum that Hudson Cook posted online here. “In order to ensure that the president’s appointees or designees have the opportunity to review any new or pending regulations, I ask on behalf of the president that you immediately take the following steps.

Among the steps Priebus mentioned are:

— Subject to any exceptions the director or acting director of the Office of Management and Budget allows for emergency situations or other urgent circumstances relating to health, safety, financial, or national security matters, or otherwise, send no regulation to the Office of the Federal Register until a department or agency head appointed or designated by the president after noon on Jan. 20, reviews and approves the regulation.

— With respect to regulations that have been published in the Office of the Federal Register but have not taken effect, as permitted by applicable law, temporarily postpone their effective date for 60 days from the date of this memorandum.

— Continue in all circumstances to comply with any applicable executive orders concerning regulatory management.

Donald Trump will be inaugurated as the 45th president of the United States on Friday. But industry experts have warned dealerships and finance companies not to reduce their compliance efforts despite some deregulatory rhetoric that might have been shared during his campaign.

Compliance expert Randy Henrick recently said via Twitter: “Don’t count on the new president to let up on compliance enforcement. CFPB and FTC staff won't change pro-consumer bias.”

One way managers and other industry professionals can handle the regulatory challenges that might be coming from the Consumer Financial Protection Bureau, the Federal Trade Commission or other places is by completing the Consumer Credit Compliance Certification Program offered by the National Automotive Finance Association.

“Well, I hate to say it, but I still think they’ll need to still continue to focus on compliance,” Hudson Cook partner Eric Johnson said in the video available here and at the top of this page. “It’s still all about compliance in both the near and the far-term future.”

“Now that (dealerships and finance companies) hopefully have their compliance management systems in place, they’ll need to make sure they’re keeping those maintained and updated as new laws, regulations and bulletins and enforcement actions come down from the CFPB,” continued Johnson, who along with fellow Hudson Cook partner Patty Covington serve as instructors of the NAF Association’s program.

“It’s going to be about compliance for the foreseeable future,” he added.

The NAF Association’s certification program is designed to provide the compliance professional with a solid working knowledge of the federal laws and regulations that govern consumer credit, together with a representative overview of state consumer credit law.

The program consists of four modules — two presented in an in-person classroom setting and two in an online format at the student’s own pace. Each module includes multiple sessions; and each session provides a thorough outline and description of the applicable law or regulation. Each session is followed by an online test that must be passed to receive credit for the session.

Another industry professional who completed the program is Ron Keable, who is the Texas field manager for Automotive Compliance Consultants.

“Automotive Compliance Consultants believes it is imperative that its consultants in the field uphold the highest standards and stay abreast of the ever-changing regulatory landscape in retail automotive,” said David Missimer, the firm’s general counsel about Keable’s certification.

“Dealership personnel rely on our consultants daily to assist them with their compliance needs. As such, each professional working for Automotive Compliance Consultants is expected to continue their education, and not only rely on what they may have learned a decade ago,” Missimer continued.

Automotive Compliance Consultants is a member of the NAF Association and recognizes the importance of membership in national and state associations like it that are dedicated to the automotive and finance industry.

“As a company, we believe if you provide compliance to dealerships, but you take no part in associations like NAF you are doing your customers a disservice,” Missimer said.

The NAF Association is hosting another opening model session. The event is set for Feb. 2-3 in Plano, Texas. Complete registration details are available here.

Companies such as Automotive Compliance Consultants will continue to have its consultants certified as consumer credit professionals in the NAF Association program.

“Compliance at dealerships will remain a focal point of state and federal agencies despite the election results. Compliance is just plain good business, and we want our people in the field not only to be good at what they do but be certified professionals,” said Automotive Compliance Consultants president Terry Dortch.

“This company is committed to making continuing investments like NAF training to bring increasing value to our customers,” Dortch added.

When reading through an email message or some other kind of material, the voice of the person who compiled it will stream through my mind if I know the individual’s tone and delivery.

Not sure if this phenomena happens to other people or if it’s just the condition I have after more than 40 years of television, radio, movie and other media consumption.

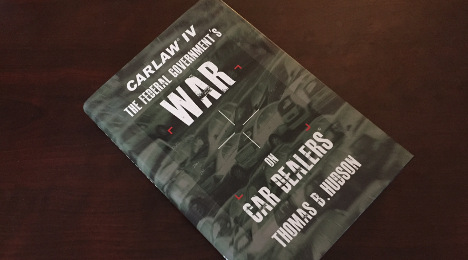

This scenario unfolded as a read through Tom Hudson’s latest book. And for me, it made the great composition by the Hudson Cook chairman all the more enjoyable.

While Cherokee Media Group was on hiatus from publishing our daily e-newsletters during the closing days of 2016, I had the opportunity to read Tom’s latest work — CARLAW IV, The Federal Government’s War on Car Dealers. Tom was kind enough to share a copy for this review, and to say the least, he gave me a wonderful Christmas gift.

If you ever have heard Tom speak, you know he mixes his witty humor with whatever relevant facts and precedents are germane to the specific top he might be discussing. After delving through the book, the anecdotes and analysis he shares about federal and state regulatory activities going back nearly 10 years offered keen insight into where the industry currently stands.

Tom explained how the Consumer Financial Protection Bureau germinated into the regulatory behemoth it now is while other agencies have taken notice and intensified their overseeing activities regarding the financing and delivery of vehicles by dealerships and credit providers.

Tom acknowledged he compiled this work because he’s been practicing law “since the invention of dirt.”

Industry participants both experienced and “green peas” can benefit through the more than 300 pages of material Tom assembled.

The work is broken up nicely so that if you don’t have the opportunity to read it straight through, you can pause and pick it up later and continue nicely. The book contains other elements such as an industry lexicon that make it a resource on par with anything else available.

If you’ve read this far, please do not consider this commentary simply a free advertisement for Tom’s book. His knowledge and reputation certainly are at a level where he doesn’t need someone like me to shill for him.

Rather, I wanted this review to serve as a recommendation to an industry who has some players who believe agencies such as the CFPB will simply disappear once President-Elect Trump assumes control of the White House in a little more than a week.

I assure you, a host of skilled and well-informed experts have conveyed to me that situation is unlikely to unfold no matter how many times Trump tweets.

The investment needed to acquire and navigate through Tom’s latest work are well worth it. Even if you think you know the auto finance world inside and out, I assure that Tom has at least a few nuggets of information in this book you might not already know.

I would even go so far as to recommend the newest employees at your dealership or finance company delve into the material. Perhaps they are assigned reading time of 30 minutes a day during their first month on the job to read a few segments at a time. For individuals new to the industry, they would have a knowledge foundation that could make them an even better asset to your operation.

For individuals traveling to New Orleans later this month for the annual events hosted by the American Financial Services Association and the National Automobile Dealers Association, I have no doubt Tom can tell you more about how to secure your copy. For those not making it to the Big Easy, go to this website.

Happy reading and all the best to you for 2017 and beyond.

Nick Zulovich is senior editor of SubPrime Auto Finance News and can be reached at [email protected].

In an action one of the credit bureaus acknowledged through a filing with the Securities and Exchange Commission, the Consumer Financial Protection Bureau confirmed on Tuesday that it took action against Equifax, TransUnion and their subsidiaries for what they regulator deemed to be “deceiving consumers” about the usefulness and actual cost of credit scores they sold to consumers.

The CFPB asserted the companies also lured consumers into costly recurring payments for credit-related products with “false promises.”

The CFPB ordered TransUnion and Equifax to “truthfully represent” the value of the credit scores they provide and the cost of obtaining those credit scores and other services. Between them, TransUnion and Equifax must pay a total of more than $17.6 million in restitution to consumers, and fines totaling $5.5 million to the CFPB.

“TransUnion and Equifax deceived consumers about the usefulness of the credit scores they marketed, and lured consumers into expensive recurring payments with false promises,” CFPB director Richard Cordray said. “Credit scores are central to a consumer’s financial life and people deserve honest and accurate information about them.”

The CFPB determined that TransUnion — since at least July 2011 — and Equifax (between July 2011 and March 2014) violated the Dodd-Frank Wall Street Reform and Consumer Financial Protection Act by:

— Deceiving consumers about the value of the credit scores they sold: In their advertising, bureau officials insisted TransUnion and Equifax falsely represented that the credit scores they marketed and provided to consumers were the same scores finance companies typically use to make credit decisions. They stressed that, in fact, the scores sold by TransUnion and Equifax were not typically used by finance companies to make those decisions.

— Deceiving consumers into enrolling in subscription programs: In their advertising, the regulator said TransUnion and Equifax falsely claimed that their credit scores and credit-related products were free or, in the case of TransUnion, cost only “$1.” In reality, the CFPB determined consumers who signed up received a free trial of seven or 30 days, after which they were automatically enrolled in a subscription program. Unless they cancelled during the trial period, consumers were charged a recurring fee — usually $16 or more per month. This billing structure, known as a “negative option,” was not clearly and conspicuously disclosed to consumers.

The bureau added that Equifax also violated the Fair Credit Reporting Act, which requires a credit reporting agency to provide a free credit report once every 12 months and to operate a central source — AnnualCreditReport.com – where consumers can get their report.

Until January 2014, the bureau found consumers getting their report through Equifax first had to view Equifax advertisements. The CFPB said this practice violates the Fair Credit Reporting Act, which prohibits such advertising until after consumers receive their report.

More details of enforcement action

Under the Dodd-Frank Act, the CFPB reiterated that it is authorized to take action against institutions engaged in unfair, deceptive, or abusive acts or practices, or that otherwise violate federal consumer financial laws. Under the consent orders, TransUnion and Equifax must:

— Pay more than $17.6 million in total restitution to harmed consumers: TransUnion must provide more than $13.9 million in restitution to affected consumers. Equifax must provide almost $3.8 million in restitution to affected consumers. The companies must send notification letters about the restitution to affected consumers.

— Truthfully represent the usefulness of credit scores it sells: TransUnion and Equifax must clearly inform consumers about the nature of the scores they are selling to consumers.

— Obtain the express informed consent of consumers: Before enrolling a consumer in any credit-related product with a negative option feature, TransUnion and Equifax must obtain the consumer’s consent.

— Provide an easy way to cancel products and services: TransUnion and Equifax must give consumers a simple, easy-to-understand way to cancel the purchase of any credit-related product, and stop billing and collecting payments for any recurring charge when a consumer cancels.

— Pay $5.5 million in total penalties: TransUnion must pay $3 million to the Bureau’s civil penalty fund. Equifax must pay $2.5 million to the bureau’s civil penalty fund.