Auto defaults climb for the first time in 2021 — barely

For the first time this year, S&P Dow Jones Indices and Experian spotted a rise in auto defaults.

But the uptick analysts noticed was the smallest amount possible.

For the first time this year, S&P Dow Jones Indices and Experian spotted a rise in auto defaults.

But the uptick analysts noticed was the smallest amount possible.

If finance companies based their decisions on how to run and staff their collections and recovery departments based only the metrics included in the S&P/Experian Consumer Credit Default Indices, they truly might be a one-man — or woman — band within their operations.

Perhaps when auto-finance executives thought defaults couldn’t get any lower, the industry responded with, “Hold my beer!”

According to the newest data compiled by S&P Dow Jones Indices and Experian, auto defaults now are at the lowest reading ever recorded.

Perhaps the next round of coffee or drinks should be in celebration for the collections departments at auto-finance companies.

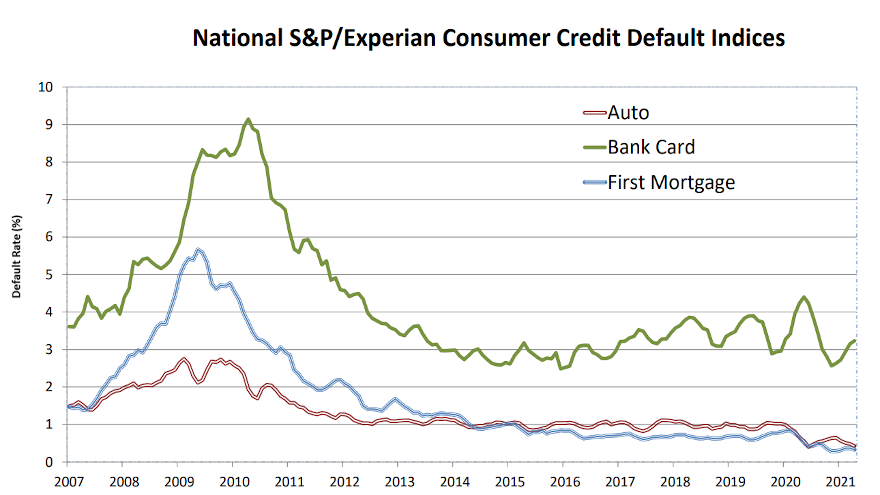

The auto portion of the S&P/Experian Consumer Credit Default Indices declined again in April and now sits just 3 basis points away from the all-time low recorded by S&P Dow Jones Indices and Experian.

According to data through April released on Tuesday, the auto default rate dropped another 5 basis points to 0.43%. It’s now 21 basis points lower than December’s reading of 0.64%.

Fueled in part by extensions, deferments and other accommodations offered by finance companies because of the pandemic, analysts noted the all-time low arrived last summer when a 16-basis-point drop from May to June created the unprecedented low reading of 0.40%.

The default rate hasn’t been above 1% since the close of 2019 with S&P and Experian pegged it at 1.02%.

Turning back to the newest data, analysts determined the composite rate — which represents a comprehensive measure of changes in consumer credit defaults — dipped 4 basis points lower to settle at 0.50%.

S&P and Experian mentioned the first mortgage default rate also decreased 4 basis points to 0.33%, while the bank card default rate climbed 8 basis points to 3.23%.

Turning next to the five major metropolitan statistical areas analysts track for this monthly update, they found that four produced lower rates in April compared to the previous month.

Miami generated the largest drop, falling 19 basis points to 1.04%. Chicago decreased 9 basis points to 0.50%, while Dallas softened by 8 basis points to 0.51%.

New York edged 3 basis points lower to 0.83%.

Los Angeles was the only major city that increased, ticking up two basis points to 0.52%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

S&P Global Ratings recently discussed two topics quite relevant to finance companies: contract extensions and resulting defaults as well as actions at the Federal Reserve.

Analysts discovered that as of February, extensions on auto-finance contracts contained in public asset-backed securities (ABS) fell to their lowest levels since the pandemic started, but they remained higher than year-ago levels.

For the public prime pools S&P Global Ratings track using Reg AB II loan level data, the monthly average extension rate decreased 6 basis points to 0.40% from 0.46%.

For public subprime pools, the decline was much more dramatic. Analysts found that they dropped 110 basis points to 2.40% from 3.50%.

“We attribute the improvement to stimulus checks that were paid in January and the economic recovery,” analysts said in a news release noting that 379,000 jobs were added in February as unemployment inched downed to 6.2% from 6.3% that month.

Nonetheless, S&P Global Ratings pointed out that public prime and subprime extensions remained higher than February 2020 levels of 0.32% and 1.53%, respectively, “as the job market hasn’t returned to pre-pandemic levels, especially in the leisure and hospitality sectors,” according to analysts.

S&P Global Ratings also tracked the vintage cumulative charge-offs of contracts extended each month since January 2020.

Analysts found that those contracts extended last March and April have had lower cumulative default rates than those loans extended in January and February of 2020.

In prime, S&P Global Ratings indicated the cumulative charge-off rate of contracts extended in April 2020 — what the firm said was the peak month of extensions — is 2.1% through February of this year.

In subprime, analysts indicated the cumulative charge-off rate of contracts extended in April 2020 is 8.0%.

After the latest moves by the Federal Open Market Committee (FOMC), expectations strengthened for interest rates to remain low for two more years.

S&P Global Ratings concurred with other experts, saying in another news release that there is still a substantial recovery that needs to come about before the Fed will ease up on its current monetary policy stance.

Unlike the Great Recession, which was triggered by a housing bubble, S&P Global Ratings emphasized that the 2020 recession had its origins in a pandemic. Efforts to control the spread of COVID-19 led to a partial lockdown of the economy, which, in turn, froze the financial markets, according to firm experts.

As the crisis has unfolded, S&P Global Ratings explained the focus of policymakers was one of prioritizing smooth market-functioning to minimize market dislocations. For the most part, they were able to execute this strategy effectively.

“Now that the stress level in the financial markets has subsided to lower-than-average levels, the Fed’s focus has shifted to returning the economy to a state of maximum ‘inclusive’ employment,” S&P Global Ratings senior economist Satyam Panday said.

Panday noted that current core personal consumption expenditure inflation stood at 1.4% as of February, while the unemployment rate came in at 6.0% in March, versus 3.5% before the pandemic, which was the lowest in a half-century.

As a result, Panday stressed the Fed is still far from its dual goal of sustained inflation of 2% and maximum employment.

“In our view, tapering of asset purchases is likely to begin in 2022, and policy rate liftoff should occur in 2023 once maximum employment is achieved and inflation reaches 2% and is on track to moderately exceed 2% for some time,” Panday said.

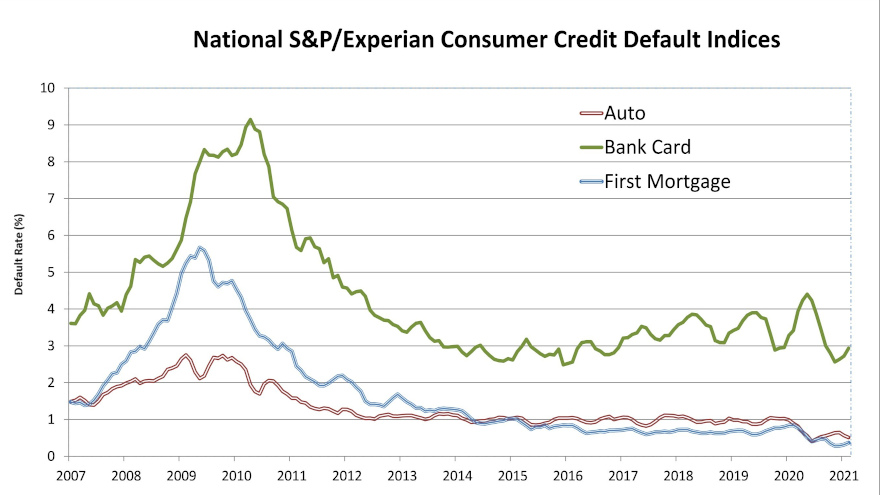

The auto default rate now has been below the 1% level for 15 consecutive months, according to data assembled by S&P Dow Jones Indices and Experian.

The streak continued thanks to a small dip in the auto segment of the S&P/Experian Consumer Credit Default Indices released earlier this week. Based on data through March, the auto default rate edged 3 basis points lower to 0.48%.

The last time the auto default rate sat above 1% was in December 2019 when analysts pegged it at 1.02%. Six months later, thanks to the pandemic and accommodations provided by finance companies, the rate dropped by more than half to an all-time low of 0.40%.

Meanwhile, analysts indicated the March composite rate — a comprehensive measure of changes in consumer credit defaults — ticked 1 basis point higher to 0.54%.

While the first mortgage default rate was unchanged at 0.37%, S&P and Experian discovered the bank card default rate rose 22 basis points to 3.15%.

Looking at the five large metropolitan areas analysts track for each update, four of those five cities generated higher default rates in March compared to the previous month.

Miami led the way with an increase of 7 basis points to 1.23%, while Los Angeles was right behind with a rise of 6 basis points to 0.50%.

Chicago moved 4 basis points higher at 0.59%, and New York ticked up 3 basis points to 0.86%.

The last city in the rundown — Dallas — remained unchanged at 0.59%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

Defaults are a bad outcome for both lenders and borrowers, and research shows that the mismatched timing between a person’s income and their bills is one of the most common reasons for these financial shortfalls.

A new behavioral science experiment conducted by Duke University’s Common Cents Lab with customers of Beneficial State Bank (BSB) shows a simple, creative way that banks can reverse this trend and reduce defaults by eliminating mismatches.

While banks cannot influence borrower externalities like the loss of a job or a medical emergency that might lead to a missed payment or default, they are better positioned to address income and expense mismatches.

Auto loans in particular can be challenging for income flows because the default monthly payment date is almost always the day a vehicle is purchased. And while loan payments are due on a specific date every month (e.g., the 15th), many people are paid on certain days of the week (e.g., every other Friday).

To help close this gap, a text-able recurring payments form was designed for BSB borrowers so they could sync the autopay of their loans with their income. The experiment randomized over 1,000 new BSB auto loan customers into either a control group or an experimental group. During BSB’s required welcome call for new loan recipients, the experimental group was texted a recurring payments form to help them sync payments with income. The control condition did not get the form.

The form made it easy to make multiple payments because smaller payments often help with budgeting. For example, if a monthly auto loan payment was $397 (the average in the U.S. for a used car), a borrower could choose to do two smaller payments of $198.50. Since millions of people get paid weekly, they could even split it into four weekly payments of $99.25.

Importantly, while both the control and experimental groups reported high interest in the program, those in the experimental group who received the enrollment form were 2.3 times as likely to enroll in automatic payments. The members of this group were also more likely to divide their payment into smaller sub-payments that synced with income.

As a result, the experimental group performed far better in terms of defaults, on-time payments, and total payments. None of the members in the experimental group defaulted on their loan while 17 members in the control group defaulted. The synced group also paid sooner — an average of 1.4 days before the due date compared to 2.75 days after the due date for the control group – which meant fewer late fees. And by the study’s conclusion, the experimental group had paid 100% of their loan payments while the control group had paid an average of 94.2% of their total loan payment.

Small changes in an approach like this — rooted in natural human preference and inclinations — are a highly effective way to positively impact people’s lives. For someone whose income is tight, knowing there will be money in the bank when a loan payment is due makes it easier to confidently sign up for autopay, which can then have additional long-reaching impacts.

When even a single late payment on your car loan can result in late fees and damage to a credit score, autopay can be a tremendous advantage. Not to mention the worst-case scenario of repossession, which can jeopardize a person’s ability to work and earn an income.

At the same time, beyond avoiding missed or late payments, syncing payments can also help to pay off an auto loan faster, a win-win for both the borrower and the lender.

The great news is that building a program to time loan payments with income is an easy one to institute for most banks and lenders. It requires a minimum of time and investment, can be rolled out across multiple loan types and platforms, and produces immediate and obvious bottom-line benefits.

Ultimately, implementing behaviorally informed solutions like these are simple, effective ways to produce good outcomes for everyone involved.

Richard Mathera, Lindsay Juarez, and Kristen Berman are part of the Common Cents Lab at Duke University.

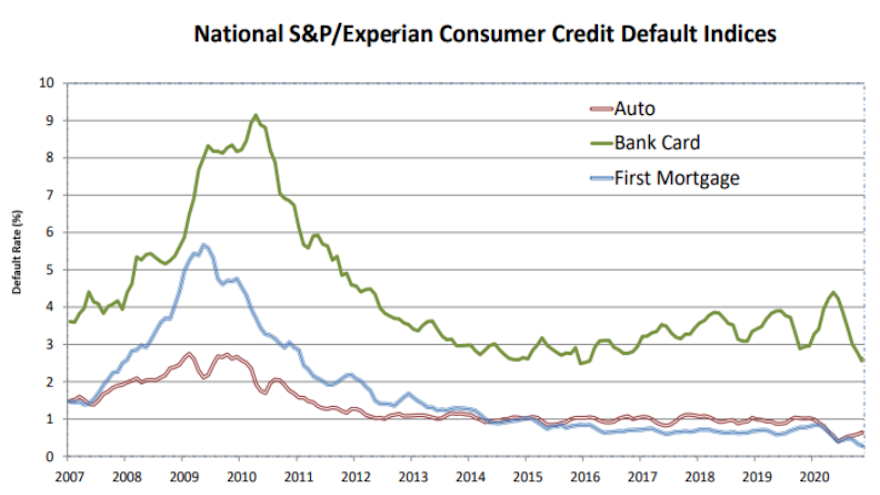

It probably wouldn’t be surprising if finance company executives and managers looked at the latest auto default reading from S&P Dow Jones Indices and Experian and responded by saying, “What? Wait a second. Really?”

According to data through February for the S&P/Experian Consumer Credit Default Indices, auto defaults dropped for the second month in a row to settle at 0.51%. That’s five basis points lower than January and 13 basis points below December’s reading.

And the February mark is beginning to approach the neighborhood of the all-time low registered in June, when analysts pegged it 0.40%.

What about past February readings before the pandemic began to influence so much in the credit world? Glad you asked. According to past data from S&P Dow Jones Indices and Experian, auto defaults during the second month of the year were as follows:

2020: 0.89%

2019: 0.99%

2018: 1.09%

2017: 1.05%

2016: 1.06%

2015: 1.06%

2014: 1.03%

2013: 1.11%

2012: 1.22%

2011: 1.58%

Turning back to the newest information, analysts reported the composite rate — a comprehensive measure of changes in consumer credit defaults — moved counter to the auto segment, rising 5 basis points at 0.53%.

Analysts also discovered the bank card default rate rose 21 basis points to 2.93%, while the first mortgage default rate climbed five basis points to 0.37%.

Finally, all five of the major metropolitan areas that analysts track for the monthly report rose in February.

New York generated the highest increase, climbing 34 basis points to 0.83%, while Miami rose 21 basis points to 1.16%.

Los Angeles jumped by 12 basis points to land at 0.44%.

Analysts said Chicago and Dallas each edged up 2 basis points, to 0.55% and 0.59%, respectively.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

Perhaps one of the clearest data examples of how extensions or other contract modifications impact delinquencies and defaults within a short timeframe arrived this week courtesy of S&P Global Ratings, S&P Dow Jones Indices and Experian.

First, let’s look at the extensions recorded in December on auto financing within public asset-backed securities (ABS). S&P Global Ratings discovered they increased significantly.

For the public prime pools that analysts track, extensions soared 32.5% to 0.73%. For public subprime pools, they jumped 19.2% to 4.84%.

S&P Global Ratings attributed the increases to the following factors:

• Normal seasonal behavior due to customers often falling behind on their credit obligations at year-end

• COVID-19-related impact as many consumers remained out of work or had their hours trimmed due to business restrictions to combat the rise in infection rates

• Finance companies giving contract holders more time to make their payments as many individuals would receive stimulus checks of $600 per person (and an additional $600 per child) in January.

With December’s spike in extension rates, S&P Global Ratings reported that deferrals reached their highest levels since the summer.

On average, analysts said 60% of the prime accounts (on a dollar basis) that were 60-plus-days delinquent as of the end of December were accounts that were previously extended since March. In subprime, analysts noted the percentage was 68%.

“Early indications are, however, that January will show a significant improvement,” S&P Global Ratings said.

Well, speaking of January information, S&P Dow Jones Indices and Experian released their data through January for the S&P/Experian Consumer Credit Default Indices.

The auto default rate dropped 8 basis points on a sequential basis to 0.56% in January. That reading is 43 basis points lower than a year ago.

Auto defaults haven’t been above 1% in this monthly tracker since the close of 2019 when analysts pegged it at 1.02%, closing a stretch of four consecutive months at 1% or higher.

The lowest auto default reading ever recorded by S&P Dow Jones Indices and Experian came in June when modification soared because of the pandemic. It bottomed out at 0.40%, then rose for five straight months.

Meanwhile, the composite rate — which represents a comprehensive measure of changes in consumer credit defaults — moved 2 basis points higher in January compared to the previous month to land at 0.48%.

In other credit segments, analysts reported the bank card default rate rose 9 basis points to 2.72%. and the first mortgage default rate ticked up 3 basis points to 0.32%.

Looking at the five largest cities S&P Dow Jones Indices and Experian track each month, four generated higher default rates in January versus the previous month.

Miami increased the most with a gain of 9 basis points to come in at 0.95%, while New York wasn’t far off that pace, rising 7 basis points to 0.49%.

Chicago and Dallas each edged up 1 basis point to 0.53% and 0.57%, respectively.

Los Angeles was the only one of these five metropolitan areas to show a decrease, dipping 3 basis points to 0.32%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

Much on the default front remained unchanged to close 2020.

Among the readings to finish the last year in that category was auto default.

According to data through December released Tuesday by S&P Dow Jones Indices and Experian, the December auto default metric came in at 0.64%, which was unchanged from November.

The reading, however, was 38 basis points lower than the last month of 2019. Analysts pinpointed the December 2019 reading at 1.02%.

December’s mark remaining unchanged also broke a streak of five consecutive months of climbing auto defaults. The upward move began with a record low posted in June at 0.40%

For more perspective, a decade earlier, the auto default reading landed at 1.77% in December 2010.

Elsewhere in the newest information analysts shared on Tuesday, the composite rate of the S&P/Experian Consumer Credit Default Indices — which represents a comprehensive measure of changes in consumer credit defaults — also stood pat in December, coming in at the exact same mark as autos at 0.64%.

While the first mortgage default rate ticked up 1 basis point higher to 0.20%, S&P and Experian noticed that the bank card default rate made the most significant move to finish 2020, rising 7 basis points to 2.63%.

Meanwhile, two of the five major metropolitan areas analysts track registered unchanged readings in December.

Dallas and Miami both stayed steady at 0.56% and 0.86%, respectively.

S&P and Experian noted that both Los Angeles and Chicago each decreased 2 basis points, to 0.35% and 0.52%, respectively.

New York went counter to the other four cities, but only slightly, as analysts spotted the default increase for the Big Apple at just 1 basis point to 0.42%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.