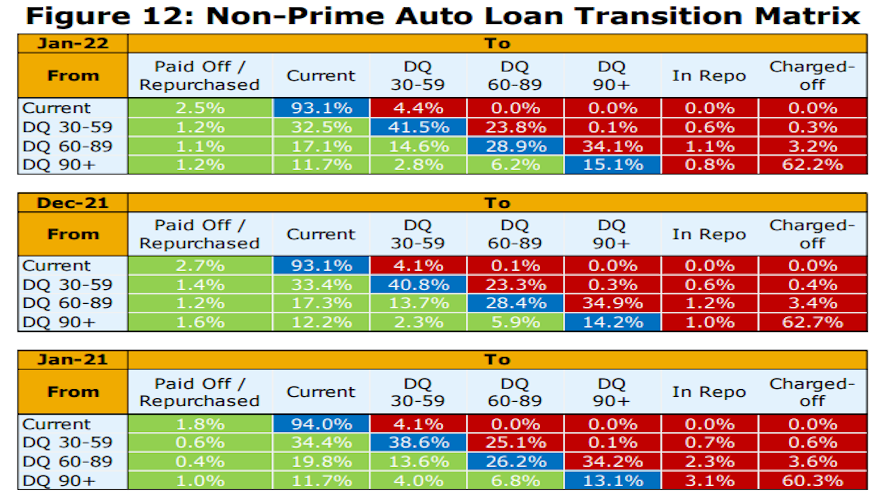

Kroll Bond Rating Agency had the opportunity to use an adjective to describe its latest auto-finance data that’s quite familiar to executives and managers.

Analysts included the word “seasonal” when recapping its January indices that are based on information accumulated through the securitization market.

“January remittance reports showed weaker credit performance across prime and non-prime auto loan pools during the December collection period as the seasonal impact of holiday spending weighed on consumer budgets,” KBRA said in its latest report.

Analysts determined annualized net losses in KBRA’s prime auto loan index increased a “modest” 2 basis points month-over-month to 0.25%, while the percentage of borrowers that were 60+ days past due remained flat at 0.35%.

Meanwhile, analysts found that annualized net losses and 60-day delinquency rates in KBRA’s non-prime index increased at a much faster pace, jumping 91 basis points and 41 basis points month-over-month to land at 5.44% and 4.88%, respectively.

KBRA pointed out that continued strength in the used-vehicle market has pushed recovery rates to historically high levels.

Analysts noted that prime and nonprime recovery rates began to normalize during the second half of 2021, but still remain elevated in January, coming in at 58.3% and 51.9%.

“We expect credit performance to continue to weaken in both indices throughout 2022, as inflationary pressures and the remaining wind down of stimulus programs weigh on consumer balance sheets,” analysts said.

“However, tight labor markets, excess savings built up throughout the pandemic, and the approaching tax refund season should help to hamper any meaningful deterioration in credit over the coming months,” KBRA added.

More evidence that consumers maintaining their monthly payments for their vehicles is continuing to wobble arrived this week from Kroll Bond Rating Agency (KBRA).

In its latest analysis looking at the automotive securitization market, KBRA found that December remittance reports showed mixed credit performance across prime and non-prime auto pools during the November collection period.

Read more

Delinquencies and losses should be the canary in the coal mine for performance trends, but they can also wag the dog, drawing attention away from looming issues. In subprime lending, borrowers could demonstrate the first indications of trouble for the economy at large, as economic issues tend to impact them first.

Now, as auto loan forbearance programs and extended unemployment benefits and stimulus checks have run out, one would expect the subprime auto sector (more than the prime) to start to show some cracks. Yet losses and delinquencies remain modest.

Still, 2022 remains a wait-and-see game with inflation rising, creating challenges to subprime consumers’ wallets, and the uncertainty of just how long it will be before new car supply improves enough to ease stratospheric used vehicle prices.

Let’s look at the numbers to close out the year.

Originations and issuances, by the numbers

Even if vehicles are hard to come by, the cost of acquiring one has been on the rise. New car prices are up 8.9% but used car prices have risen 39.8% since March 2020. Even at the time of year when things quiet down, this market is still hot. Prices rose for the first time in 25 years between September and October.

It’s no wonder then that total auto loan debt increased to $1.44 trillion in Q3 2021, up from last year’s $1.36 trillion in Q3 2020. It accounted for 9.4% of the $15.24 trillion in national household debt.

While new auto loan originations decreased slightly from $202 billion in Q2 to $199 billion in Q3 as the NY Fed reported, this was the result of higher origination amounts in Q2 rather than more loans originated. $33.8 billion of that total by volume represents subprime auto loan originations (credit score <620). The share of subprime loans remained steadily around 17% of the total dollar amount in Q2 and Q3.

Subprime auto originations retreated greatly in 2020, but 2021 has shown a rebound, although still not yet at pre-pandemic levels. In Q2 2020, this sector was hit the hardest, so comparing the growth rate year-over-year for subprime auto originations to Q2 2021 shows a large boost of 32.8% according to TransUnion. But that was working back from a deficit. The subprime growth rate in Q2 2020 was -16.7%. The growth rate for Q2 2021 is 5.9%.

Subprime auto ABS has been active as well. Overall auto ABS issuance is at a 10-year high with $92 billion. Focusing on subprime auto ABS, FINSIGHT tracked $42 billion in new subprime auto ABS issuance in 2021, which trounces 2020’s $27.6 billion in issuance.

With 64 deals already complete in 2021, that is well above the pre-pandemic level of 57 deals in 2019 and reflects a 10-year high in FINSIGHT data.

Performance and practice

As expected, with government aid ending in 2021, we are starting to see delinquencies rise again. Subprime 60+ day delinquencies peaked at 4.17% in January 2021, declining to a low in 2021 of 2.58% in May only to increase again to 3.76% in October 2021.

But comparing subprime 60+ day delinquency rates year-over-year, they remain below the pre-pandemic rates. Looking at September 2021, the delinquency rate increased to 3.69% in September from 3.59% in August, but this was still lower than 5.23% for September 2019.

Losses too are on the rise. Subprime auto annualized net loss rates for deals tracked by Fitch reached 5.59% at the start of the year, down from 9.47% the previous year. Falling to a yearly low of 1.84% in May, they are climbing back up to 4.20% in October 2021.

S&P saw similar trends with net loss rates at 4.11% in September 2021, but this again remains well below pre-pandemic losses, which were 8.55% in September 2019.

S&P even sees some positives in the future to keep these numbers in check, noting improvements in employment, the child tax credit payments that families have begun to receive, and the strength in used car prices. However, as KBRA suggests, the usual holiday spending plus the end of government-sponsored pandemic benefits will create headwinds for the sector in the coming months.

Looking ahead

The market’s fate in 2022 may be resting on the slim edge of a microchip. If chip supply comes back on line, new vehicles enter the market without outpacing demand, used vehicle prices may remain steady at their relatively high levels, continuing to buoy collateral values and perhaps consumer optimism (as owner of a high value assets).

But there is the potential for a much darker alternative reality. New vehicle supply comes back strong, subprime consumers feel the sting of being upside down as used vehicle prices drop (in some cases off of record prices they’ve paid), the prospect of negative equity dampens new vehicle sales, competition increases for fewer financings, in turn causing changes in underwriting standards and conduct at dealers. In short, carpocalypse. 2022 might not be the year for it, but it may be up ahead.

Joseph Cioffi is a partner at Davis+Gilbert in New York City where he is Chair of the Insolvency + Finance Practice Group, a multidisciplinary practice spanning corporate, insolvency and litigation. He has a unique perspective afforded by his experience in all stages of credit and market cycles, including in subprime lending investments, operations and litigation. Joseph and his group have been deeply involved in disputes and litigation resulting from the last financial crisis. Nicole Serratore, an attorney in the Insolvency + Finance Practice Group of Davis+Gilbert, assisted with this post that originally appeared on this website.

Kroll Bond Rating Agency (KBRA) and S&P Global Ratings each shared their latest observations of contract performance based on metrics collected through the auto ABS market.

Analysts at both firms spotted similar patterns.

Beginning with S&P Global Ratings, the firm said through a news release that U.S. prime auto ABS saw “strong” results in September, with even lower monthly annualized losses year-over-year due to high recovery rates.

S&P Global Ratings indicated prime month-over-month performance was relatively stable, while subprime performance results were “less favorable but still quite positive relative to historical metrics.”

Analysts determined subprime losses increased year-over-year but were still only about 50% of the September 2019 loss level.

Subprime delinquencies and losses also rose month over month, while recoveries declined, according to S&P Global Ratings.

“Both segments are reporting very low static pool cumulative net losses for the first-quarter 2020 though first-quarter 2021 vintages,” S&P Global Ratings analysts said.

The firm went on to mention “significant” year-over-year changes in the prime pool composition through September included the average FICO score declining slightly to 750 from 760 and used vehicles increasing to a record 63% from 59%.

Analysts added that the used-vehicle composition also increased in subprime pools.

“Of the 25 transactions we reviewed in October, we lowered our loss expectations on 19 and maintained them on six. These reviews resulted in 51 upgrades and no downgrades,” S&P Global Ratings analysts said.

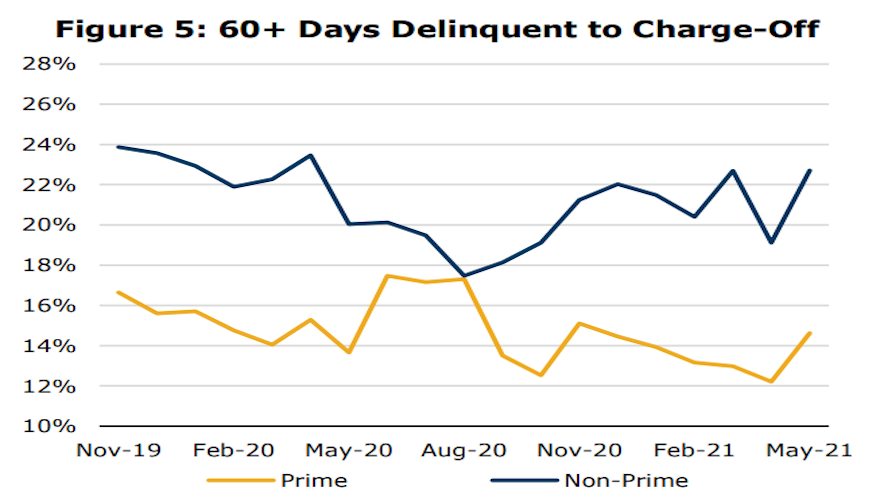

Turning next to KBRA’s analysis of October activity, the firm discovered that early-stage delinquencies (30 to 59 days past due) in KBRA’s Prime Auto Loan Index increased 4 basis points month-over-month to 0.84%, while late-stage delinquencies (60 days or past due) rose 1 basis point to 0.29% .

Furthermore, analysts said early- and late-stage delinquencies in KBRA’s Non-Prime Auto Loan Index were up 42 bps and 29 bps month-over-month, respectively, at 7.2% and 3.94%.

“Annualized net losses (ANL) trended somewhat higher in our prime index versus the previous month but remained relatively flat in our non-prime index. However, net loss rates remained well below pre-pandemic levels, as elevated used vehicle values have continued to support loan recovery rates,” KBRA experts said in their newest report.

“It is likely that securitized auto loan credit performance will continue softening into early next year, keeping in line with seasonal trends as holiday spending weighs on borrower finances,” they continued. “Moreover, the termination of extended federal unemployment benefits in early September 2021, coupled with the phasing out of other COVID-related safety net programs like federal student loan forbearance in January 2022, will likely create additional headwinds to consumer credit performance in 2022.”

KBRA closed its updated by noting the percentage of prime and non-prime contract holders who transitioned from current to 30 to 59 days delinquent totaled 0.5% in its prime index and 4.4% in its non-prime index.

Finally, the firm said the percentage of prime consumers who rolled from 60 days or more past due to charge-off equaled 12.5%, which was down 162 basis points month-over-month, while the non-prime roll rate into charge-off decreased 20 basis points to 19.3%.

After TransUnion released its Q3 2021 Quarterly Credit Industry Insights Report (CIIR), Satyan Merchant made a return appearance on the Auto Remarketing Podcast.

The senior vice president and automotive business leader at TransUnion not only delved deeper into the third-quarter metrics, but also gave perspectives on how much impact pandemic-triggered customer assistance programs have been based on the latest data.

To listen to the episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

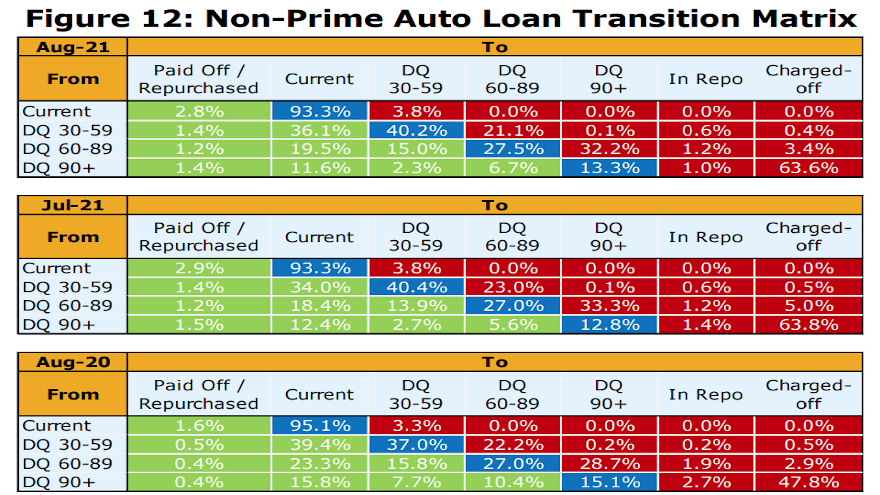

The word choices Kroll Bond Rating Agency (KBRA) used to describe its latest auto-finance indexes might be reassuring to executive and managers even if their collections are deteriorating.

KBRA reported on Monday that August remittance reports showed softening credit performance across securitized auto loan pools during the July collection period.

Read more

When analysts touched on delinquencies as a part of Experian’s latest State of the Automotive Finance Market report, the declaration they made about that particular metric likely pleased finance companies greatly.

However, for repossession agents and forwarding companies, the assertion might have reinforced their concerns about how soft their recovery activities are.

Experian indicated that more than 99% of outstanding auto-finance accounts that were current first quarter stayed current during the second quarter.

Analysts pegged the 60-day delinquency rate for the second quarter at 0.41%. That’s down from 0.44% during the same quarter last year and 0.62% in Q2 of 2019.

Experian went on to mention that the 30-day delinquency rate came in at 1.31% in Q2, which is actually up slightly from the Q1 rate of 1.26%. It was still much below the 30-day delinquency rate analysts noted during the second quarter of 2019, when it was 2.00%.

The financial services industry — including auto financing — is rebounding strongly from the early impacts of the COVID-19 pandemic, according to TransUnion’s Q2 2021 Quarterly Credit Industry Insights Report (CIIR).

In fact, analysts discovered the metric that many finance company executives might be watching closest nowadays — delinquencies — is at a rate on par with what they observed before the pandemic.

Read more

Kroll Bond Rating Agency (KBRA) highlighted how much federal stimulus money provided a positive bounce for maintaining monthly payments.

And according to the firm’s newest report, that bounce is losing its momentum, but the overall market still is solid as analysts said May remittance reports showed auto credit trends remained strong during the April collection period.

Read more

Nicholas Financial made quite a year-over-year rebound when detailing its 2021 fiscal year results last week, including vital metrics like net income and delinquency rates.

Despite a dip in total revenue, the subprime auto finance company reported that its net income for the fiscal year that ended March 31 jumped to $8.4 million compared to $3.5 million a year earlier, while its diluted net income per share went from $0.45 to $1.09 during the same stretch.

The improvements arrived even as Nicholas Financial said total revenue decreased 9.8% to $56.0 million during the 2021 fiscal year from $62.1 million generated in the previous fiscal year.

How did the company do it? Nicholas Financial reported that the company originated $88.2 million in finance receivables, collected $118.6 million in principal payments, reduced debt by a net amount of $35.3 million, repurchased $0.9 million of common stock and increased cash by $8.3 million.

“We are very pleased with our overall fiscal year-end results,” Nicholas Financial president and chief executive officer Doug Marohn said in a news release. “We continue to produce excellent portfolio performance, recognizing very low delinquency and net write-offs, the likes of which we have not seen in years.

“We were also able to enjoy year-over-year increases in both indirect and direct originations and loan volumes,” Marohn continued. “The year-over-year increase on indirect originations was the first we have seen since my return to Nicholas, and it was especially gratifying to see this during the pandemic.”

As Marohn referenced, Nicholas Financial cut its total delinquency rate in half by the finish of the 2021 fiscal year, slicing it to 5.67% from 10.22% a year earlier.

And the 7,307 contracts that came into its portfolio had similar characteristics as the previous fiscal year, including:

— Average term: 46 months versus 47 months a year earlier

— Average amount financed: $10,135 versus $10,035 a year earlier

— Average APR: 23.4% in both fiscal years

Nicholas Financial finished its 2021 fiscal year with 22,760 active contracts.

And just before the fiscal year closed, the company also opened a new location in West Jordan, Utah. Along with Utah, Nicholas Financial now is licensed in Arizona, New Mexico and Texas and has recently initiated expansion efforts in each of those states.

“It is with great pleasure we welcome the Salt Lake City market to our branch network,” Marohn said. “It is a wonderful area with great people and a robust economy, and we have assembled a very talented team to service both our dealer partners and borrowing customers. We are committed to growing our company, and one way we will do that is through growing our footprint throughout the United States.”

With plenty of positive momentum going into its 2022 fiscal year, Marohn is upbeat about Nicholas Financial maintaining and growing its presence in the subprime space.

“The ability to once again report substantially increased earnings is a testament to our core business strategy as well as to the hard-working men and women who execute that strategy every day,” Marohn said. “Our commitment to the branch-based model with a local office in every market we service allows us to better support our dealer partners and our borrowing customers. This approach has also facilitated the expansion of our direct loan products to virtually every NFI branch office.

“As we continue to increase our core product market share in the existing branch markets, we remain focused on growing the direct loan business, as well as expanding our branch network in western states.”