Kroll Bond Rating Agency (KBRA) is seeing the likelihood strengthen that seasonal payment patterns are coming; that some of your contract holders might purchase holiday gifts rather than maintain their monthly vehicle payment.

Analysts delved into the topic when they shared KBRA’s September index readings based on securitizations in both prime and non-prime.

Read more

Kroll Bond Rating Agency (KBRA) examined how states are modifying their use of federal unemployment benefit programs connected to the pandemic and identified four finance companies whose automotive securitizations might have the most resulting risk exposure.

Analysts recapped in a report distributed this week that a total of 26 states have announced plans to opt out of some or all of the federal unemployment benefit programs provided under the American Rescue Plan Act of 2021 (ARP).

Read more

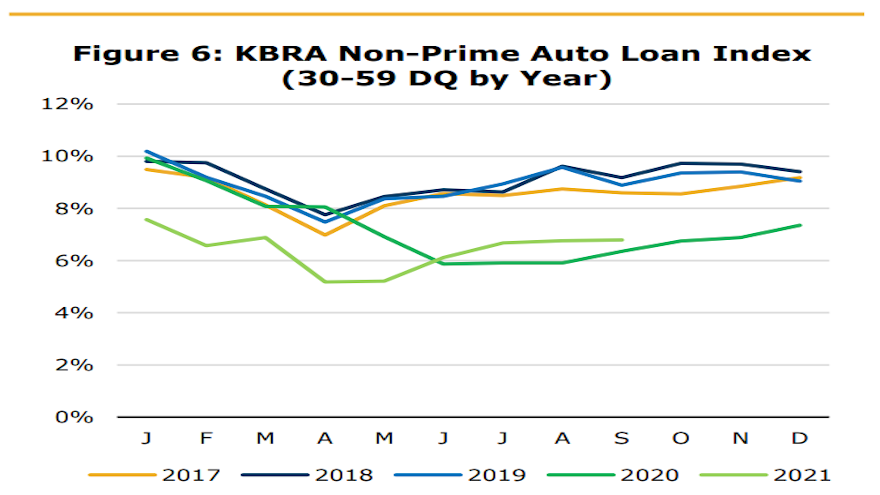

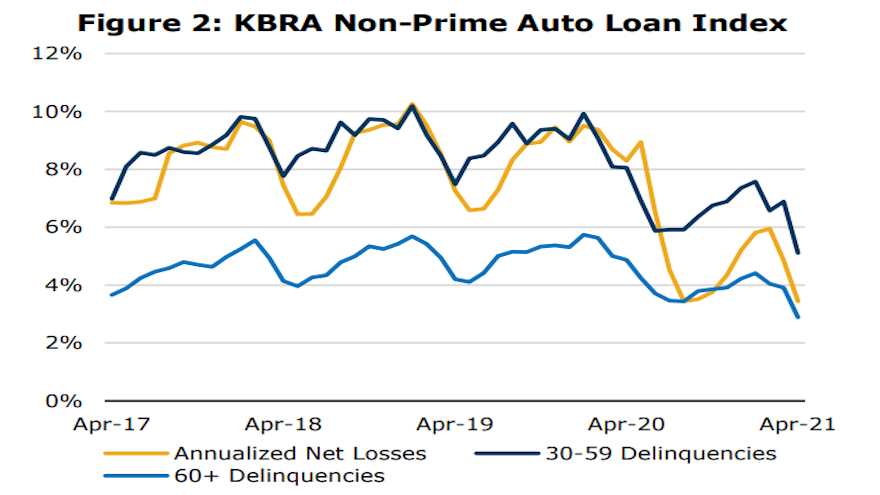

Kroll Bond Rating Agency (KBRA) used the descriptor “well grounded” when analysts dissected April remittance reports to discover the credit trends that surfaced during the March collection period.

KBRA indicated delinquencies for both non-prime and prime contracts decreased.

Analysts said in their newest report that early stage delinquencies — 30 to 59 days past due — in the KBRA Prime Auto Loan Index fell 23 basis points month-over-month to 0.67%, while late-stage delinquencies — more than 60 days past due — declined 11 basis points to 0.23%.

Meanwhile, the firm said early and late-stage delinquencies in the KBRA Non-Prime Auto Loan Index dropped 177 basis points and 102 basis points, respectively, coming in at 5.11% and 2.89%.

Analysts mentioned annualized net losses also trended lower in both indices during the month, “driven by favorable delinquency metrics and a frothy used-car market caused by strong demand and new vehicle production shortages, which has helped to keep recovery rates at elevated levels in 2021.”

KBRA also highlighted that contract prepayment rates rose sharply in March, mirroring a similar trend that analysts observed in other consumer loan sectors.

The firm determined prime and non-prime prepayments rose to 26.75% and 32.40%, respectively, up 13 percentage points and 11.8 percentage points versus the previous month.

“We expect the rise in prepayment rates to be transitory, as it is likely borrowers used the extra cash received from the third round of stimulus and tax rebates to pay down some of their outstanding debt during the month rather than accumulate savings as uncertainty is reduced and economic activity improves,” analysts said.

Furthermore, there was yet another upbeat metric to report. KBRA noted that its analysis of April’s Reg AB II asset-level disclosures showed improved credit metrics.

Analysts found that the percentage of prime and non-prime contract holders who went from 30 days delinquent to current rose to 47.9% and 44.9%, respectively. That’s up 1,323 basis points in prime pools and 1,634 basis points in non-prime pools versus the previous month.

And KBRA said the percentage of prime contract holders who slid from 60 days or more past due to charge-off dropped to 12.2%, down 77 basis points, while the non-prime roll rate into charge-off declined 357 basis points to 19.1%.

Colonnade Securities offered an extended examination of the below-prime auto finance industry this week, identifying what the independent investment bank focused on the financial services and business services sectors believes are four factors currently impacting the space most.

According to the report, the fundamentals of the below-prime auto finance industry have not deteriorated significantly, but the sector is now out of favor with traditional financial sponsors. In part, Colonnade cited four factors, including:

— Past aggressive underwriting has led to elevated delinquencies for some firms

— Private equity investors have hit the horizon of disappointment

— Bifurcation of the below-prime auto finance sector

— Access to capital

Colonnade explained a wave of investments in 2010 through 2012 led to heightened competition and looser underwriting, followed by a spike in delinquencies and losses. The result is a significant decrease in new equity capital available to the sector, according to the report.

“While banks that lend to the below-prime auto finance industry are more cautious and selective, senior debt availability remains strong for performing industry participants due, in large part, to the asset-backed securities market,” Colonnade said in a news release.

The investment bank added in the report, “The impact of liberal standards has been revealed in the performance of the asset-based securities issued by a few significant issuers.

Colonnade contends the industry has bifurcated between large providers with total receivables of more than $300 million and small below-prime auto finance firms. Colonnade insisted those large, well-run players continue to grow profitably while a few smaller firms have failed.

“These larger firms have invested in automated credit decisioning and data analytics that reduce static pool losses,” Colonnade said in its report. “The larger firms are also able to hire and retain skilled leaders and technical people needed to implement a tech-forward operation. “In addition, large firms have made significant investments in compliance staff and infrastructure.

“The second segment of the industry consists of smaller players that have not achieved critical mass and do not have the resources to invest in credit/analytic technology,” the bank continued in the report.

Colonnade recapped that few M&A transactions have been completed in recent years, although there have been some capitulations (business exits/liquidations). Several of the large, successful firms are still seeking change of control as their private equity owners run through their investment horizons.

“Sponsor-owned firms will eventually be sold due to the 10-year liquidation schedule of the typical private equity fund,” Colonnade added in its report.

Colonnade expects to see an uptick in mergers and acquisitions activity in the industry over the next 18 months as private equity investors are forced to take their properties to market.

“There will be transactions, but the valuations are unlikely to meet the original expectations of the investors,” the investment bank said in a news release. “These market dynamics will create compelling investment opportunities for long-term, yield-oriented investors, such as family offices and other non-traditional financial sponsors.”