TurboPass is continuing to build relationships with finance companies that specialize in subprime paper.

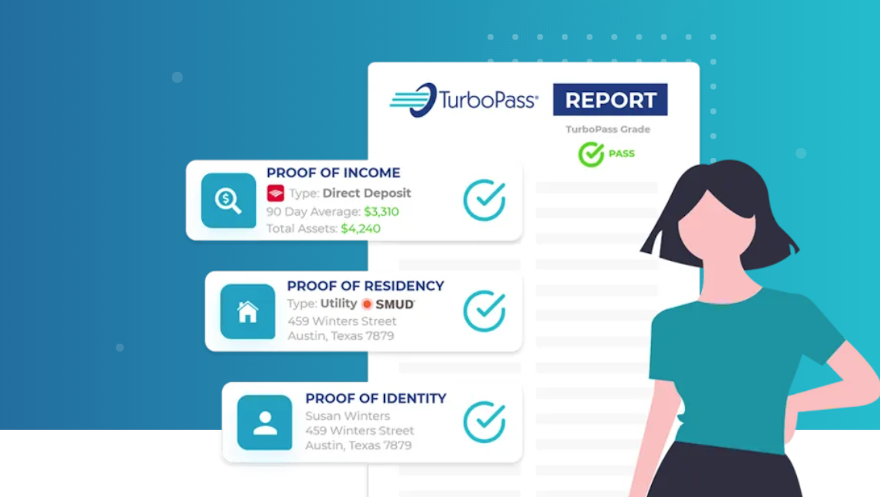

Soon after announcing a finalized strategic partnership with Turner Acceptance, TurboPass also shared that it’s working with Automotive Credit Corp. (ACC) to leverage its universal income validation solution and find more details about consumers’ ability to pay on a retail installment contract.

The companies highlighted that dealers can now send a simple text message to a consumer at the point of sale or during their shopping process to validate “ability” that’s ready in seconds, saving valuable time in the vehicle buying and closing process.

This process can enable finance companies to have funding dashboard access to validate dealer-initiated reports eliminating the need to send personal identification documents in the funding package.

“After analyzing alternatives and in light of the current unemployment situation, we are moving forward to sign up all of our dealers nationwide onto the TurboPass platform. This will allow dealers to collect income, employment and proof of residence data, streamlining the stip-clearing process to get deals done faster and to minimize incidents of errors and fraud,” ACC chief operating officer Mike Opdahl said in a news release.

Founded in Michigan in 1992, ACC has partnerships with thousands of dealers throughout the United States including Arizona, California, Colorado, Florida, Illinois, Indiana, Michigan, Minnesota, Nevada, Ohio, New York, and Utah.

“Our team members are happy to leverage this innovation because it helps our dealers succeed in many ways,” ACC business development director Michael Blasius said. “It also helps our underwriting teams make solid and fast decisions.

“With the new COVID realities, this novel method is not only customer-authorized and (trusted), it allows us to deliver great value to our dealership partners around the country,” Blasius went on to say.

TurboPass can eliminate the hassle and risk associated with document-based verification of income, employment and residence and provides trusted direct (bank and credit union) source data that can fulfill finance companies’ need for copies of bank statements, proof of income, proof of employment and other stipulations.

“The TurboPass report is a unique solution in the auto finance ecosystem. It’s something that our dealers have said is a long-time coming,” TurboPass co-founder and chief executive officer Mike Jarman said.

“In light of the coronavirus environment, verifying income and employment is difficult, yet more important than ever,” Jarman continued. “The fact that ACC, an innovative and important lender to so many used-car dealers in America, recommends and accepts TurboPass to clear stips and is now actively promoting its adoption to its thousands of dealers is both exciting for our company and indicative of where the industry is moving.”

For more details about the companies, go to automotivecredit.com and turbopassreport.com.

Davis & Gilbert partner Joseph Cioffi makes another podcast appearance to offer more insights about the Credit Chronometer report that surveyed executives from throughout the subprime auto finance sector about the space’s prospects to navigate through the coronavirus pandemic.

What Cioffi uncovered was the vast majority of survey participants remain upbeat, and he tells senior editor Nick Zulovich some of the reasons why.

To listen to the episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

The coronavirus pandemic is accelerating consumers’ recognition of more favorable financing terms in connection with used vehicles among other benefits of acquiring a pre-owned model instead of a new car.

That’s among the latest findings shared on Tuesday by Edmunds, which asserted that current unique market conditions due to COVID-19 could be driving more consumers out of the new market and into used vehicles.

Edmunds analysts reported that June used-vehicle finance figures and Edmunds website data indicate shifts in shopping behavior that are not usual for the used-vehicle market and could point to more typical new car shoppers entering the fray:

• Reduced interest rates. Edmunds data shows that interest rates for used vehicles dropped to the lowest level since January 2018 with the average annual percentage rate (APR) falling to 7.8% in June, compared to 8.3% in May and 8.6% a year ago.

• Bigger down payments. The average used down payment climbed to $3,167 in June, surpassing $3,000 for the first time that Edmunds has on record dating back to 2007.

• Less negative equity. Edmunds data reveals that 26.3% of used vehicle sales with a trade-in had negative equity in June, the lowest level so far in 2020.

• Increased cross-shopping of used vehicles. According to Edmunds website data, more new shoppers are cross-shopping used vehicles than before COVID-19. Edmunds also said 29% of new-vehicle shoppers between mid-May and mid-June also considered used, compared to 24% between mid-January and early March.

“More consumers are looking for value in their next car purchase due to the economic challenges of the coronavirus pandemic, so the more favorable loan conditions we’re seeing are likely a direct result of more consumers with good credit shifting into the used market,” Edmunds executive director of insights Jessica Caldwell said in a news release.

“Thanks to a shortage of new vehicle inventory, more automakers and dealers have leaned into promoting attractive certified pre-owned programs, which might be driving more typical new car shoppers into the used market,” Caldwell continued.

Edmunds data also indicated that the share of used vehicle purchases with a vehicle trade-in dropped in June to the lowest level since February 2009, which experts said could also be indicative of another trend emerging due to COVID-19: more first-time buyers.

“The fact that there are fewer people trading in a vehicle when making a car purchase could indicate that there are consumers entering the market for the first time — possibly due to concerns surrounding public transportation — which is an exciting prospect for the industry,” Caldwell said.

June Used-Car Finance Data (Averages)

|

|

June 2020

|

June 2019

|

June 2015

|

|

Term

|

67.3

|

67.4

|

66.3

|

|

Monthly Payment

|

$405

|

$411

|

$378

|

|

Amount Financed

|

$22,337

|

$22,181

|

$20,706

|

|

APR

|

7.8%

|

8.6%

|

7.7%

|

|

Down Payment

|

$3,167

|

$2,665

|

$2,217

|

Source: Edmunds

While the cost of new vehicles continues to climb, the newest data from Edmunds indicated finance companies are finding ways to mitigate their risk when booking new-model paper.

On Wednesday, Edmunds experts reported the average down payment for new vehicles financed in June rose to the highest amount seen all year, increasing to $4,451.

Furthermore, Edmunds determined the average contract term for the June new-car paper dipped below 70 months for the first time since February.

Edmunds also indicated interest rates for new vehicles increased slightly in June. The annual percentage rate (APR) on new financed vehicles averaged 4.2% in June, compared to 4% in May and 4.3% in April.

Despite this slight month-over-month increase, analysts noted that this is still the second-lowest average interest rate that Edmunds has on record since September 2015.

Edmunds data also shows that zero-percent finance offers took a dip for the second month in a row in June but remained at near-record levels. These deals constituted 19.4% of all new financed purchases in June, compared to 24% during the previous month.

“Although car shoppers still got to take advantage of favorable financing conditions in June, all signs point to automakers pulling back on the more generous incentives introduced at the outset of the pandemic,” Edmunds executive director of insights Jessica Caldwell said in a news release.

“As states across the country have reopened, consumers have resumed more of their regular purchasing habits, and as inventory levels decline, automakers understandably are less prone to spend big to spur demand,” Caldwell continued.

“It might not seem like a positive for car shoppers, but it’s probably for the best that loan terms are returning a bit closer to Earth after skyrocketing for months,” Caldwell went on to say. “At zero-percent financing, a six- or seven-year loan could make sense for a responsible buyer, but for many Americans, relying on longer loan terms to justify their bigger vehicle purchases could put them at greater risk for negative equity in the future.”

That negative equity stems in part to how much new vehicles costs nowadays.

ALG, a subsidiary of TrueCar, projected June average transaction prices (ATP) for new vehicles to be up 3.2% or $1,117 from a year ago but down 0.2% or $88 from May.

“Average transactions prices continue to tick up year-over-year, but we are seeing signs of decline and expect a small dip in average transaction price month-over-month as automakers slowly pull back from zero percentage financing over 84 months that helped spur demand for higher price models and trim levels,” ALG chief industry analyst Eric Lyman said in a news release.

“While incentives are still up year-over-year, the aggressive incentives that came out fast and furiously in April and May to help alleviate sales pains are beginning to soften due to low inventory and assembly plants that are still not back to full production,” Lyman continued.

“Retail sales over the Fourth of July holiday weekend will be the next big test of industry’s strength and resiliency and will be a litmus test for automakers in deciding to further pull back on incentives,” he added.

Meanwhile, the valuation analysts at Kelley Blue Book reported the estimated average transaction price for a light vehicle in the United States was $38,530 in June. They computed new-vehicle prices increased $1,141 (up 3.1%) from the same month last year, while rising $160 (up 0.4%) compared to last month.

“Though Q2 sales are expected to be down 35% due to COVID-19 and the ensuing economic recession, transaction prices over this time strengthened more than normal,” Kelley Blue Book analyst Tim Fleming said in a news release.

“The industry average climbed 3% — helped by increases in non-luxury cars —and light truck sales mix at around 75% of the total market,” Fleming continued. “Today’s new-car buyers are likely more financially secure despite the economic uncertainty, and they are purchasing a disproportionate number of trucks and SUVs. However, buyers are still shying away from luxury brands, which saw prices dip 1.5%.”

New-Car Finance Data (Averages)

|

|

June 2020

|

June 2019

|

June 2015

|

|

Term

|

69.9

|

69.7

|

67.9

|

|

Monthly Payment

|

$568

|

$562

|

$492

|

|

Amount Financed

|

$34,911

|

$32,824

|

$29,008

|

|

APR

|

4.2%

|

6.0%

|

4.6%

|

|

Down Payment

|

$4,451

|

$4,135

|

$3,308

|

Source: Edmunds

Launcher Solutions president Nikh Nath joined the podcast to share his views about a topic relevant not only to auto financing, but also likely all segments of the automotive space nowadays.

Nath, whose company is a technology provider specializing in loan originations, described the growing awareness of risk mitigation in light of many business functions being impacted by the coronavirus pandemic.

To hear the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

Darwin Automotive said this week that it released the final application needed for Virtual F&I orchestrated by JM&A Group.

Darwin highlighted that it’s giving the tool Documents on Demand for free to all new and previous dealer customers.

The company explained Documents on Demand includes the following features and functionality:

• Flex Forms: All dealership documents can be uploaded into the system and printed as PDFs.

• Usign: All documents that allow for electronic signature can be mapped within the application by the user with just a few clicks. This includes installment agreements that allow for e-signature collection.

• Smart Stips: This feature allows the manager to send a secure link to a customer so they can upload items including proof of residency or insurance, driver’s license, etc., from any device. They are then stored in Darwin’s electronic deal jacket.

• Signing: A single signing ceremony can happen in one place that includes all deal documents required.

Before activation users are required to attend a training webinar.

“JM&A Group leads the industry in Virtual F&I, which is further enabled by Darwin’s suite of products. The potential for time savings and new revenue streams through Virtual F&I is an exciting proposition for our industry as consumer preferences and buying habits shift,” said Scott Gunnell, group vice president of business strategy and operational excellence at JM&A Group.

“Advancements and widespread availability of digital tools like Darwin’s on-demand offering accelerate dealers’ success in the virtual space. By using these tools, dealers can advance their digital retail strategy and provide a consistent experience regardless of how or when your customers prefer to purchase,” Gunnell continued in a news release.

Darwin Automotive chief executive officer Phillip Battista added, “A fully virtual experience is what customers need and want right now and Darwin Documents on Demand is the final application that makes that happen. Even better, we are providing it at no cost as we appreciate the loyalty our customers have shown and want to thank them.

“Dealers just need to complete a short training webinar to ensure the most efficient usage. As COVID-19 is still impacting the market we are continuing to develop applications that enable dealers to profitably service their customers in a contactless way,” Battista went on to say.

Darwin Automotive currently operates in all 50 states with more than 6,300 dealerships subscribed to its programs. Darwin said it delivered 504,000 deals on its platform last month and is on track to deliver 6.5 million units for the year.

For more information, contact [email protected], call (732) 781-9010 or visit https://darwinautomotive.com.

EFG Companies wants dealers to generate up to $200,000 in revenue per year through a new F&I product rolled out this week.

The firm announced the launch of its re-imagined Motorist Assistance Plan (MAP) vehicle service contract. EFG Companies highlighted this newly engineered VSC can provide dealers the potential to increase VSC sales by 15% through 25 million available terms.

EFG Companies contends that traditional VSCs sometimes have a small set of very specific terms that may not fit every customer’s needs, forcing dealers to shoehorn customers into narrow terms with too much or too little coverage. With the enhanced MAP, EFG expanded eligibility requirements and term mileage in 2,500 mileage increments, resulting in 25 million term options dynamically available to the dealer.

Along with five deductible options and six surcharge options, the updated MAP can allow the dealer to better tailor the product to each customer’s personal driving habits, giving them a viable product for every customer and increasing penetration rates.

The company also mentioned canceled contracts and burdensome chargebacks are also reduced for the dealer with the product’s focus on each customer’s specific protection and budget constraints.

A significant benefit to the newly designed MAP is the product’s surgical-level risk-based pricing.

Not only is this more beneficial for all customers, but EFG Companies also said dealers can benefit significantly from greater contract specificity in their reinsurance positions as reserves are better aligned with contract coverage. This situation can creates a much more efficient loss management and rating process, reducing the impact of high-volume claims on dealers’ reinsurance positions.

“Recent events around the COVID-19 pandemic have significantly accelerated the pace of change in the automotive industry, from online vehicle retailing to F&I products that have a higher degree of relevancy to the consumer,” EFG Companies president and chief executive officer John Pappanastos said in a news release.

“The U.S. long-term economic outlook reflects diminished consumer confidence, driving consumers to demand more specific levels of protection that are better aligned with their individual needs and budgets at a more specific level than we’ve ever seen before,” Pappanastos continued. “This product delivers on all fronts for the consumers while meeting dealers’ evolving profitability hurdles.”

EFG Companies pointed out that MAP is designed for new, used and high-mileage vehicles. With four levels of coverage, including exclusionary and named components, MAP eligibility is extended to current plus 12-model-year vehicles with less than or equal to 150,000 miles.

F&I managers can offer MAP based on the individual driving habits of their customers with:

— Expanded eligibility requirements

— Expanded term mileage in 2,500-mile increments

— Six surcharge options that include commercial and ride-sharing vehicles

— Five deductible options to meet every customer’s need at the time of a claim.

For more information, visit this website.

Nicholas Financial found a way to cheer the close of its 2020 fiscal year since it broke a string of two consecutive years of negative earnings.

And the subprime auto-finance company also highlighted how funds from the Paycheck Protection Program generated a positive impact, too.

Nicholas Financial reported that its net income for the fiscal year that ended March 31 totaled $3.5 million as compared to net loss of $3.6 million for the fiscal year that closed on the same date in 2019.

Nicholas Financial said it generated that figure even though annual revenue decreased 12.9% to $62.1 million from the previous fiscal year’s total of $71.3 million.

The finance company ended the fiscal year on the upbeat not since its fourth quarter included net income of $2.3 million as compared to net loss of $4.7 million a year earlier.

“We are very pleased to return to profitability in Fiscal Year 2020, after posting negative earnings in each of the previous two years,” Nicholas Financial president and chief executive officer Doug Marohn said in a news release.

“Although the uncertainty related to the COVID-19 pandemic and its impact on the economy is a very real factor, we believe the pieces are now in place to build upon those modest profits through market scale, new product offerings and other strategic initiatives,” Marohn continued.

In response to the global impacts of COVID-19 on U.S. companies and citizens, the government enacted the CARES Act on March 27. Nicholas Financial said the CARES Act included several tax relief options for companies, which resulted in the following available provisions:

— The company has elected to carryback its 2018 net operating losses of $9.7 million to 2013, thus generating an anticipated refund of $3.4 million and an income tax benefit of $1.3 million. The tax benefit is the result of the federal income tax rate differential between the current statutory rate of 21% and the 35% rate applicable to 2013.

— The company plans to carryback its 2019 net operating losses of $2.9 million to 2014, thus generating an anticipated refund of $1.0 million and an income tax benefit of $0.4 million. The tax benefit is the result of the federal income tax rate differential between the current statutory rate of 21% and the 35% rate applicable to 2014.

— During the quarter ended March 31, the company had significant cash movements of approximately $19.9 million for the bulk portfolio purchases and approximately $7.4 million from the credit facility, which increased outstanding debt. The company did not have any significant capital expenditures.

Beyond those moves, Marohn explained other ways Nicholas Financial is looking to make it through the coronavirus pandemic.

“As we navigate through the market conditions facing us today and impacting both our borrowing customers and our retail dealer partners, we are also focused on maintaining the underwriting and servicing discipline that allowed us to be profitable once again,” Marohn said. “Our four-prong approach to growing our company is more important now than ever.

“We are dedicated to growing market share in our existing markets, we are expanding our direct loan program wherever we have a branch location, we are committed to expanding our branch network in Idaho, Iowa, Nevada, Utah, Wisconsin and other locations, and we remain open to portfolio acquisitions as they present themselves,” he went on to say.

In other matters, Nicholas Financial said that on May 27 the company obtained a loan in the amount of $3,243,900 from Fifth Third Bank in connection with the U.S. Small Business Administration’s Paycheck Protection Program Pursuant to the Paycheck Protection Program, all or a portion of the PPP Loan may be forgiven if the company uses the proceeds of the PPP Loan for its payroll costs and other expenses in accordance with the requirements of the Paycheck Protection Program.

The company said intends to use the proceeds of the PPP loan for payroll costs and other covered expenses and intends to seek full forgiveness of the PPP loan as soon as permitted under the Paycheck Protection Program.

“The company is very fortunate to have the benefit of the Paycheck Protection Program at this critical time,” Marohn added. “With these additional funds, we are able to bring back 100% of our employees who were furloughed in April, release the hiring freeze implemented in March and ensure all of our existing branch offices will remain open and operational for the foreseeable future.”

If the PPP Loan is not fully forgiven, Nicholas Financial acknowledged that it will remain liable for the full and punctual payment of the outstanding principal balance plus accrued and unpaid interest. The PPP Loan accrues interest at a rate per annum equal to 1.00% and an initial payment of accrued and unpaid interest is due on Dec. 27.

The outstanding principal balance plus accrued, and unpaid interest is due on May 27, 2022, according to Nicholas Financial.

“The PPP Loan is unsecured. The PPP Loan may be prepaid at any time prior to maturity with no prepayment penalties. The Promissory Note contains events of default and other provisions customary for a loan of this type,” the company said.

ProGuard Warranty wants their customers to be singing about including a vehicle protection product with their new- or used-car purchase.

ProGuard is collaborating with SiriusXM to offer customers nationwide a three-month SiriusXM subscription, included at no extra cost, with the purchase of any ProGuard protection plan for their vehicle.

The companies highlighted eligible customers with a factory installed SiriusXM radio will receive three months of SiriusXM All Access, SiriusXM’s most extensive package, which enables the listener to hear all that SiriusXM offers both in their vehicle and outside the vehicle with the SiriusXM app.

Customers who already received a trial subscription with their vehicle purchase are not eligible, according to a news release issued on Tuesday.

ProGuard, which sells a wide variety of protection plans and ancillary products through several thousand dealers across the U.S., said it is well positioned to deliver the benefit of SiriusXM to a substantial base of potential customers in the market for a new or pre-owned vehicle.

“ProGuard has exceeded every growth benchmark we’ve ever set and as a company we are constantly looking ahead at what it will take to get to the next level,” ProGuard Warranty president Dominic Limongelli said.

“Further enriching the customer experience is our top priority and by giving our customers access to SiriusXM’s wide-ranging audio entertainment we are adding value to our already superior products,” Limongelli continued. “Teaming up with SiriusXM provides one more way we can differentiate ourselves and better serve our dealer partners.”

SiriusXM vice president of auto remarketing Gail Berger added, “At SiriusXM, we pride ourselves on delivering the best audio entertainment experience available, and as the number of SiriusXM-equipped vehicles in the pre-owned market grows every year, we want to get as many of those pre-owned customers as we can to tune in and experience all that we have to offer.

“Working with ProGuard, a trusted and growing brand, enables us to connect with a large population of buyers through ProGuard’s thousands of independent and franchise dealer partners,” Berger went on to say. “And ProGuard will be able to deliver the added benefit of SiriusXM to eligible customers who buy any of their excellent F&I products.”

Processing total-loss claims triggering GAP coverage can be one of the most complicated tasks in F&I. JM&A Group is trying to reduce some of the stress connected with them.

In order to improve efficiency and fulfill payments in a more timely manner, JM&A Group recently introduced new GAP claims self-service portals serving both consumers and finance companies.

The company highlighted the enhanced portals provide a one-stop shop to file a claim, upload documentation and access real-time status updates.

“Last year alone, JM&A’s Customer Service team answered more than 2.1 million calls and paid out in excess of $525 million in total vehicle service, maintenance and GAP-related claims,” said Sandra Porceng, vice president of customer services at JM&A Group.

“Given our high level of output, we are continually finding ways to streamline our process and improve efficiencies,” Porceng continued in a news release. “We are confident these new self-service portals specifically designed for our GAP claims will do just that, providing support to vehicle owners filing a claim while helping us to strengthen relationships with our lenders.”

Beginning on Monday, JM&A Group indicated consumers and finance companies will use the self-service portals to upload all of their total loss information and documentation directly to JM&A.

In return, JM&A associates will be able to remain in contact, providing status updates on their claim and its payment.

Vehicle owners with a GAP claim can register for the consumer portal at mygapclaim.com to take advantage of these new enhancements.

Leading up to the launch, JM&A mentioned its GAP claims team has been in regular communication with its finance company partners to guide them through the transition, providing step-by-step registration information and virtual guidance as requested to promote early adoption and acclimation.

JM&A added that finance companies that have not registered for the new portal should visit this webpage for a short video overview and to fill out a brief form, providing basic information.