LendingTree recently reported that millennials owe a median of $15,281 in auto debt across the 100 largest metros in the U.S.

Researchers used an anonymized sample of credit reports from the first and second quarters of this from more than 200,000 millennial LendingTree users to calculate their total auto debt obligations.

LendingTree auto finance expert Jenn Jones said millennial auto debt may be this high because …

Read more

Open Lending announced this week it is partnering with one of the nation’s largest credit unions, America First Credit Union (AFCU), which now will offer indirect auto financing services through Open Lending’s Lenders Protection program.

The companies said their alliance can allow dealers to give more opportunities for vehicle deliveries with credit union members who are near- and non-prime or emerging-prime.

“In an auto lending environment with climbing interest rates and persistent car inventory issues, Lenders Protection helps keep car ownership accessible,” said Tom Rice, senior vice president of national sales at Open Lending.

“Our partnership with AFCU will empower the credit union to offer auto loans with longer terms and better rates — and give more members access to financing that works for them in uncertain economic times,” Rice continued in a news release.

America First Credit Union will offer expanded services via Open Lending beginning in the fourth quarter.

“When it comes to first-time car buyers, the ability to offer auto loans with flexible terms helps us meet our members and buyers where they are financially,” AFCU chief lending officer Brett Christensen said in the news release. “As a credit union, we’re always looking for ways to better serve our current and future members’ needs.

“With Open Lending, we’re able to help more people achieve car ownership and build stronger relationships with our members, allowing us to better serve their future needs such as a mortgage, home equity or personal loan down the line,” Christensen went on to say.

To learn more about Open Lending or to schedule a demo, go to this website.

Edmunds said its analysts have adjusted their auto finance data cleaning process to include new and used monthly payments up to $2,000 to account for changes to the market, as previously the limit was up to $1,500.

Based on the third quarter data Edmunds shared on Monday, you can understand why.

Edmunds reported 14.3% of consumers who financed a new-vehicle purchase in Q3 committed to a monthly payment of …

Read more

DDI Technology literally now has more room to maneuver.

This week, the electronic lien and title technology firm and a subsidiary of IAA announced the grand opening of its newly expanded corporate offices in Irmo, S.C.

Now with 35% more office space, DDI highlighted the modern headquarters will accommodate more than 200 people, satisfying the company’s current needs and preparing it for future expansion.

Executives said the expanded DDI facility will support the continued growth of the team and will help retain and attract top employees with innovative enhancements.

DDI noted the workspace includes technology-enabled conference rooms with space to collaborate with customers and partners, better process flow for DDI’s title center operations and expanded capacity for title vaulting.

“We are proud to call Irmo, South Carolina, home, and this significant investment proves our commitment to the area for years to come,” said Tab Edmundson, IAA vice president of client solutions and DDI president.

“We are thrilled to continue contributing to the local business community and economy by creating jobs and giving back. I am excited for the future of DDI,” Edmundson added.

EasyCare wants to help your dealership customers feel more confident about taking delivery of that vehicle that has some of the latest technology available.

On Monday, the APCO Holdings brand introduced TechCare, a new vehicle service contract (VSC) designed exclusively to cover the costly technology, electronic components, and safety systems in vehicles.

The company explained that TechCare can provide vehicle buyers with a lower-cost alternative to a traditional VSC, helping dealerships boost service retention rates while saving customers thousands of dollars in repair bills.

TechCare is the latest addition to EasyCare’s comprehensive suite of F&I products designed to give dealers the opportunity to maximize every sale, driving greater revenue for the dealership and a better experience for customers.

“Today’s vehicles are loaded with high-tech options to the point where they are essentially computers on wheels. TechCare protects car buyers in the event that these systems and components fail or are damaged,” APCO Holdings chief executive officer Scot Eisenfelder said in a news release.

“Consumers purchase similar protection plans for other products they rely on as part of their daily lives, such as smartphones and computers. This type of protection for technology in vehicles should be a familiar concept for consumers,” Eisenfelder continued.

TechCare coverage includes protection for in-vehicle technology such as:

—Touchscreens, cameras, infotainment systems and speakers

—Electronics such as navigation/GPS systems

—TV screens, DVD players, WiFi and USB ports

—Safety systems such as blind spot detection, lane departure warning, parking sensors and autonomous braking systems.

TechCare coverage begins after the manufacturer’s warranty expires and can be extended up to seven years, according to the news release.

EasyCare estimated that replacement and repair costs for vehicle technology can easily run into thousands of dollars. The average replacement cost for a navigation display unit alone can run over $2,000. Replacing a digital multimedia receiver can add up to $2,428. TechCare covers these kinds of repairs so consumers don't have to worry about an unexpected repair bill.

In addition to coverage for technology, electronics and safety systems, TechCare comes with:

—24/7 emergency roadside assistance and towing

—Substitute transportation (rideshare vehicles and taxis) reimbursement

—Trip interruption reimbursement

—A diminishing deductible option to help dealers with service retention (if a customer returns to any store in the selling dealer’s group the deductible is lower or $0)

TechCare can be sold with any vehicle eligible for coverage, including electric vehicles (EVs). It provides dealerships with another opportunity to sell a VSC product to customers who do not choose to purchase a traditional VSC.

The company went on to mention TechCare is accepted at any dealership or ASE Certified repair facility in the U.S. and Canada, and all repairs are made by certified technicians. TechCare is also 100% transferable to a vehicle’s new owner in the event of a sale.

For more information, visit https://easycare.com.

Today’s automotive industry continues to see noticeable changes in everything from consumer demand, behavior, and shopping patterns to the way operations are dealing with an ongoing shortage of inventory, parts, and labor. What’s more, the shopping process itself continues to evolve into more of a digitized experience. While the industry isn’t fully digitized the way we consume virtually everything else, we’re light years ahead of where we were back in 2015.

F&I product providers overall remain confident with their ability to manage through the increased parts and labor costs with specific product pricing increases. In fact, the price of replacement parts and the labor needed to install them rose last year and continues to list above 2021 levels, partly due to inflation. However, F&I providers continue to manage these increases along with their dealer partners.

F&I profits remain healthy

These costs are important to note because F&I sales continue to be an important profit center for the industry as a whole. Some of the largest auto retailers reported an increase of year-over-year F&I profits as high as 66% during Q4 of 2021. Also, depending on the type of participation program they’re involved in, their program can also dictate the level of profit dealers are realizing.

Aside from prices, the shopping experience itself is changing before our eyes, with the continued proliferation of digital retailing and a more digitized F&I process. Dealers have increasingly embraced digital-retail processes over the past few years, which benefits their finance departments by injecting more efficiency into the process – something consumers have long desired.

This is good news since consumers already are extremely accustomed to acquiring products digitally via popular e-commerce platforms. A plethora of training programs are now available to help dealers and their F&I departments get up to speed in how they offer F&I products and services in an online environment.

Continued focus on the customer experience

This is critically important since it provides car shoppers with education on F&I options earlier in the process, helping them make more informed decision from the comfort of their own home. It also leads to a customer experience that exceeds their expectations, which may even lead to greater long-term loyalty and engagement. Ultimately, a more digitized F&I process gives consumers transparency, convenience and speed — everything a dealer needs in order to sell a car and F&I benefits in a more expeditious manner.

Over the last year, more dealers are selling F&I products such as vehicle service contracts, appearance products, tire and wheel protection, prepaid maintenance and GAP coverage. In fact, the majority of dealers say their F&I sales are up between 5% and 10% compared to the previous year, according to a recent retailer survey of F&I trends2.

Key trends among specific F&I products

Most dealers today are selling F&I products such as tire and wheel (73%), exterior appearance products (72%), GAP coverage (68%), and vehicle service contracts (66%). Dealers say there are a handful of ways they can sell even more F&I products, including the ability to provide access to online financing (56%), offering F&I products that help with vehicle affordability (53%), and F&I products that are more geared toward the sale of used vehicles (48%).

In terms of selling more F&I products during online shopping, 54% of dealers say they still need better resources that offer pricing online, and 53% of dealers say they need resources that offer the ability for customers to select F&I product and coverage options online.

The majority of dealers say access to more F&I products designed specifically for used vehicles would be the most impactful overall to improving F&I product sales, as well as increased coverage for existing protection products like VSCs, and a more diverse set of F&I product options.

In terms of greatest opportunities for selling more F&I products today compared to a year ago, most dealers (55%) said more EV/plugin sales gives them the best chance. This correlates to the most frequent reasons cited by consumers for selecting F&I products – more technology features found in cars today and electrical components.

Each of these trends illustrate continue strong growth for F&I product potential and sales for today’s auto retailers of all sizes and focus of new/used.

Travis Wools is vice president of marketing and communications at Protective Asset Protection.

Auto repossessions are on the rise. Subprime repos are up 11% since 2020, according to Jalopnik. Even among prime borrowers with excellent credit scores, repossession rates have doubled from 2% to 4% in the past two years, according to Barron’s.

This trend is not surprising, considering how expensive vehicles have become. The average price for a new car is now more than $47,000 and the average used car price is over $32,000, according to Kelley Blue Book. More than 12% of customers who purchased a new vehicle in the last two years have payments of over $1,000 per month, according to Edmunds.

If the U.S. enters a recession within the next year, it’s likely that repossession rates will accelerate. Remember the subprime mortgage crisis, when millions of homeowners found themselves in a position of negative equity? Over six million homeowners lost their homes to foreclosure, many of whom chose to walk away in a strategic default.

Unfortunately, there is potential for this scenario to play out in the auto industry. For nearly two years, car buyers have been paying thousands of dollars over MSRP for new vehicles, and thousands of dollars above typical used vehicle valuations. If someone pays $15,000 over sticker for a vehicle, and within a year the value of that vehicle drops to $5,000 below MSRP, it’s going to be a long time before that person is right side up in their loan. And car loans are much easier to walk away from than home loans.

For lenders, this creates a huge problem. I spoke to one lender recently who said that although they are able to recover 98% of vehicles, the average loan value they are able to recover on those vehicles is 60%.

This could be a crisis-in-waiting for lenders with large portfolios of auto loans.

Crypto as collateral

One way to prevent strategic defaults on auto loans is to demand larger down payments. However, cash-strapped consumers either can’t, or won’t, put more money down. Tapping into retirement accounts is not a realistic option, as pulling out cash for an auto loan would result in early withdrawal penalties.

But what about cryptocurrency? Approximately 145 million American adults, or about 56% of the population, own some form of cryptocurrency, according to a recent Motley Fool survey; and another 46.5 million Americans say they are likely to invest in cryptocurrency for the first time in 2023.

Additionally, 80 percent of cryptocurrency owners are long-term holders, according to Glassnode. This means that a sizeable percentage of car buyers may be cash strapped, but with thousands of dollars of cryptocurrency stashed away on an exchange or in a digital wallet.

For lenders, the benefits of offering crypto-collateralized loans are two-fold. If the consumer defaults, the lender can still repossess the vehicle as they normally would. In addition, the lender can tap into some or all of the cryptocurrency that is being held as collateral, in order to cover the outstanding loan value.

If the economy continues to tighten, fewer car buyers will be able to qualify for auto loans. In particular, millennial and Gen Z consumers tend to have thin credit profiles. Another benefit to lenders is the ability to approve more loans for car shoppers who are willing to use crypto as collateral.

Lenders faced with rising default rates might want to consider tightening lending policies now. In addition, find a third-party partner who can set up and facilitate the ability to offer crypto-collateralized loans to consumers. These types of loans are a win-win-win for lenders, auto dealerships and consumers alike.

Fred Brothers is president and co-founder of Cion Digital, developers of a crypto payment and marketplace lending platform connecting consumers, merchants and lenders with new payment and loan options. Prior to co-founding Cion Digital, Brothers served as the executive vice president and chief innovation officer at FIS, a Fortune 500 provider of financial technology.

Experian senior director of automotive financial solutions Melinda Zabritski shared more time for the Auto Remarketing Podcast to discuss which auto finance metrics landed within expectations for the second quarter and which ones did not.

Zabritski also touched on how finance companies are keeping risk under control amid high vehicle prices.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

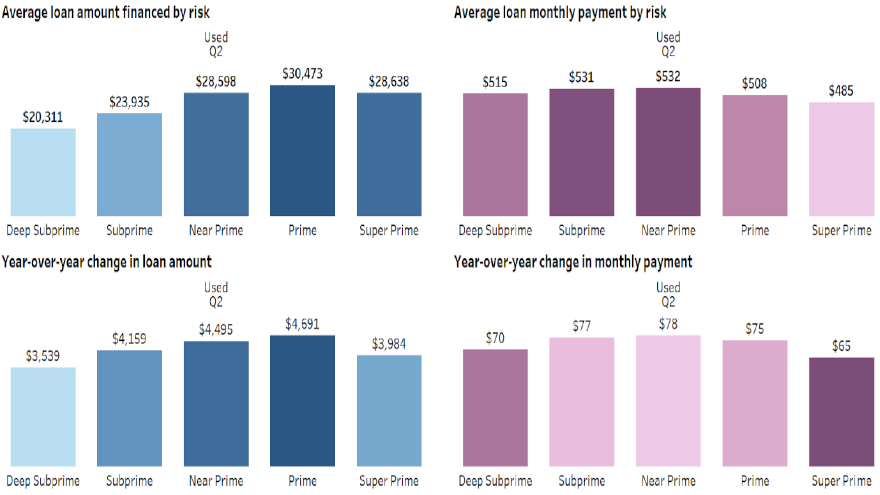

The newest auto finance data from Experian reinforced the theory that consumers are taking delivery of used vehicles more often because of necessity.

As the automotive market continues to face inventory shortages, analysts said consumers are shifting back to the used-vehicle market. According to Experian’s State of the Automotive Finance Market Report: Q2 2022 released on Thursday, 61.78% of …

Read more

Credit Acceptance said late on Monday that founder Don Foss passed away on Sunday from complications arising from an aggressive form of cancer. He was surrounded by his family, according to the company announcement.

Specializing in subprime auto financing, Credit Acceptance was incorporated in 1972, as Foss served as chief executive officer until 2002, followed by chairman of the board until his retirement in 2017.

Throughout his legendary career in the automotive industry, Foss was recognized with many awards, including:

—Innovative CEO in the Top Small Companies in America issue of Forbes. (1996)

—Lifetime Achievement Award from the Metro Detroit Chapter of the Michigan NIADA for his contributions to the automobile industry through Credit Acceptance and his personal philanthropy. (2003)

—Special Finance Hall of Fame Award from Special Finance Insider Magazine. (2008)

—Entrepreneur Shares Global 400 leadership award. (2010)

—Northwood University presented him with a Doctor of Laws, Honoris Causa, degree. (2010)

—NABD Hall of Fame Award. (2015)

When he was inducted by the National Alliance of Buy-Here, Pay-Here Dealers, Foss recapped the start of his time in the automobile industry, which spanned 55 years, beginning in 1967 when he opened his first car lot in Detroit and began selling primarily to customers who did not qualify for traditional financing.

When Foss opened his own retail operation, it was dirt lot he rented for $35 a month.

“Like most of you who worked in a family business, I worked after school and during the summers,” Foss said during his acceptance speech after receiving his Hall of Fame induction.

“My dad was my mentor,” Foss said. “He taught me a great lesson early on. You can’t sell anything by saying no.”

Foss evidently didn’t say no to customers too often. That single dirt-lot operation grew into 17 locations. Foss also harkened back to his father’s advice to formulate what’s now Credit Acceptance.

“My wife would like nothing better than for me to kick back and take it easy, just live off the fruits of my labor. But I still like the car business. I still have fun selling cars,” Foss said during that 2015 speech.

“I humbly accept this award,” he continued. “I think about all of the wonderful people I’ve worked with over the years who have helped me through my career. But I don’t want you guys to think I’m done. I’d like to think I’m just getting started.”

In July, Credit Acceptance celebrated its 50th anniversary with Foss being part of the festivities.

“Five decades ago, our founder, Don Foss, came up with an innovative way to offer auto financing to enable dealers to sell cars to more people,” the company said in a LinkedIn post commemorating the milestone. “And now, individuals with no credit or bad credit are able to rebuild their credit by making on-time car payments and putting themselves on the road to a better financial future.

“Since our founding, we’ve served millions of consumers, thousands of dealers and over 2100 team members delivering on the mission to change lives,” the company continued.

Credit Acceptance went on to highlight in Monday’s announcement that not only was Foss known for his incredible business insight and perseverance, but he also lived the company’s “We Change Lives” purpose in his community.

The Don Foss Annual Scholarship (created in 1998) and the Don Foss Endowed Scholarship (created in 2015) together have awarded more than 630 scholarships to students pursuing careers in the automotive industry at Northwood University. And in 2016, he established a private fund, Car Dealers Care National Foundation, which gives back to the community both through his personal philanthropy and through CARite, a chain of dealerships he founded in 2011.

“Don has left behind a lifetime of hard work, which turned Credit Acceptance into one of the largest auto finance companies in the country. He was truly an American Entrepreneurial Icon, and his story epitomizes the great American dream. Don’s death is a great loss, and he will be missed by many,” the company said.

“Our deepest condolences to the Foss family and everyone who knew Don,” the company went on to say.