As the Consumer Financial Protection Bureau takes a closer look at alternative data, the American Bankers Association delivered an eight-page comment letter containing a half dozen suggestions about the current and potential use of alternative data and modeling techniques in the credit process.

Along with the suggestions, ABA also raised regulatory concerns, especially when using alternative data might trigger the CFPB to take action for what the bureau could allege as unfair, deceptive, and abusive acts and practices (UDAAP).

Authoring the material was Nessa Feddis, the association’s senior vice president and deputy chief counsel for consumer protection and payments. Feddis began by outlining a foundation of ABA’s stance regarding alternative data.

“As a general matter, banks support the use of alternative data sources to evaluate credit applicants, particularly people with no or ‘thin’ credit files who may be eligible for credit,” Feddis wrote. “The use of alternative data, coupled with mobile channels of access to bank products and services, may have potential to expand financial services and open the door to people who otherwise have limited or no access to mainstream credit.

“However, banks have concerns about the reliability and predictability of some alternative data and about consumer protections promoting privacy and data security,” she continued. "In addition, it should also be emphasized that banks recognize the importance of fair lending and demonstrating that underwriting models are sound.”

Feddis then went into six suggestions that could quell concerns about UDAAP allegations among other aspects of leveraging this technology. The recommendations included:

1. Alternative data providers should be sensitive to consumer privacy and data security and ensure that data are accurate and reliable.

2. Regulators must recognize that application of disparate impact liability in supervision and enforcement causes banks to retreat from using alternative data, limiting inclusion and competition.

3. To promote the use of alternative data in mortgage lending credit decisions, regulators should provide guidance on how banks can test and demonstrate that models comply with the Fair Housing Act’s disparate impact liability, consistent with the Supreme Court’s Inclusive Communities framework, and also meet supervisory safety and soundness expectations about model validation.

4. Regulators must also recognize that the persistent threat of an undefined UDAAP sanction hovers like a dark cloud over financial innovation and will cause banks to retreat from using alternative data.

5. A supervisory approach that reduces banks’ compliance risk will encourage banks to use alternative data as a tool to develop products, especially small dollar loans, designed for people who may not qualify under traditional underwriting standards.

6. The bureau should reconsider its Project Catalyst and No Action Letter policy to promote testing of alternative data and foster innovation without the risk of triggering fair lending and UDAAP liability.

“Banks are enthusiastic, but cautious, about using alternative data and models to innovate and improve customer access to credit and product affordability,” Feddis wrote to close her letter to the CFPB.

“A number of factors impede experimentation and use of alternative data,” she continued. “Fair lending, UDAAP, and model validation challenges, risks and costs are primary obstacles. Lack of assurance about the predictability, reliability and accuracy of the data as well as privacy and data security concerns also cause banks to hesitate.

“Simply put, the compliance and reputation costs and risks can overwhelm the uncertain return,” Feddis went on to say in the letter available here.

While plenty of attention went toward the U.S. House voting major changes involving healthcare last week, the House Financial Services Committee passed the Financial CHOICE Act 2.0 — the measure that would greatly modify the Dodd-Frank Act and the Consumer Financial Protection Bureau.

The committee passed the proposal along party lines by a 34-26 vote with all Democratic lawmakers opposing and all Republican members supporting the plan crafted by chairman Jeb Hensarling, who wants to make a wide array of changes, including:

—Allowing the sole director to be removed at will by the president

—Removing the bureau’s supervisory authority

—Limiting the CFPB’s enforcement authority to enumerated statutes

—Removing its unfair, deceptive, and abusive acts or practices (UDAAP) authority

—Repealing mandatory advisory boards and market monitoring authority.

“The American Financial Services Association (AFSA) fully supports this legislation crafted by the House Financial Services Committee under the leadership of chairman Jeb Hensarling,” said a spokesman for AFSA in a message to SubPrime Auto Finance News. “AFSA believes the CFPB’s current approach to oversight of the vehicle finance industry amounts to regulation by enforcement.”

The Financial Services Roundtable (FSR) also gave a succinct, positive reaction to the committee’s actions, calling it an important first step to improving the regulatory system and promoting economic growth. FSR chief executive officer Tim Pawlenty signaled support for many of the provisions in the proposal.

“Improvements to financial regulations can lead to economic growth, while still protecting taxpayers and consumers,” Pawlenty said. “We thank the Committee for its leadership in driving the regulatory reform debate forward and look forward to working with policymakers to craft a regulatory reform system that unlocks more economic opportunity for all Americans.”

Consumer Bankers Association (CBA) president and chief executive officer Richard Hunt cheered the passage, as well, but Hunt still has some reservation about what the Financial CHOICE Act 2.0 contains.

“Since Dodd-Frank’s passage, banks have been working diligently to comply with the sometimes onerous and duplicative requests of regulators,” Hunt said. “We are encouraged by chairman Hensarling’s commitment to meaningful and targeted changes to Dodd-Frank, and welcome many of the Financial CHOICE Act’s provisions which provide regulatory relief for both banks and consumers, such as the repeal of the Durbin Amendment. With almost no debate prior to passage, the Durbin Amendment imposed price controls on debit interchange fees while promising lower prices for consumers — but the savings never came.

“In addition, CBA appreciates many of the committee’s reforms to the CFPB,” Hunt continued. “However, we continue to believe consumers would be best served by establishing a five-person, bipartisan commission at the bureau. In order to achieve long-term economic stability and sustain consumer confidence, the CFPB must be governed by a diverse group of policymakers and industry experts who understand the everyday needs of American families and small businesses.”

Both Democrats on the committee and other consumer advocates criticized Hensarling and this proposal, often interjecting the moniker “wrong choice” within the reactions.

Committee Democrats mentioned 13 amendments to the Financial CHOICE Act 2.0, adding that “Republicans ultimately rejected all Democratic amendments proposed.” How the matter unfolded upset the likes of Liz Ryan Murray, policy director of People’s Action Institute.

“The wrong CHOICE Act would cripple the CFPB’s ability to protect us — the American people. Big banks and loan sharks brought our economy to the brink of collapse in 2008. We refuse to let Rep. Hensarling and the GOP eliminate the protections we’ve won. The wrong CHOICE Act destroys the CFPB’s independence and ties its hands,” Ryan Murray said.

“Congress must immediately reject this Wall Street wish list. They are supposed to serve the people, not corporate profits,” she went on to say.

It’s been a little while since I’ve made an entry into my diary about navigating through the rigors of the National Automotive Finance Association’s Consumer Credit Compliance Certification Program.

I’m happy to report I can see the certification summit. While I didn’t get here with climbing boots and a backpack, it’s been just as rewarding as any journey a hiker, biker or just a strolling walker could make.

And now the NAF Association is widening the opportunity for you to make the same satisfying and worthwhile journey.

Because the NAF Association obtained so many requests, the organization announced this week that participants in its popular Consumer Credit Compliance Certification Program now can complete the opening of the four modules online.

Previously, the only way to begin the program was to attend a two-day classroom session, which was scheduled twice per year.

I participated in the opening session the NAF Association hosted last September here in the Dallas-Fort Worth area, which rivals Detroit or anywhere else in the country as far as automotive penetration. As many of you are aware, large finance companies such as General Motors Financial, Santander Consumer USA, Capital One Auto Finance and Exeter Finance all call this area home.

Furthermore, each of the Uber drivers who took me to the headquarters of Digital Recognition Network (DRN) and EFG Companies on Tuesday mentioned how much the area is being impacted by the construction of Toyota’s sprawling headquarters here in Plano.

By the way, listen up for future installments of the Auto Remarketing Podcast to hear the conversations I had with top executives and DRN and EFG.

If you still want to begin the Consumer Credit Compliance Certification Program with in-person training, the NAF Association indicated classroom sessions will continue to be offered and candidates who elect to begin the program online are welcome to attend the classroom session, too, but will not be required to do so.

The in-person training is simply superb. Hudson Cook partners Patty Covington and Eric Johnson explain the regulatory material without sounding like Charlie Brown’s teacher from the Peanuts cartoons.

Module 2 and Module 3 will continue to be offered online as they have since the program’s inception.

Once a participant passes the requirements of a module segment, the next portion becomes available. And participants must score 80 percent or higher on a segment exam.

(Imagine if all of the people and providers you depend on had to produce at least at an 80-percent clip or higher?)

Having to achieve that level of success absorbed numerous of my Saturdays since September.

But it’s been so worth the effort. The program not only gives you a comprehensive and digestible explanation of important federal mandates for auto financing, it also provides important foundational knowledge about state regulations that sometimes can vary as much as the color of vehicles in your inventory or portfolio.

The NAF Association indicated more than 500 compliance professionals have completed the program. By the end of the month, I hope to be a part of an increase in that tally after taking in Module 4 with Patty and Eric this week and completing one more exam.

While I might not be in the trenches of a finance company's underwriting or collections department, I like to think of all of us at Cherokee Media Group that generate Auto Remarketing, SubPrime Auto Finance News, Auto Remarketing Canada and BHPH Report, as well as the conferences at Used Car Week, as one of your service providers; a company that offers an important resource — knowledge.

And with the Consumer Credit Compliance Certification soon to be in my knowledge quiver, it’s my intention for it to reflect in the caliber of content you see from us here at Cherokee Media Group, recapping not only the moves regulators are making but also discussing how they might impact your business.

Before closing, I want to express again my sincere appreciation to Jack Tracey, Cindy Sly and the team at the NAF Association as well as Patty and Eric and the Hudson Cook stable of legal experts for allowing me to participate in the training.

Jack could have quickly brushed me aside and said, “No way!” But as always, he and everyone else involved all have been gracious.

More information about the Consumer Credit Compliance Certification Program can be found at www.nafassociation.com or by contacting Cindy Sly at [email protected].

So if you or your company has been considering this program, I wholeheartedly recommend it. Not only will your firm be better for it, so will the entire auto finance industry.

Nick Zulovich is senior editor of SubPrime Auto Finance News and BHPH Report and can be reached at [email protected].

The Consumer Financial Protection Bureau said on Wednesday that Security National Automotive Acceptance Company (SNAAC) violated a consent order from 2015, demanding that the finance company make good on the redress it owes to consumers and pay an additional $1.25 million penalty.

The CFPB initially ordered SNAAC, which specializes in working with servicemembers, to pay both redress and a civil penalty for illegal debt collection tactics, including making threats to contact servicemembers’ commanding officers about debts and exaggerating the consequences of not paying. The bureau determined SNAAC violated the 2015 order by failing to provide more than $1 million in refunds and credits, affecting more than 1,000 consumers.

“This company violated a bureau order when it failed to get money back to servicemembers it had hounded with illegal debt collection tactics,” CFPB Director Richard Cordray said. “We are making sure this company finally rights its wrongs.”

SNAAC, based in Mason, Ohio, is an auto finance company that operates in more than two dozen states and specializes in loans to servicemembers, primarily to buy used vehicles.

The company shared a statement with SubPrime Auto Finance News, stating that “the settlement resolves a disagreement between SNAAC and the CFPB over the interpretation of part of a consent order.”

The company continued, “SNAAC agreed to this settlement to close this matter and move forward in serving customers in the respectful, honorable manner that has been the company’s tradition.”

SNAAC pointed out that the CFPB acknowledges in the settlement agreement that “SNAAC has consented” to the order “without admitting” to its findings. The original consent order covered approximately 2,200 of the more than 83,000 accounts serviced by SNAAC between 2011 and 2015.

“At issue in this disagreement was the application of credits provided to a fraction of those accounts that had already benefited from a settlement balance for substantially less than was owed,” SNAAC said.

“Although SNAAC disagreed with the CFPB’s interpretation of the 2015 consent order, the company offered to pay all the disputed amounts in order to move forward,” the company continued. “The CFPB declined the offer and began an inquiry.

“SNAAC fully cooperated and responded quickly to all requests for data, reports and testimony,” the company went on to say. “SNAAC is proud of its work over the past 30 years for its customers, many of whom would not have had access to the credit they and their families need.”

Back in June 2015, the CFPB sued SNAAC for aggressive collection tactics against consumers who fell behind on their vehicle installment contracts. If servicemembers lagged behind on payments, the bureau said SNAAC’s collectors would threaten to contact — and in many cases did contact — their chain of command about their debts.

Also, the bureau said the company exaggerated the consequences of not paying. For instance, the regulator indicated SNAAC representatives told some consumers that failure to pay could result in action under the Uniform Code of Military Justice, demotion, discharge, or loss of security clearance. But these consequences were extremely unlikely.

The CFPB alleged that SNAAC’s aggressive tactics, which took advantage of servicemembers’ special obligations to remain current on debts, victimized thousands of borrowers.

Then in October of that year, a CFPB consent order indicated that SNAAC engaged in “unfair, deceptive, and abusive acts and practices” while collecting on these vehicle installment contracts. The order required SNAAC to pay $2.275 million in consumer redress through credits and refunds, and a $1 million civil penalty.

Consumers with an account balance were to receive credits to their accounts, and consumers with a zero balance were to receive cash refunds. While SNAAC submitted two plans that claimed to provide the full amount of redress ordered, the bureau insisted both were designed to underpay such redress.

Acting on a tip from a servicemember’s father, the CFPB discovered that SNAAC had issued worthless “credits” to hundreds of consumers and failed to provide proper redress to many more.

The CFPB reiterated that it is issued this new consent order against SNAAC for violating the terms of the 2015 consent order by failing to properly give refunds or credits to affected borrowers. In this latest development, the CFPB found that the company had failed to meet its obligation to pay redress to consumers by:

— Issuing worthless “credits” to settled-in-full accounts: In purporting to provide redress, the CFPB said SNAAC treated accounts that were settled-in-full as having a positive account balance. Instead of providing refunds to consumers with settled-in-full accounts, the bureau said SNAAC issued worthless account “credits.” Those consumers received no benefit from such a “credit” because they no longer owed SNAAC money and could not use such a credit toward any new or existing loan.

— Issuing worthless “credits” to discharged accounts: The CFPB indicated SNAAC also issued worthless account “credits” to consumers whose debts had been discharged in bankruptcy, and who no longer owed SNAAC money on their vehicle installment contract. The bureau asserted that SNAAC had no legal claim to any unpaid balance, and these consumers received no benefit from the “credits.” SNAAC had, in fact, already stopped collections on these accounts, according to the regulator.

— Failing to properly give redress to consumers making payments under settlement agreements: Some SNAAC consumers were making payments under settlement agreements, the CFPB said. But the bureau noted SNAAC based redress on the original, higher account balance in place before it agreed on a settlement with the borrower. As a result, in many instances, the CFPB said SNAAC issued credits that exceeded consumers’ settlement balances, rather than refund any amount above what the consumers actually owed. And because their settlement balances were improperly credited, some consumers unwittingly overpaid SNAAC to settle their accounts, according to the bureau.

More details of enforcement action

Under the Dodd-Frank Act, the CFPB is authorized to take action against institutions engaged in unfair, deceptive, or abusive acts or practices, or that otherwise violate federal consumer financial laws. Under this consent order:

— SNAAC must pay redress as promised to affected consumers: SNAAC must pay the bureau roughly $720,000, which the bureau will send as refunds to about 925 consumers. SNAAC must issue about $370,000 in new credits to over 1,000 consumers with remaining account balances as well as properly credit roughly 1,000 consumers making payments under settlement agreements. SNAAC must also pay $75,000 to the bureau to cover the costs of distributing these payments.

— SNAAC must pay a $1.25 million penalty: SNAAC must pay a penalty of $1.25 million to the CFPB Civil Penalty Fund, in addition to the $1 million penalty it paid under the 2015 consent order.

The text of the consent order can be found here.

The National Automotive Finance Association is organizing the 21st annual Non-Prime Auto Financing Conference with the same mandate organization leadership has held for more than two decades.

“This is the industry event where all the non-prime auto financing company executives gather for information on the most relevant issues affecting non-prime financing, where vendors servicing the industry gather and where 21 years of networking continues,” NAF Association executive director Jack Tracey said in a message to SubPrime Auto Finance News.

“It’s exciting to see how this conference over the past 21 years has grown in prominence,” Tracey continued. “It’s where everyone comes. Nonprime auto financing leaders attend the conference because they know they’ll see the rest of the industry there.

“We strive each year to pull together a conference program that addresses issues facing nonprime auto industry and to provide education and solutions on the problems confronting the industry,” he went on to say. “Our objective is to have everyone go home with a least one good idea for improving their business.”

This year’s event, which carries the theme, “Optimizing NonPrime Performance,” is scheduled to run from May 31 through June 2. The event again is to unfold in Plano, Texas, but at a new facility — the Hilton Dallas/Plano Granite Park.

Some of the conference sessions includes the release of the 2017 Non-Prime Auto Financing Survey as well as a discussion about how finance companies can raise capital. Another segment has the title, “CFPB in Their Own Words.”

Among some of the notable conference speakers scheduled to appear are:

■ Rep. Jeb Hensarling, a Texas Republican and chairman of U.S. House Financial Services Committee

■ Tom Webb, retiring chief economist at Cox Automotive

■ Amy Martin, senior director of the structured finance ratings group at Standard & Poor’s

Complete registration details for the 21st annual Non-Prime Auto Financing Conference can be found at www.nafassociation.com.

Last summer, Rep. Jeb Hensarling, the Texas Republican who also is the U.S. House Financial Services Committee chairman, introduced a plan he described as a way to replace the Dodd-Frank Act and promote economic growth.

This spring, the outspoken critic of the Consumer Financial Protection Bureau is circulating an update to his proposal, which includes renaming the bureau as the Consumer Financial Opportunity Agency.

Among the eight pages of modifications now being dubbed the Financial CHOICE Act 2.0, the American Financial Services Association highlighted some of the most noteworthy, including:

—Allowing the sole director to be removed at will by the president

—Removing the bureau’s supervisory authority

—Limiting the CFPB’s enforcement authority to enumerated statutes

—Removing its unfair, deceptive, and abusive acts or practices (UDAAP) authority

—Repealing mandatory advisory boards and market monitoring authority.

In its latest update via Newsbriefs, AFSA not only shared a copy of these proposed plan changes, the organization noted that Hensarling’s outline also mentioned how the president could appoint and remove the deputy director of this new agency while establishing what the Financial Services Committee chair called an Office of Economics to review rulemaking and enforcement.

Hensarling is also looking for the prohibition of the consumer complaint database from being published and reforming joint investigations and enforcement actions, according to the document available here.

As likely expected, the ranking member of the Financial Services Committee staunchly pushed back against Hensarling’s latest proposal. Rep. Maxine Waters, a California Democrat, outlined 11 different qualms she had with the Financial CHOICE Act 2.0, including repeal of the Volcker Rule, among other objections.

“The so-called Financial Choice Act is a piece of legislation that will essentially kill the most important aspects of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was designed to prevent another financial crisis. Republicans and Donald Trump have once again prioritized the needs of Wall Street over the needs of hard-working Americans, with a proposal that would take away much-needed protections and put our economic security at risk,” Waters said.

“Simply put, the Wrong Choice Act bows down shamefully to Wall Street’s worst impulses, and would lead us back down the road to economic catastrophe,” she continued.

“The new version, which is even worse than chairman Hensarling’s first draft, cannot be allowed to become law. There is too much at stake for consumers and for our economy at large,” Waters went on to say.

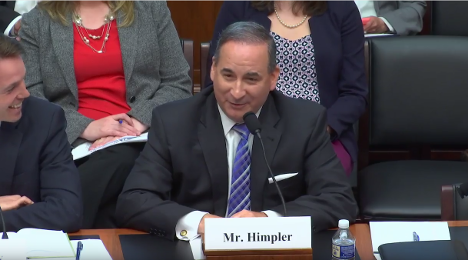

While a former Department of the Treasury official insisted the Dodd-Frank Act resulted in an economy “far stronger and more resilient today than it was preceding the crisis,” American Financial Services Association executive vice president Bill Himpler addressed the Consumer Financial Protection Bureau’s regulatory overreach of the state-regulated consumer credit industry and the need for Congress to reform the bureau’s practices, approve its budget and amend its structure.

The points of view came a day after the CFPB’s semiannual visit to the U.S. House, as Himpler joined three other experts in testifying to the House Financial Services subcommittee on Financial Institutions and Consumer Credit in a session entitled, “Examination of the Federal Financial Regulatory System and Opportunities for Reform.”

In a memo leading up to hearing, the subcommittee indicated providers of financial services are generally subject to a variety of regulatory and supervisory requirements. This hearing was geared to examine the impact the rules and processes from federal financial agencies, specifically the Federal Reserve, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the Consumer Financial Protection Bureau and the National Credit Union Administration, have had on financial companies and their customers.

Lawmakers noted the hearing was also set to examine opportunities for reform of these federal financial agencies, with the aim of improving transparency, accountability and due process for regulated persons and entities and their customers.

The hearing took place last week, a day after CFPB director Richard Cordray delivered his semi-annual report to the full House Financial Services Committee and sparred back and forth with lawmakers, especially from the GOP. AFSA pointed out that Himpler’s testimony and responses filled in critical context about the difficulty financial services providers are facing complying with the unbalanced regulations and enforcement actions put forth by the CFPB.

Himpler noted that while many are focused on financial institutions being too big to fail, AFSA is concerned about those that are “too small to succeed” under the weight of CFPB overregulation.

“AFSA strongly believes that credit should be available to everyone who can manage it, not just to the wealthy or those with perfect credit scores,” Himpler said in written testimony. “It is not apparent that the CFPB shares this philosophy. The CFPB seems to believe that credit should only be extended to those borrowers who do not present any risk.”

The committee addressed a variety of issues with regard to the CFPB, including the bureau’s faulty use of disparate impact theory in vehicle finance, issues with the construction and use of the consumer complaint database and a general lack of balance between consumer protection and credit availability.

“We believe in the CFPB’s mission to protect consumers, but that has to be balanced with ensuring the availability of credit and all too often … it seems that the bureau does not have that balance in mind,” Himpler said in response to questions from the committee.

In prepared testimony, Amias Moore Gerety, former acting assistant secretary for financial institutions at the Treasury Department, applauded the ramifications of the Dodd-Frank Act, the law that led to the creation of the CFPB.

“A broad, diverse and dynamic financial system is a benefit to the U.S. economy and to our citizens. But this strength can only be realized on the foundation of clear rules, appropriate oversight, and independent expertise. Here in Washington, the pain of the financial crisis may be receding from memory, but throughout the country the cost of lost jobs, lost homes and the immeasurable cost of lost opportunities persist. This cost, above all, to the United States, our citizens and taxpayers, must be the central consideration when evaluating changes to our regulatory system,” Gerety said in his prepared testimony.

“In writing the Dodd-Frank Act, Congress sought to make our financial regulations both more protective and more responsive to changes in our economy and in finance. Since the passage of Dodd-Frank, the regulatory agencies and their staff have demonstrated immense capacity to listen to the concerns of industry, advocates and citizens — both to design and revise regulations and guidance that increase the stability and the fairness of our economy,” he continued.

“The result is that our financial firms, our financial system, and most importantly, our economy, is far stronger and more resilient today than it was preceding the crisis. Investors and counterparties have more faith in their financial transactions and investments, and the U.S. has continued to distinguish itself as the safest and most dynamic place to invest capital in the world,” Gerety went on to say.

The entire subcommittee hearing can be viewed here or through the window at the top of this page.

The semiannual testimonial tussle on Wednesday between Consumer Financial Protection Bureau’s Richard Cordray and members of the U.S. House Financial Services Committee spanned more than four hours as the regulator’s director traded arguments back and forth about the agency’s activities and more.

Chairman Jeb Hensarling didn’t hesitate to set the tone for the day during his opening statement, which included the Texas Republican saying, “For conducting unlawful activities, abusing his authority and denying market participants due process, Richard Cordray should be dismissed by our president.

“Not only must Mr. Cordray go, but this current CFPB must go as well,” Hensarling continued. “American consumers need competitive markets and a ‘cop on the beat’ to protect them from fraud and deception. They don’t need Washington elites trampling on their freedom of choice and picking their financial products for them.

“Today, Mr. Cordray and his CFPB don’t just act as a cop on the beat, they act as legislator, prosecutor, judge and jury all rolled into one,” Hensarling went on to say. “The CFPB represents the summit of unelected, unaccountable and unconstitutional agency government. It represents a dagger aimed at the heart of our foundational principles, namely co-equal branches of government, checks and balances, due process and justice for all.

“Clearly you can be a Democrat — upper case D — and believe in the CFPB, but you cannot be a democrat — lower case D — and believe in this institution,” he added.

Rep. Maxine Waters, a Democrat from California and ranking member of the Financial Services Committee, quickly came to the CFPB’s defense again.

“Despite what you will hear from Republicans, the leadership structure of the Consumer Bureau is not unique; in fact there are other federal regulatory agencies with similar structures,” Waters said. “But these facts haven’t stopped Republicans and some in the industry from making legal challenges to its structure.

“I reject these misguided attacks on the Consumer Bureau, and I will continue to stand up for the hardworking American consumers that the agency defends every day. The Consumer Bureau is an invaluable ally to consumers, and its work must continue,” she went on to say.

Cordray didn’t back down during his latest appearance on Capitol Hill. He defended the CFPB’s moves, including enforcement actions against companies such as Wells Fargo as well as to “clean up the problems” associated with credit reporting.

“Those who talk about weakening the Consumer Bureau are missing the importance of the work we are doing to stand up for individuals and families all over this country,” Cordray said during his opening statement. “Nobody should want to return to a system that failed us and produced a financial crisis that damaged so many lives.”

The entire hearing can be viewed here or via the window at the top of this page.

This past Friday, the American Financial Services Association (AFSA) submitted a list of regulatory reforms to the Trump administration that the organization insisted would provide relief to its members operating in the consumer credit industry and ultimately benefit customers and communities across the United States.

At the behest of Mark Calabria, chief economist for Vice President Mike Pence, AFSA made the proposals following a White House meeting of AFSA member company executives, representatives of the administration’s Domestic Policy Council and Calabria in March. AFSA’s proposals include:

—A halt to Consumer Financial Protection Bureau examinations

—Placing moratoriums on the use of disparate impact theory and the CFPB’s complaint database

—Withdrawing compliance bulletin 2015-07 on in-person collection of consumer debt

—Terminating the arbitration and small-dollar rulemakings

—Withdrawing compliance bulletins 2012-03 and 2016-02 on service providers

—Re-designating payments from the civil penalty fund

—Ensuring the accuracy of press releases as they relate to the enforcement actions to which they pertain, and;

—A general review of CFPB procedures

Additionally, the trade association submitted letters to Defense Secretary James Mattis regarding reforms to the Military Lending Act that would help U.S. military service members access beneficial forms of credit, and to Ajit Pai, chairman of the Federal Communications Commission regarding reforms to modernize the Telephone Consumer Protection Act (TCPA).

In a public appearance last Thursday, CFPB director Richard Cordray described what he contends is the bureau’s approach to regulatory implementation, “which we believe is key to helping industry avoid unnecessary burdens while achieving compliance.” Cordray delivered remarks during the U.S. Chamber of Commerce’s 11th annual Capital Markets Summit.

“As we approach our work, we have made it very clear that we see ourselves as a 21st century agency. What does this really mean? Among other things, it means an agency built on developing our own independent sources of data and ensuring a strong democratic foundation of public engagement,” Cordray said.

“Despite our best efforts, we recognize that the outcome of any human process will be imperfect. We learn from the comments we receive and our final rules are helpfully informed by that input on a consistent basis,” he continued. “But even after we issue a final rule, if the data shows over time that any of our substantive calls need to be reconsidered, we can and will face the issue frankly and address it. We will not let pride of authorship interfere with the serious task of policymaking in the interests of consumers and the American public.

“We believe our rulemaking process does not end with finalizing a set of rules,” Cordray went on to say. “It is not good enough for us to take the view that once new rules are published, our work is done and we can say to financial institutions that ‘it is your problem now.’ If the point of our regulations is to protect consumers and to promote fair, transparent, and competitive markets, then we should care a great deal about how well the rules are implemented. We feel that way especially because we fully appreciate the difficulty of the task and the constant perils of unintended consequences, changes in circumstances, and the difficulty of predicting the future.”

First, the development surfaced that the Department of Justice filed an amicus brief — a legal document filed in appellate court cases by non-litigants with a strong interest in the subject matter — questioning the Consumer Financial Protection Bureau being overseen by a single director.

Turns out, that stance was concurred by a collection of 15 state attorneys general, led by Kansas attorney general Derek Schmidt. These attorneys general argue that there are “unprecedented efforts” to insulate the CFPB director’s decisions from review result in "essentially unchecked administrative powers", which is at odds with the Constitution’s command that all executive power be vested in the president.

Schmidt made those assertions to the U.S. Court of Appeals for the District of Columbia Circuit, which will be conducting a rehearing of a case in which the initial decision reached last October called the CFPB “unconstitutionally structured.” The case pit the regulator against PHH Corp., a Mount Laurel, N.J.-based finance company that operates in the mortgage space.

It involved a three-judge panel of the court, which ruled the CFPB’s structure was constitutionally flawed and that its director, who currently is Richard Cordray, should be removable at the will of the president.

The 15 attorneys general argue that the states have an interest in ensuring the division of power within the federal system to avoid unauthorized encroachment on state authority and also to secure individual liberty and the opportunity for citizens to participate actively in governance. The states included in the amicus brief were:

—Alabama

—Arizona

—Arkansas

—Georgia

—Idaho

—Indiana

—Kansas

—Louisiana

—Missouri

—Nevada

—Oklahoma

—South Dakota

—Texas

—West Virginia

—Wisconsin

“The CFPB possesses the power to preempt or displace broad swaths of state regulatory authority,” the attorneys general wrote in their filing. “But the agency’s structure permits it to exercise this broad preemptive power without undertaking the careful deliberative processes that would be required of the elected branches of the federal government or of an independent agency headed by a multi-member board.

“Thus, the CFPB has a significantly reduced incentive to give proper weight to federalism interests than have the political branches or multi-member agencies,” they continued. “This reduced incentive increases the risk of federal agency encroachment on state prerogatives.”

The brief argues that the states have a direct interest in ensuring that the CFPB governance structure is accountable to democratically elected institutions.

A copy of the brief is available here.