The series of Auto Remarketing Podcasts featuring Dasceq founder and chief executive officer Abhishek Goel continues with a focus on how artificial intelligence (AI) can be the key ingredient in digital collections.

Goel defines what AI is in connection with collections and the importance of training and support to use it properly.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

This episode is the first in a series of Auto Remarketing Podcasts featuring Dasceq founder and chief executive officer Abhishek Goel and focusing on the potential digital technology has to revamp collections.

During the opening episode, Goel describes how technology can be used by a “new-age collector.”

To listen to the episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

The Consumer Financial Protection Bureau (CFPB) decided debt collection firms are ready to abide by new rules.

Last week, the bureau announced that two final rules issued under the Fair Debt Collection Practices Act (FDCPA) will take effect as planned on Nov. 30. The CFPB issued a proposal in April that — if finalized — would have extended the effective dates to Jan. 29.

The CFPB said in a news release that the regulator has now determined that such an extension is “unnecessary.”

Following this announcement, the CFPB added that it will publish a formal notice in the Federal Register withdrawing the April proposal.

The CFPB recapped that it proposed extending the final rules’ effective date by 60 days to allow stakeholders affected by the COVID-19 pandemic additional time to review and implement the rules.

“The public comments generally did not support an extension,” officials said. “Most industry commenters stated that they would be prepared to comply with the final rules by November 30, 2021.

“Although consumer advocate commenters generally supported extending the effective date, they did not focus on whether additional time is needed to implement the rules,” officials continued. “The alternative basis for an extension that many commenters urged, a reconsideration of the rules, was beyond the scope of the NPRM and could raise concerns under the Administrative Procedure Act.

“Nothing in this decision precludes the CFPB from reconsidering the debt collection rules at a later date,” officials went on to say.

The bureau recapped the two final rules under the FDCPA that now will take effect in November.

The first rule was issued in October and focuses on debt collection communications and clarifies the FDCPA’s prohibitions on harassment and abuse, false or misleading representations, and unfair practices by debt collectors when collecting consumer debt.

The second rule was issued in December and clarifies disclosures debt collectors must provide to consumers at the beginning of collection communications. The second rule also prohibits debt collectors from suing or threatening to sue consumers on time-barred debt.

Additionally, the CFPB noted that the second rule requires debt collectors to take specific steps to disclose the existence of a debt to consumers before reporting information about the debt to a consumer reporting agency.

The CFPB said it is committed to informing consumers about their rights and protections under the rules and assisting debt collectors in implementing them. Consumer education materials on debt collection and resources to help debt collectors understand, implement, and comply with the rules are available through consumerfinance.gov.

The CFPB went on to note that it will consider additional guidance for debt collectors, including those that service mortgage loans, as necessary.

“The CFPB recognizes that mortgage servicers are expected to receive a potentially historically high number of loss mitigation inquiries in the fall as large numbers of borrowers exit forbearance and that, as a result, mortgage servicers, in particular, may face capacity constraints,” officials said.

“The CFPB will continue to work with all market participants to ensure a smooth and successful implementation,” officials added.

Paper and forms sometimes still are a major part of auto financing, especially in connection with servicing and loss mitigation processes that are normally handled by people in the middle and back office who rely on manual processes and green-screen technology.

Constant is leveraging its latest partnership to help modernize those operational segments.

On Wednesday the provider of digitized, self-service technologies for banks and credit unions, announced a partnership with Alkami, a leading digital banking solutions provider.

Constant and Alkami are working together to deliver a “transformative” solution to enhance digital loan servicing and loss mitigation for banks and credit unions across the nation.

Despite the digitization of the front office, Constant explained that back-office practices sometimes can result in a delay in response times, costly errors, lost files, and increased non-compliance risk. With regard to hardship relief, Constant pointed out that clients and borrowers would need to call their banks, visit a branch or send an email to get payment assistance when experiencing financial hardship.

Constant and Alkami acknowledged wait times can be extreme, depending on the volume of requests.

“Our partnership with Constant is an exciting venture and one that will give us the opportunity to offer banks and credit unions in our client community a platform that digitizes antiquated, manual, back-office processes so borrowers can access debt payment relief and financial wellness information around the clock,” Alkami co-founder and chief strategy and sales officer Stephen Bohanon said in a news release distributed by Constant.

“Constant will help us deliver an enhanced digital experience that will empower our clients and their customers or members to obtain debt payment assistance seamlessly. We are thrilled to have them as a member of our Gold Partner Program,” Bohanon continued.

Constant, through the partnership with Alkami, will offer its hardship relief and financial wellness solutions to Maine-based cPort Credit Union. Constant’s self-service features will be available to cPort members as an extension of their existing online banking experience.

As the first credit union in Maine to offer expanded, digital loss mitigation services to its members, executives said cPort is delivering on its commitment to operate responsibly and generate long-term value and stability for those that need it most in the local community.

“When it comes to financial hardships, asking for help can be difficult. We care deeply about the communities we serve so making it easy for our members to connect and get the help they need was important to us,” said Kelsey Marquis, senior vice president and chief financial officer for cPort Credit Union.

“Constant allows us to deliver on our commitment to continuously drive innovation and provide leading-edge solutions to meet our members’ changing needs with the honesty, respect and fairness our members expect from us,” Marquis continued in the news release.

Constant chief executive officer Catherine York Powers reiterated the company’s mission while adding how the partnership with firms such as Alkami can result in client relationships like the one with cPort Credit Union

“With increased consumer protection scrutiny and borrowers demanding faster turnaround, servicers will need to refresh their strategies for managing customer and member interactions, retention and sustained financial hardships,” York Powers said. “As payment assistance, forbearance, and foreclosure relief come to an end, there is urgency to make those preparations to prepare for increased delinquency trends and avoid unnecessary consumer harm wherever possible.

“We are both encouraged by Alkami’s decision to tackle that responsibility proactively and are excited to support them and their clients,” she went on to say.

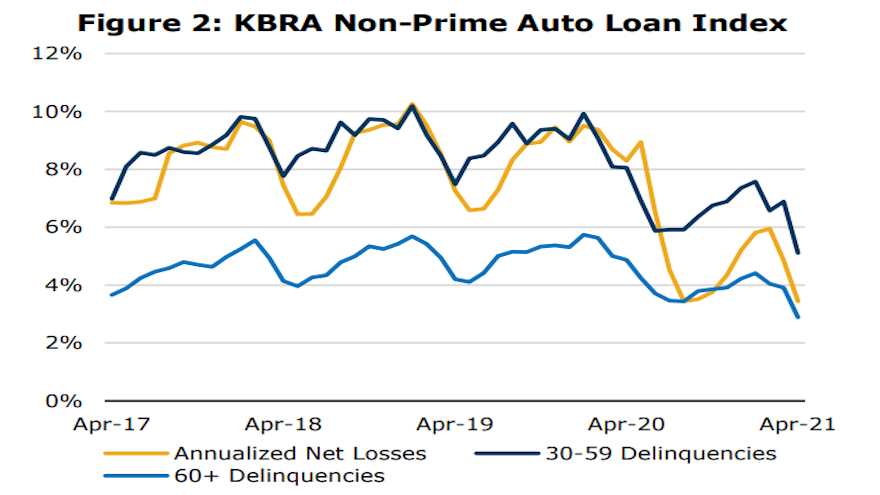

Kroll Bond Rating Agency (KBRA) used the descriptor “well grounded” when analysts dissected April remittance reports to discover the credit trends that surfaced during the March collection period.

KBRA indicated delinquencies for both non-prime and prime contracts decreased.

Analysts said in their newest report that early stage delinquencies — 30 to 59 days past due — in the KBRA Prime Auto Loan Index fell 23 basis points month-over-month to 0.67%, while late-stage delinquencies — more than 60 days past due — declined 11 basis points to 0.23%.

Meanwhile, the firm said early and late-stage delinquencies in the KBRA Non-Prime Auto Loan Index dropped 177 basis points and 102 basis points, respectively, coming in at 5.11% and 2.89%.

Analysts mentioned annualized net losses also trended lower in both indices during the month, “driven by favorable delinquency metrics and a frothy used-car market caused by strong demand and new vehicle production shortages, which has helped to keep recovery rates at elevated levels in 2021.”

KBRA also highlighted that contract prepayment rates rose sharply in March, mirroring a similar trend that analysts observed in other consumer loan sectors.

The firm determined prime and non-prime prepayments rose to 26.75% and 32.40%, respectively, up 13 percentage points and 11.8 percentage points versus the previous month.

“We expect the rise in prepayment rates to be transitory, as it is likely borrowers used the extra cash received from the third round of stimulus and tax rebates to pay down some of their outstanding debt during the month rather than accumulate savings as uncertainty is reduced and economic activity improves,” analysts said.

Furthermore, there was yet another upbeat metric to report. KBRA noted that its analysis of April’s Reg AB II asset-level disclosures showed improved credit metrics.

Analysts found that the percentage of prime and non-prime contract holders who went from 30 days delinquent to current rose to 47.9% and 44.9%, respectively. That’s up 1,323 basis points in prime pools and 1,634 basis points in non-prime pools versus the previous month.

And KBRA said the percentage of prime contract holders who slid from 60 days or more past due to charge-off dropped to 12.2%, down 77 basis points, while the non-prime roll rate into charge-off declined 357 basis points to 19.1%.

REPAY made a significant increase in its collections capabilities this week, announcing it has signed a definitive agreement to acquire BillingTree for approximately $503 million.

According to a news release, the acquisition will be financed with approximately $275 million in cash from REPAY’s balance sheet and $228 million in newly issued shares of REPAY Class A common stock to be issued to the seller.

The company said the transaction is subject to certain customary closing conditions and is expected to close by the end of the second quarter.

BillingTree, founded in 2003 and headquartered in Scottsdale, Ariz., is a leading provider of omni-channel, integrated payments solutions to the healthcare, credit union, accounts receivable management (ARM) and energy industries.

Through its technology-enabled suite of products and services, including a variety of payment channels and reporting capabilities, BillingTree helps organizations get paid faster and more efficiently.

“We are thrilled to announce this acquisition, our largest to date, and look forward to further expanding our position in healthcare, credit unions, and accounts receivable management with the help of BillingTree’s team and strong platform capabilities,” REPAY chief executive officer John Morris said in the news release. “BillingTree satisfies all of our acquisition investment criteria, including a large addressable market opportunity that is amid a shift away from legacy payment methods and towards the technology-first, industry-specific payment mediums in which BillingTree specializes.

“Additionally, BillingTree has strong recurring revenue streams, high customer retention, approximately 50 unique ISV integrations, an attractive financial profile, and numerous opportunities for synergy realization,” Morris continued. “We are looking forward to welcoming BillingTree into the REPAY family and together pursuing many amazing growth opportunities ahead.”

REPAY elaborated on how the BillingTree acquisition enhances scale and client diversification because of these elements:

— BillingTree serves more than 1,650 clients across multiple, attractive end markets with industry leading retention metrics

— BillingTree’s solutions are tightly integrated with more than 50 software platforms

— The acquisition is expected to increase REPAY’s total card payment volume to more than $20 billion on an annualized basis and expand REPAY’s software partner integrations to more than 175

“BillingTree’s unique approach has always been to develop strategic alliances with service, software, and billing providers resulting in full integrations that create seamless, compliant and innovative payment solutions,” Morris said. We believe that we are an ideal strategic partner for BillingTree, as we also go to market with a highly integrated, omni-channel approach.

“Together, we can capture more of the massive addressable market in payments and combine our incredible team members and technology to create simplified experiences for merchants across our collective, ever-expanding verticals,” Morris went on to say.

In more signs that the industry is returning to some normalcy, the Receivables Management Association International (RMAI) held its 2021 annual conference in Las Vegas earlier this month, welcoming more than 500 attendees in person and another 150 virtual attendees

RMAI leaders also capitalized on the event by honoring an outstanding member and RMAI’s executive director.

In 2017, RMAI created the President’s Award, which recognizes an individual for outstanding contributions and services to the association and membership. The award goes to someone serving on an RMAI committee who is selected because of contributions to committee goals and innovative ideas helping further the success of RMAI.

This year, RMAI presented the President’s Award to Amber Russo of Kino Financial, which is a certified debt buying company that joined RMAI in 2019.

“When faced with the need to change course and innovate, she champions the effort enthusiastically with tireless dedication ensuring success,” RMAI said in a news release. “Her efforts paid dividends as she co-chaired two successful virtual silent auctions that raised record donations for the RMAI Legislative Fund.

In addition to being a member of the fundraising committee, RMAI said Russo also served on the editorial and social media committee.

Russo also is a Certified Receivables Compliance Professional.

In what the organization said was a “closely guarded secret,” the RMAI board of directors awarded the Bud Reitzel Lifetime Commitment Award RMAI executive director, Jan Stieger.

RMAI created the Reitzel Award to recognize an individual for outstanding leadership and dedication in the receivables management industry who has demonstrated ideals the namesake demonstrated during many years of service.

Stieger joined RMAI in 2011. Through her leadership, the organization highlighted that she has overseen the complete transformation of RMAI from an entity operated by an association management company to “one of the most dynamic and respected organizations within the receivables management industry.”

RMAI pointed out that Stieger’s many accomplishments over the past decade include:

• The development of a robust state and federal government advocacy program that has protected the industry and driven significant policy changes. Since 2011, RMAI said it has been successful in over 95% of its advocacy efforts.

• Launching and the continued enhancement of the Receivables Management Certification Program from a program originally focused on debt buying companies to a highly valued program that benefits the entire receivables industry, by providing significant operational controls and consumer protections contained in rigorous and uniform industry standards for certified debt buyers, collection agencies, collection law firms, brokers and process servicers.

• Expanding RMAI’s education and networking experiences from RMAI’s annual conference and executive summit to regional events such as this September’s Advocacy Training and Baseball Night in Atlanta.

• Rebranding the association in 2017 from DBA International to RMAI with an expanded focus on secondary market opportunities and RMAI certification, both of which continue to grow RMAI’s footprint today.

• Successfully led RMAI through the many challenges associated with the COVID-19 pandemic. Despite the issues faced by the industry as well as membership in 2020, RMAI is now in its fourth straight year of membership growth.

Efforts by ACA International and other industry organizations connected with collections helped to generate what they called the “favorable ruling” earlier this month when the U.S. Supreme Court unanimously decided a case involving the Telephone Consumer Protection Act (TCPA) and definition of an autodialer.

In Facebook versus Duguid, ACA International recapped that the court held to qualify as an “automatic telephone dialing system” under the TCPA, a device must have the capacity either to store a telephone number using a random or sequential number generator, or to produce a telephone number using a random or sequential number generator.

“The Supreme Court’s decision in Facebook vindicates the more than decade of advocacy ACA International and its members have engaged in to seek clarity on the TCPA, which is often abused by lawyers in the plaintiffs’ bar seeking to profit off of small businesses and other legitimate informational callers. The Supreme Court’s decision is an important step forward in recognizing that Congress has always intended this statute for abusive telemarketers or bad actors, not legitimate callers that consumers need information from,” ACA International chief executive officer Mark Neeb said in a statement

“ACA and industry trade associations filed an amici curiae brief in the case to advocate for legal clarity when using modern methods to communicate with consumers as well as clarity on the definition of an autodialer,” Neeb continued.

“ACA has been advocating with the Federal Communications Commission, Congress, and at the Supreme Court to take action to provide clarity surrounding overbroad interpretations of an ATDS. This decision is a step forward in those efforts to clarify the law,” he went on to say.

ACA drilled deeper into the implications of this decision through an online training session featuring:

— Leah Dempsey, vice president and senior counsel of federal advocacy, ACA International

— David Kaminski, partner, Carlson & Messer LLP

That online session is available on this website.

Perhaps here’s some news on a Friday that might help finance companies and their collectors exhale a bit.

The Consumer Financial Protection Bureau this week proposed extending the effective date of two recent debt collection rules to give affected parties more time to comply due to the ongoing COVID-19 pandemic.

According to a news release, the CFPB issued a notice of proposed rulemaking (NPRM) to delay by 60 days the effective date of two final rules issued under the Fair Debt Collection Practices Act (FDCPA).

The debt collection rules, issued late last year, were scheduled to take effect on Nov. 30. The CFPB is proposing to extend the effective date of both rules to Jan. 29.

“The proposed delay would allow stakeholders affected by the pandemic additional time to review and implement the rules,” the bureau said.

The CFPB recapped that the first debt collection rule issued in October focuses on the use of communications related to debt collection and clarifies prohibitions on harassment and abuse, false or misleading representations and unfair practices by debt collectors when collecting consumer debt.

Officials added that the second debt collection rule rolled out in December clarifies disclosures debt collectors must provide to consumers at the beginning of collection communications. The CFPB said the rule also prohibits debt collectors from making threats to sue, or from suing, consumers on time-barred debt.

“The rule requires debt collectors to take specific steps to disclose the existence of a debt to consumers before reporting information about the debt to a consumer reporting agency,” officials said.

The CFPB added the latest proposal will be open for comment for 30 days following publication in the Federal Register. You can read the text of the entire proposal on this website.

In collaboration with the Federal Trade Commission (FTC), the Consumer Financial Protection Bureau (CFPB) this week released the 2020 annual report to Congress on the administration of the Fair Debt Collection Practices Act (FDCPA).

Officials said the report highlights efforts by the CFPB and the FTC to protect consumers, particularly those who have suffered profound financial impacts due to the COVID-19 pandemic. They added the CFPB and the FTC — along with state and federal partners — accomplished much toward stopping unlawful debt collection practices and continuing their vigorous law enforcement, consumer education and public outreach and policy initiatives.

Last year, the CFPB recapped that it engaged in four public enforcement actions, arising from alleged FDCPA violations. The CFPB resolved two of these cases. The two judgments ordered nearly $15.2 million in consumer redress and $80,000 in civil money penalties. Two cases remain in active litigation.

Among other highlights, the report notes the following CFPB accomplishments:

— Identified several issues that raise the risk of consumer harm during the COVID-19 pandemic through its supervisory prioritized assessments

— Published content to help consumers financially navigate the COVID-19 pandemic, including on debt collection, that has been accessed by users approximately 4.3 million times;

— Provided consumer debt collection educational materials, including, “Ask CFPB,” an interactive online consumer education tool that logged 1.9 million pageviews and/or downloads in English and 220,000 in Spanish for its debt collection questions;

— Released a report highlighting servicemembers’ complaint data from 2019

— Published information about debt collection activity during the pandemic for student loans

— Published results of a quantitative online survey of over 8,000 respondents to test several versions of disclosures to support the understanding of time-barred debt and revival that informed the CFPB’s final rules on debt collection.

Meanwhile over at the FTC, among the actions taken to combat unfair, deceptive, and otherwise unlawful debt collection practices in 2020, the regulator mentioned:

— Led Operation Corrupt Collector, a nationwide federal and state law enforcement sweep and outreach initiative targeting phantom debt collection and abusive and threatening debt collection practices

— Filed or resolved seven cases against 39 defendants, and obtained $26 million in judgments

— Brought the first federal action combatting unlawful “debt parking”

— Banned the operator of a debt collection scheme who engaged in serious and repeated violations of law from ever working in debt collection again;

— Deployed educational materials to inform consumers about their rights, and educate debt collectors about their responsibilities, under the FDCPA and FTC Act

— Supplied 15,755 copies of a fotonovela (a novel) on debt collection, developed for Spanish speakers, to raise awareness about scams targeting the Latino community

The CFPB and the FTC share authority to enforce the FDCPA, and continue to work closely to coordinate efforts to protect consumers from unfair, deceptive, and abusive debt collection practices. The two agencies reauthorized a permanent memorandum of understanding in February 2019 that facilitates consultation in rulemaking, enables coordination in enforcement, sharing of supervisory information and consumer complaints and collaboration on consumer education.

The complete report can be downloaded here.