Experian senior director of automotive financial solutions Melinda Zabritski made a suggestion to finance companies after Experian released its Q3 2020 State of the Automotive Finance Market report on Thursday.

The recommendation came in connection with a metric that providers might already watch with a laser focus — delinquencies — even as the subprime segment continues to shrink to a new low.

According to the report, 30- and 60-day delinquency rates improved in the third quarter, coming in at 1.56% and 0.51%, respectively.

Comparatively, a year ago, Experian reported the 30-day delinquency rate stood at 2.25% and the 60-day delinquency rate sat at 0.75%.

“While the decline in 30- and 60-day delinquency rates is a positive trend for the industry, particularly with some of the accommodation programs coming to an end, we do need to consider the impact these programs have had on consumers,” Zabritski said in a news release.

“Some consumers likely leveraged financial assistance programs to manage through hardship, so it’s important for lenders to keep a close eye on how delinquency rates evolve over the coming quarters,” she continued. “Nonetheless, the improvement is a positive sign for the country’s economic recovery.”

Overall, the industry is taking on less risk as Experian pegged the subprime segment of all financing at 19.23% in the third quarter, representing a record low in its database.

And in Q3, analysts added that deep subprime financing remained below 3% of the overall market.

Beyond influencing consumers’ ability to manage monthly payments and perhaps how much appetite finance companies have for subprime, Experian pointed out the pandemic also has impacted overall volume.

However, despite fewer vehicle sales, analysts discovered outstanding balances still grew 2.8% from a year ago, reaching $1.2 trillion. This increases also comes at a time where a smaller percentage of vehicles are being financed.

Experian indicated the percentage of new vehicles with financing was 82.43% in Q3 compared to 86.99% the previous year. Similarly, the percentage of used vehicles with financing was 33.71% in Q3 compared with 39.79% over the same period.

“It is important to note, the drop in the percentage of vehicles with financing can also be attributed to an increase in cash transactions,” Experian said.

Prime consumers continue to opt for used vehicles

During the first few months of the pandemic, Experian recapped that automakers offered new-vehicle incentives to improve sales. As a result, analysts saw prime borrowers opt for new vehicles, reversing a trend they observed in previous quarters.

With fewer incentives offered during the third quarter, Experian found that a higher percentage of prime consumers shifted back to used.

In fact, analysts reported prime and super prime contract holders made up 55.3% of used vehicles financed during the quarter, a new high for used-vehicle financing.

Experian sees the shift back to the used vehicle market is likely driven by continued affordability conversations; a metric that Cox Automotive and Moody’s Analytics recently chose to track more closely.

The newest Experian report showed both the average amounts financed for both new and used vehicles increased in Q3.

The average amount financed for a new vehicle rose more than $2,000 over the previous year, reaching $34,635, while the average amount financed for a used vehicle climbed $945 to $21,438 over the same period.

Analysts explained the increases could also be attributed to consumer preference, with buyers leaning toward larger, more expensive vehicles.

Experian noted that small SUVs were the most purchased vehicles, making up 26.01% of contracts in Q3, followed by midsize SUVs at 24.15%.

Despite the increases in average amounts finance, Experian mentioned the increases in average monthly payment weren’t as sharp.

To be exact, analysts said the average new-vehicle payment amount increased $11 year-over-year, reaching $563 in Q3. The average used-vehicle payment ticked up $6 to $397.

To keep those monthly payment manageable, finance companies are absorbing more risk by stretching terms and edging rates lower.

Experian determined the average term for new vehicles financed during the third quarter increased slightly to 69.68 months, up from 68.98 months a year earlier. And the average term for used vehicles financed in Q3 increased from 64.49 months to 65.15 months.

Analysts went on to note that the average interest rate for a new-vehicle contract booked in Q3 saw sharp decrease, sliding from 5.38% in Q3 of last year to 4.22% in Q3 of this year. The average interest rate for used-vehicle paper originated in Q3 dropped from 9.09% to 8.43% year-over-year.

“With affordability still top of mind, particularly during the pandemic, lower interest rates have certainly helped consumers keep monthly payments at a manageable level,” Zabritski said.

“As the market evolves and financial situations shift, it’s important for lenders and dealers to stay close to the trends and make strategic decisions that help keep the industry moving forward and consumers in their vehicles.”

Additional findings for Q3

Experian closed its latest update by mentioning a trio of other trends, including:

• Average credit scores saw a sharp increase for new vehicles, jumping from 728 in Q3 2019 to 732 in Q3 2020. The average credit score for used vehicles also saw a one-point increase from 664 to 665 year-over-year.

• New-vehicle leasing continued decrease in Q3 2020, comprising 26.2% of new-vehicle financing, compared to 30.27% in Q3 2019.

• Captive finance companies continued to increase market share, rising from 30.85% in Q3 2019 to 34.49% in Q3 2020. The buy-here, pay-here segment saw a slight increase from 4.32% to 4.69%, while all other provider categories sustained year-over-year decreases.

To view the entire Q3 2020 State of the Automotive Finance Market report webinar, go to this website.

Fitch Ratings, Kroll Bond Rating Agency (KBRA) and S&P Global Ratings each offered perspectives on the securitization market this week.

After sharing metrics their analysts gathered, each firm pointed to two trends moving in opposite directions. All three highlighted how contract modifications are declining and as a result, delinquencies are climbing with the expectation for potential acceleration coming in 2021.

The rundown received by SubPrime Auto Finance News began with S&P Global Ratings publishing its look at the U.S. auto loan asset-backed securities (ABS) sector’s performance for September.

S&P Global Ratings said U.S. prime auto loan ABS performance strengthened in September, with losses declining to an eight-year low due to an extremely strong recovery rate of nearly 80%. Analysts noticed that extensions also decreased for the fifth straight month in this credit space.

Meanwhile, S&P Global Ratings indicated recovery rates started to normalize for subprime paper, causing losses to increase from its lowest recorded level in August. Analysts added this segment reported higher extensions for the first time in five months.

S&P Global Ratings shared more context when the firm elaborated about particular vintages.

“Prime and subprime static pool data indicate that the 2018 and 2019 vintages are currently performing in line with or better than the 2017 vintage,” analysts said in their report. “However, caution is warranted because losses associated with previously extended loans won't appear for several months.

“Additionally, the federal government’s pandemic emergency unemployment compensation, providing an additional 13 weeks of unemployment assistance over what the states offer, is set to expire at year end,” they went on to say.

Update from KBRA

The latest report from KBRA included information from October data.

The firm said early stage delinquencies in the KBRA Prime Auto Loan Index rose 2 basis points month-over-month to 0.91% in October, while late-stage delinquencies remained unchanged at 0.37%.

Furthermore, analysts determined early and late-stage delinquencies in the KBRA Non-Prime Auto Loan Index climbed to 6.76% and 3.86%, respectively, in October. Those readings represented rises of 39 basis points and 10 basis points compared to the previous month.

But KBRA pointed out both delinquency metrics remained “meaningfully” lower on a year-over-year basis, adding that annualized net loss rates are at their lowest levels in years. Analysts explained those findings arrived as a result of a “strong” used-vehicle market and low delinquency rates throughout the spring and summer months.

“Further stimulus, which at this point is uncertain, and a continuing labor market recovery could help soften the blow, but we still expect seasonal trends and the end of payment holidays for many borrowers to push delinquency rates higher (as observed in the past two months) into year end, leading to elevated charge-off rates and annualized net losses in 2021,” KBRA analysts said in their newest report.

KBRA went on to mention an analysis of October’s asset-level disclosures showed mixed credit metrics during the September collection period.

Analysts discovered the percentage of prime and non-prime contract holders who went from 30-days delinquent to current increased to 33.9% and 28.9%, respectively. Those moves marked jumps of 46 basis points and 151 basis points versus the previous month, which in both cases were slightly below their pre-pandemic levels, according to KBRA.

The firm also found that the percentage of prime contract holders who rolled from 60 days or more past due to charge-off fell to 12.5% in October, declining 98 basis points month-over-month.

However, analysts added the non-prime roll rate into charge-off jumped 99 basis points to 19.1%. “But this was still well below pre-pandemic levels,” they said.

Views from Fitch Ratings

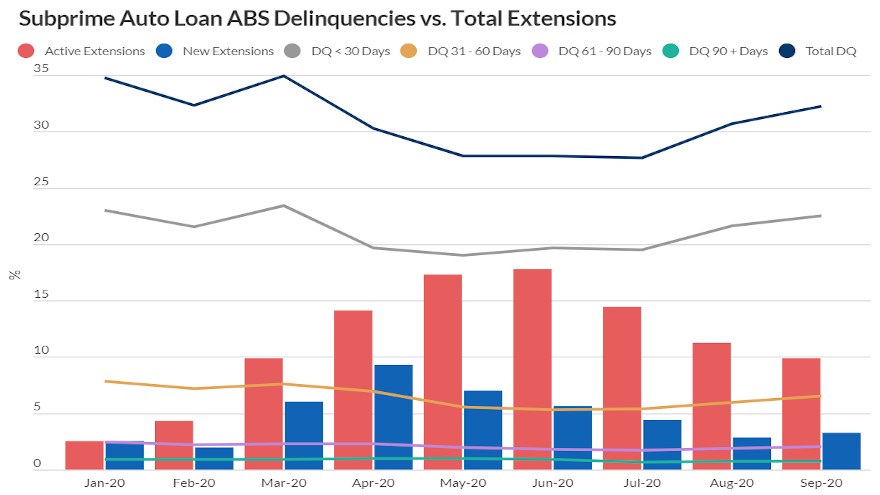

Fitch Ratings began its update by projecting a “moderate” increase in delinquencies, particularly for subprime auto ABS because of expiring contract extensions and other forms of payment relief that surged this spring and summer.

“We have not observed a meaningful increase in delinquencies given vehicle utility and priority of auto loan debt repayment during the pandemic, but additional federal stimulus is uncertain and unemployment remains materially elevated,” Fitch Ratings said.

“Slow economic growth over the next few months as a result of additional pandemic-related lockdowns may lead to another increase in extension take rates that masks true delinquency levels,” analysts continued.

The firm noted that the average of new extension requests across Fitch-rated prime and subprime auto loan ABS pools peaked in April at 5.7% and 9.8%, respectively. But Fitch said they have subsequently declined to 0.7% and 3.1% in September.

“Prime extension requests are only slightly elevated from pre-pandemic levels and continue to trend downward, but subprime extension requests began to tick back up in September,” analysts said.

Despite having an active extension, Fitch calculated that an average of 23.4% of prime contract holders and 20.6% of subprime contract are current with their payments, and an additional 19.9% of prime customers and 10.4% of subprime customers have made a partial payment.

Given the unprecedented widespread use of payment extensions, Fitch explained how it arrived at these readings.

The firm said it began using contract-level data to analyze the less than 30-day delinquency buckets in conjunction with extension take rates.

“This can serve as an early warning indicator of potential deterioration in securitized pools and provide further insight to what is provided in the monthly servicer report,” analysts said.

With all of the accommodations in play and an updated tracking strategy, Fitch recapped what they discovered with regard to delinquency rates, with the most pronounced movements being seen in early stage delinquency buckets.

Fitch said the less than 30-day delinquency category averaged 6.0% for prime ABS and 22.3% in subprime pools through the first two months of 2020, but dropped to a low of 5.0% and 19.0%, respectively, in the spring.

“As extensions began to expire, the less than 30-day delinquency bucket trended back up toward pre-pandemic levels, indicating the benefit from stimulus and extensions is fading, and struggling borrowers may again be under pressure,” analysts said.

“We expect a moderate increase in delinquencies, particularly for subprime ABS, given continued high unemployment rates and in the absence of additional federal aid,” analysts continued. “However, delinquencies are not expected to reach levels seen during the prior recession.

At the height of that recession in December 2008, Fitch recollected that 60-day prime delinquencies peaked at 0.9% and subprime at 5.0%. As of September, Fitch pointed out 60-day prime delinquencies stood at 0.2% and at 3.8% for subprime auto ABS pools.

Fitch closed its latest update by trying to crystalize its 2021 forecast, setting an expectation for limited impact on auto loan ABS ratings moving into the new year.

“Our base case credit loss proxies reflect a through-the-cycle rating approach, include a loss cushion and are not expected cases,” analysts said.

“Fitch uses stressed recessionary 2008-2009 loss levels along with more recent vintage performance to derive auto loan ABS base case cumulative net loss proxies,” they continued. “Therefore, we believe there is sufficient cushion to protect against potential negative performance trends.”

To account for contract performance during the pandemic, Fitch explained its approach for both new transaction analysis and surveillance more heavily weights the poorer performing 2008-2009 recessionary vintages.

Analysts said this choice resulted in roughly a 10% to 20% increase in Fitch’s cumulative net loss proxies from pre-pandemic levels, depending on issuer-specific performance and other items such as amortization observed in outstanding prime and subprime transactions.

The most recent TransUnion financial hardship survey conducted in late October pinpointed how short of funds individuals and families financially impacted by the pandemic are toward meeting their monthly obligations.

According to the online survey of 3,100 adults conducted by TransUnion in partnership with third-party provider Qualtrics Research Services, these households land $886.70 short of keeping up with line items such as installment contracts for vehicles, a mortgage or rent, utilities and other necessities.

The TransUnion survey also highlighted the top six specific reasons why. They included:

— I own a small business that closed/orders dried up: 16%

— I’ve lost my job: 19%

— I/we relied on part-time job to supplement income: 18%

— Partner lost job/reduced work hours: 25%

— My work hours have been reduced: 42%

— Other: 13%

Among the participants, 24% told TransUnion they would not be able to maintain their vehicle payments. That reading is lower than other categories such as credit cards (38%), utilities (35%) and mobile phone bill (30%).

To pay bills and loans, TransUnion reported 32% of impacted consumers state they plan to use money from savings. The latest installment of the survey also showed borrowing money from family and friends remains flat at 23%.

When further broken down, TransUnion noted that 53% plan to borrow from friends, 51% from parents, 44% from other family members and 22% from a crowdfunding site.

TransUnion went on to mention that consumers continue to indicate they will rely on credit to pay their bills and loans at the highest levels of this study. One-fifth plan to use credit cards or balance transfers, 16% plan to take out personal loans and 13% intend to open new credit card.

With such a high volume of consumers currently navigating financial challenges, DRN recently reiterated in a company blog post about how it’s trying to help finance companies with its data before a vehicle repossession becomes necessary.

Strategic account manager Jared Kirby recapped that one of DRN’s first enterprise clients was a large captive finance company.

“They were long-time users of DRNsights’ vehicle location data in their repossession processes but wanted to brainstorm how they might use it pre-repo to make better repo decisions,” Kirby wrote.

“We partnered with this client to pull DRN data into their behavioral scoring model to help them make better decisions on if and when to repossess vehicles. We started by looking at a handful of accounts that were nearing repo stage and saw that some had very consistent license plate scans,” he continued. “This makes those vehicles easy to find and, in some cases, meant this lender could easily contact the borrower and secure payments or create payment arrangements.

“This is always a better outcome than repo — the borrower stays in their car and the lender receives its payments and avoids a costly repossession,” Kirby went on to note.

As contract extensions and other accommodations by finance companies continue to expire, auto defaults continue to rise.

According to data through October released by S&P Dow Jones Indices and Experian, auto defaults now have climbed for four consecutive months after bottoming out a record low in June at 0.40%.

Analysts pegged the October reading at 0.59%. Back in January before the pandemic arrived, they said auto defaults stood at 0.99%.

And looking back 10 years ago as auto financing still was rebounding from the Great Recession, S&P Dow Jones Indices and Experian had auto defaults at 2.04%.

Meanwhile, the other parts of the newest S&P/Experian Consumer Credit Default Indices continue to decline.

The composite rate, which represents a comprehensive measure of changes in consumer credit defaults dropped 10 basis points to 0.53%.

Analysts said the bank card default rate fell 20 basis points to 2.80%, and the first mortgage default rate decreased 11 basis points to 0.35%.

Looking at the default data with the five largest metropolitan areas, S&P and Experian discovered they all dropped in October compared to the previous month.

Analysts found that Miami posted the largest decrease, sinking 67 basis points to 1.13%.

New York dropped 30 basis points lower to 0.58%, while Los Angeles declined 18 basis points to 0.53%.

Analysts added the rate for Chicago dipped 7 basis points to 0.58% as Dallas edged 1 basis point lower to 0.61%.

Jointly developed by S&P Indices and Experian, analysts noted the S&P/Experian Consumer Credit Default Indices are published monthly with the intent to accurately track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien.

The indices are calculated based on data extracted from Experian’s consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month.

Experian’s base of data contributors includes leading banks and mortgage companies and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

S&P Global Ratings spotted yet another difference between the prime and subprime auto finance segments.

In September, analysts discovered new extension rates between U.S. prime and subprime auto loan asset-backed securities (ABS) diverged.

For public shelves with 17 issuers, S&P Global Ratings reported the prime segment posted its fifth consecutive month of declines in extensions, as the weighted average monthly rate dropped 12.7% to 0.55% from 0.63%.

In contrast, analysts indicated subprime extensions across the four public shelves — SDART, DRIVE, AmeriCredit and World Omni Select 2019-A — increased 13.4% to 3.65% from 3.22%.

S&P Global Ratings then looked to explain why these trends surfaced.

“We believe that the uptick in the subprime extension rate was primarily due to enhanced unemployment benefits dropping to $300 a month from $600. Some unemployed consumers continued to receive the $600 benefit into early August, but September was the first full month of the lower benefit amount,” analysts said in a news release.

“At the same time, many workers in people-facing businesses such as hospitality and retail remain unemployed or underemployed,” analysts continued.

“Furthermore, Hurricane Laura, which caused significant damage to Louisiana at the end of August, also contributed to higher loan extensions,” analysts went on to say. “Louisiana had the highest extension rates in the U.S. for September for both prime and subprime pools.”

A TransUnion financial hardship survey in late October showed that more than half of Americans — 54% to be exact — said they have been financially impacted by the COVID-19 pandemic.

And TransUnion’s origination data for both auto financing and personal loans reflect that effect.

Looking at originations booked during the second quarter, TransUnion reported that the auto-finance market experienced an 11.9% year-over-year decline with 6.5 million new contracts opened in Q2 2020, compared to 7.3 million in Q2 2019.

While originations decreased across all tiers, analysts pointed out this drop was particularly noticeable among subprime consumers as this risk tier declined 28.1% over the same period last year.

Despite the recent decline, TransUnion said originations are expected to improve quarter over quarter in Q3 as the auto market moves past the large-scale shutdowns from earlier this year that contributed to dealership closures.

Analysts added that subprime origination growth will likely continue to lag other risk tiers as finance companies skew their portfolios toward lower-risk consumers.

“While the overall percentage of auto accounts leveraging financial accommodation programs has been declining, there were approximately 3.8 million auto accounts in some form of accommodation at the end of September,” said Satyan Merchant, senior vice president and automotive business leader at TransUnion.

“The consumers that are still enrolled in such programs are the ones likely experiencing the greatest financial hardship as the risk mix of these consumers has been increasingly shifting toward subprime over the last few months,” Merchant continued in a news release that accompanied the Q3 2020 Industry Insights Report.

“Performance has largely held steady, but as economic stimulus funds evaporate and consumers exit accommodation, future delinquencies may see an impact,” he went on to say.

Q3 2020 Auto Loan Trends

|

Auto Lending Metric

|

Q3 2020

|

Q3 2019

|

Q3 2018

|

Q3 2017

|

|

Number of Auto Loans

|

83.7 million

|

83.4 million

|

81.9 million

|

78.6 million

|

|

Borrower-Level Delinquency Rate (60+ DPD)

|

1.45%

|

1.40%

|

1.36%

|

1.40%

|

|

Average Debt Per Borrower

|

$19,646

|

$19,145

|

$18,835

|

$18,567

|

|

Prior Quarter Originations*

|

6.5 million

|

7.3 million

|

7.3 million

|

7.1 million

|

|

Average Balance of New Auto Loans*

|

$23,850

|

$21,953

|

$20,998

|

$20,653

|

*Note: Originations are viewed one quarter in arrears to account for reporting lag. Source: TransUnion

Meanwhile, TransUnion discovered personal loan balances decreased, too, as lenders and consumers navigated COVID-19.

Analysts determined total balances in the consumer-lending industry declined to $151 billion in Q3 2020, down from $156 billion in Q3 2019, following a dramatic drop off in originations due to the COVID-19 crisis

TransUnion explained the first full quarter of COVID-19 impacted originations — which was Q2 2020 — created a decline of 46.2% year-over-year as lenders temporarily exited the market, tightened underwriting and shifted their portfolio mix toward lower risk consumers.

Analysts noted that decreased consumer demand for credit also contributed to the drop-off as stay-at-home orders drove decreased spending and stimulus funds provided additional liquidity.

TransUnion mentioned that performance has remained stable as serious delinquencies improved to a 10-year low of 2.53% in Q3. Delinquencies were down across all risk tiers, with the exception of super prime, which remained low, but ticked up to 0.03% from 0.02% in Q2.

“The pandemic drove a nearly 50% reduction in consumer lending originations in Q2 2020 versus the prior year,” said Liz Pagel, senior vice president and consumer lending business leader at TransUnion.

“Lender pullback and decreased consumer demand continued over the past quarter as we saw total balances in the consumer lending market contract for the first time since early 2012,” Pagel continued in the news release.

“Lenders are expected to ramp up originations in Q4 for the holiday season as investor demand returns to the sector,” she went on to say. “The loans outstanding continue to perform well with delinquencies at the lowest point in a decade even as consumers begin to exit forbearance programs.”

Q3 2020 Unsecured Personal Loan Trends

|

Personal Loan Metric

|

Q3 2020

|

Q3 2019

|

Q3 2018

|

Q3 2017

|

|

Total Balances

|

$151 billion

|

$156 billion

|

$132 billion

|

$112 billion

|

|

Number of Unsecured Personal Loans

|

21.4 million

|

22.5 million

|

20.3 million

|

17.5 million

|

|

Number of Consumers with Unsecured Personal Loans

|

19.4 million

|

20.2 million

|

18.5 million

|

16.4 million

|

|

Borrower-Level Delinquency Rate (60+ DPD)

|

2.53%

|

3.28%

|

3.41%

|

3.13%

|

|

Average Debt Per Borrower

|

$9,067

|

$8,998

|

$8,338

|

$8,017

|

|

Prior Quarter Originations*

|

2.6 million

|

4.8 million

|

4.5 million

|

3.6 million

|

|

Average Balance of New Unsecured Personal Loans*

|

$6,092

|

$6,382

|

$6,253

|

$6,140

|

*Note: Originations are viewed one quarter in arrears to account for reporting lag. Source: TransUnion.

Perhaps if finance companies wanted to expand their customer databases even more, what Byrider commemorated on Friday might give providers an opportunity.

To go with columns already in place for the customer’s address as well as the VIN, another segment could list names like Harry, Bonnie and Big Blue.

Byrider sent me a message this week saying they were celebrating National Name Your Car Day, prompting me to ask what triggered the chain of buy-here, pay-here dealerships to roll out a campaign that even has hashtag for social media — #ByriderNameYourCarDay.

“We are always looking for fun ways to celebrate our customers at Byrider and purchasing a vehicle is usually such a happy time for people. It seems like there’s just about a day for everything now, and we thought this was a perfect way to combine what we do with one of those ‘national days,’” Byrider chief marketing officer Walter Scott told me via email.

“Every day, we get to experience first-hand the impact a vehicle can have on a customer’s life, truly becoming almost like a member of their family as soon as they drive off the lot,” Scott continued. “Name Your Car Day is a fun opportunity to celebrate our customers, their new ‘family member’ and what we do, which is helping people move forward.”

Scott’s reply got me thinking that indeed our vehicles often are like part of the family. In my household, my primary driver is a Toyota RAV4 named Terry. My wife’s vehicle is a Toyota 4Runner named Katrina. Previously, we wrung every bit of life out of a Honda Accord named Harry, who expired after nearly 16 years of operation and almost 300,000 miles.

Some of my Cherokee Media Group colleagues also have dear four-wheeled family members, too. Or a vehicle that brings back fond memories

SubPrime Auto Finance News publisher Amanda Dunlap has Bonnie, her Barcelona Red Metallic Toyota 4Runner named in reference to famous red-haired singer Bonnie Raitt. Auto Remarketing Podcast executive producer Matt Rice used to drive Big Blue, a Dodge Magnum with impressive aftermarket wheels.

Scott shared his perspective about the unique connection of the owner to a vehicle to create a special name for it.

“It says so much and often brings back that great feeling of owning your very first car. We love that people are connected to their car,” Scott told me.

“Vehicles empower drivers and give them freedom. Whether the car is getting them to an essential job that provides for their family or to a loved one’s house for a special occasion, our vehicles get us where we need to be to make life’s most special memories,” he went on to say.

Scott’s point is even more poignant nowadays with our vehicles sometimes serving as a sanctuary during the pandemic. They are the extra dining rooms and living rooms for individuals and families.

So maybe if finance companies need an icebreaker to re-engage conversations with customers about their installment contracts, perhaps representatives could ask what the vehicle’s name is, reinforcing how valuable that car is to both the consumer and provider.

Nick Zulovich is senior editor at Cherokee Media Group and can be reached at [email protected].

While credit performance has improved during recent reporting periods, TransUnion is cautious about the sustainability that contract holders can continue to make their monthly auto-finance payments along with other credit obligations. That sentiment stems from findings through its latest consumer survey.

TransUnion reported on Thursday that serious delinquency rates in August improved once more across all consumer credit segments — including auto financing, credit cards, mortgages and personal loans — even as the number of people in accommodation programs dropped for the second consecutive month.

That assertion is part of TransUnion’s latest Monthly Industry Snapshot, which also points to potential challenges in the near future.

Since the start of the pandemic in March, TransUnion indicated consumer performance has been mostly positive with continued month-over-month improvements for many of these credit products.

“A significant percentage of consumers utilized financial accommodations to defer or freeze payments during the early stages of the pandemic. As the first wave of consumers exit accommodation and a period of excess liquidity, they are returning to their debt obligations and continuing to perform,” said Matt Komos, vice president of research and consulting at TransUnion.

“Consumers who still remain in hardship could be more likely to face income losses and thus have more difficulty exiting these programs than consumers who may have entered into hardship programs as a precautionary measure,” Komos continued in a news release.

August Industry Snapshot of Consumer-Level Delinquency Performance by Credit Product

|

Timeframe

|

Auto

|

Credit Card

|

Mortgage

|

Personal Loans

|

|

August 2020

|

1.39%

|

1.23%*

|

1.03%

|

2.53%

|

|

July 2020

|

1.43%

|

1.37%*

|

1.08%

|

2.79%

|

|

June 2020

|

1.50%

|

1.48%*

|

1.07%

|

3.11%

|

|

May 2020

|

1.55%

|

1.76%*

|

1.14%

|

3.14%

|

|

April 2020

|

1.33%

|

1.87%*

|

1.27%

|

3.27%

|

|

March 2020

|

1.37%

|

1.96%*

|

1.40%

|

3.40%

|

|

August 2019

|

1.32%

|

1.72%*

|

1.45%

|

3.08%

|

*Credit card delinquency rate reported as 90+ DPD per industry-standard; all other products reported as 60+ DPD. Source: TransUnion

The August Monthly Industry Snapshot Report found the percentage of accounts in “financial hardship” continued a downward month-over-month trajectory for auto financing, credit cards, mortgages and personal loans from the months of July to August.

TransUnion explained its financial hardship data includes all accommodations on file at month’s end and includes any accounts that were in accommodation prior to the COVID-19 pandemic.

Across all credit products, analysts determined the percentage of accounts in financial hardship during the month of August dipped to pre-May levels. Accommodation programs provided consumers with payment flexibility and added liquidity during the course of the pandemic.

However, as the number of consumers leveraging such programs decreases and government relief funds are not expected to renew, TransUnion acknowledged many consumers may find themselves at what the credit bureau called “an inflection point.”

August Industry Snapshot of Financial Hardship Status by Credit Product

|

Timeframe

|

Auto

|

Credit Card

|

Mortgage

|

Personal Loans

|

|

August 2020

|

4.32%

|

2.21%

|

5.92%

|

5.14%

|

|

July 2020

|

6.16%

|

2.83%

|

6.15%

|

6.92%

|

|

June 2020

|

7.21%

|

3.57%

|

6.79%

|

7.03%

|

|

May 2020

|

7.04%

|

3.73%

|

7.48%

|

6.15%

|

|

April 2020

|

3.54%

|

3.22%

|

5.00%

|

3.57%

|

|

March 2020

|

0.64%

|

0.01%

|

0.48%

|

1.56%

|

|

August 2019

|

0.47%

|

0.01%

|

0.86%

|

0.26%

|

Source: TransUnion

Potential challenges on the horizon

While serious delinquency rates continued to decline in August, TransUnion observed some negative movement in 30-day delinquency rates.

Analysts explained this metric — which may serve as an early indication that an account will default and potentially be charged off — increased slightly in August for the two largest payments consumers often have to make: their vehicle and mortgage payments.

“This uptick for both products could signify that consumers are starting to roll forward on deferred payments as they come off of hardship programs,” Komos said.

“However, it’s still much too early to tell. It could simply be a missed or delayed payment that is late by a few days or weeks, though the consumer’s intention is still to make the payment,” he added.

Komos mentioned that close attention is being paid to delinquency levels as TransUnion’s latest Financial Hardship Survey from the week of Aug. 24 found that COVID-19 continues to financially impact consumers.

While TransUnion discovered the percentage of financially impacted Americans dipped to 52% — the lowest level since the ongoing survey series began in March — the concern among impacted consumers regarding their ability to pay bills and other obligations remains high (75%).

According to the survey, TransUnion reported that about one-third of impacted consumers are turning to savings to pay bills or loans and 13% cited they plan to open new credit cards. Despite these concerns, data from the monthly snapshot found that consumers are continuing to make payments as the average credit card balance per consumer dropped to $5,127 in August, compared to $5,686 the previous year.

In addition, TransUnion noted the average Aggregate Excess Payment (AEP) — defined as the average amount consumers are paying over their respective minimum payments — increased to $330 in August. Although analysts acknowledged that average is similar to what they observed at the same time last year when it came in at $300.

“Many consumers have continued to make payments even when enrolled in financial accommodation plans,” Komos said.

“The real litmus test in regards to consumer credit health will become apparent in the coming months when these safeguards begin to expire and consumers have less payment flexibility,” Komos went on to say.

TransUnion’s August Monthly Industry Snapshot features insights on consumer credit trends around personal loans, auto financing, credit cards and mortgage loans.

Additional resources for consumers looking to protect their credit during the COVID-19 pandemic can be found at transunion.com/covid-19.

S&P Global Ratings reported on Tuesday that contract extensions connected with public auto loan asset-backed securities (ABS) improved at an accelerated rate in July relative to June, representing the third consecutive month of declines.

The firm also noted the rates at which contract holders made a full payment after their extension expired.

Analysts discovered these trends based on loan-level data filed with the Securities and Exchange Commission.

Across the 17 prime shelves tracked by S&P Global Ratings, analysts indicated that extensions dropped 38% to 0.86% from 1.39% in June.

For the four subprime shelves in its analysis, the firm determined extensions decreased 31% to 5.29% from 7.66% in June.

Nonetheless, S&P Global Ratings said that extensions remained above pre-COVID-19 levels, at about 2.2 times January’s prime level and 2.6 times January’s subprime levels.

“These abnormally high deferrals are distorting traditional performance metrics, causing losses and delinquencies to be lower than otherwise,” analysts said in a news release, “and some securitizers think performance will not normalize until the fourth quarter of this year or first quarter of next year.”

S&P Global Ratings touched on what it believes to be three other key observations from the latest data, including:

• Of the extended loans from March to July, 82% and 64% in the prime and subprime sectors, respectively, have come out of extension status and remain outstanding.

• The vast majority of these loans continue to perform and remain current. However, analysts observed an uptick in 60-day delinquencies in July relative to June for these previously extended contracts.

• Of those prime and subprime contracts that have come out of extension status, 68% of the prime loans and 60% of the subprime contracts made a full payment in July.

Edmunds shared data with SubPrime Auto Finance News that average down payments in August climbed by more than $400 on new-car deals and by nearly $700 on used-vehicle transactions.

Experts and surveys both pointed to how previous federal government stimulus efforts helped consumers spend on big-ticket items like a vehicle. But the prospect for more capital injections directly to consumers took a significant hit this week as Comerica Bank chief economist Robert Dye projected when he said in the institution’s September economic outlook, “We may already be at the point where meaningful fiscal policy may be out of reach due to the rancorous political environment.”

What some lawmakers dubbed a “skinny” assistance package failed to generate enough approval votes on Thursday in the U.S. Senate to move forward, drawing a stinging reaction from Majority Leader Mitch McConnell who went on Twitter to say: “Every Senate Democrat just voted against hundreds of billions of dollars of COVID-19 relief. They blocked money for schools, testing, vaccines, unemployment insurance, and the Paycheck Protection Program.

“Their goal is clear: No help for American families before the election,” McConnell tweeted.

Had federal lawmakers been able to reach an agreement, the financial assistance to consumers could have helped vehicle sales. As mentioned previously, Edmunds told SubPrime Auto Finance News that the average down payment for a used vehicle financed in August came in at $3,353, up from $2,655 a year earlier. On the new-model side, the average down payment rose from $4,052 to $4,458

“For auto sales, particularly for used, any type of stimulus, whether it’s what we’ve seen since the pandemic or any type of tax refund, seems to gives sales wind behind them,” Edmunds executive director of insights Jessica Caldwell said in a phone conversation.

“I think whenever there is some sort of crisis, people are shocked,” Caldwell added later in the conversation. “The flip side of these situations is some people believe it’s the perfect time to make a big purchase because of the depressed market. We certainly saw that in April and May when automakers were offering those blockbuster deals like 0 percent for 84 months. I think with rates continuing to be relatively low, I still think people think it’s a good time to buy a car because they can take advantage of the rates.

“I think it’s interesting how these crises turn into buying opportunities for people who feel good about their own financial situation. We definitely do people see looking for a deal on the used-car side,” she went on to say.

Edmunds reported that the average interest rate on used-vehicle financing originated in August softened slightly to 7.92% from the year-ago reading of 8.50%. The average amount financed moved a bit higher to $23,081 from $22,252.

Along with finance companies taking on risk, Dye described the potential economic peril that might be ahead, especially as federal lawmakers bicker.

“A stricter approach to unemployment benefits, in the face of a massive new wave of unemployment, would have a chilling effect on the economy,” Dye said. “In such a case, we would expect that consumer spending would be reined in for lower-income households and for households with unemployed workers. Consumer confidence would fall as unemployment increased. The loss of purchasing power and loss of confidence would hamstring the consumer economy.

“A condition of extended demand destruction and curtailment would contribute to a huge capacity overhang for many businesses. Thus, the effects of the consumer squeeze would eventually be felt upstream in many heavy industries that are not directly linked to consumer spending. State and local tax collections would be further constrained, requiring deep cuts in government spending. Truly, the potential for a double-dip recession of historic magnitude is sobering,” he went on to say.

Edmunds' in-depth auto financing data can be found below:

New-Vehicle Data

|

Year

|

Term

|

Monthly Payment

|

Amount Financed

|

APR

|

Down Payment

|

|

2015

|

68.2

|

$487

|

$29,184

|

4.2

|

$3,257

|

|

2019

|

69.5

|

$555

|

$32,590

|

5.7

|

$4,052

|

|

2020

|

70.3

|

$570

|

$34,770

|

4.7

|

$4,458

|

Used-Vehicle Data

|

Year

|

Term

|

Monthly Payment

|

Amount Financed

|

APR

|

Down Payment

|

|

2015

|

66.3

|

$372

|

$20,383

|

7.66

|

$2,193

|

|

2019

|

67.4

|

$412

|

$22,252

|

8.50

|

$2,655

|

|

2020

|

67.6

|

$418

|

$23,081

|

7.92

|

$3,353

|

Source: Edmunds