Focused on what auto finance underwriters might see daily, the Consumer Financial Protection Bureau (CFPB) released a report this week examining trends in credit reporting of debt in collections from 2018 to 2022.

While focused on other parts of the credit market, the report showed the total number of collections tradelines on credit reports declined by 33%, from 261 million tradelines in 2018 to 175 million tradelines in 2022.

The CFPB said the share of consumers with a collection tradeline on their credit report decreased by 20% in the same timeframe.

The bureau reiterated collections tradelines are furnished to credit reporting companies by third-party debt collectors. Commonly reported collection items include medical, rental and leasing, credit card, and utility accounts.

Officials noted some third-party collectors work on behalf of original creditors for a fee (contingency-fee-based debt collectors) and others purchase accounts outright from creditors (debt buyers).

Unlike most other tradelines, the CFPB said debt collection tradelines “rarely report positive information” such as on-time payments, resulting in reporting of collections tradelines being “almost entirely harmful to consumers.”

The bureau pointed out collections tradelines are visible to potential finance companies, lenders, employers, landlords, and others who run credit inquiries or background checks.

“Collections tradelines can limit people’s access to jobs and housing, as well as decrease credit scores and increase the cost of credit. Given the potential damaging impacts of collections tradelines, reporting of inaccurate data is especially harmful,” the CFPB said in a news release.

The report is drawn from the CFPB’s Consumer Credit Panel, a nationally representative sample of approximately 5 million de-identified credit records maintained by one of the three nationwide credit reporting companies.

“Our analysis of credit reports provides yet another indicator that, due to a strong labor market and emergency programs during the pandemic, household financial distress reduced over the last two years,” CFPB director Rohit Chopra said in the news release. “However, false and inaccurate medical debt on credit reports continues to be a drag on household financial health.”

The entire report can be downloaded via this website.

While still on the watch for “cutting corners to fuel their profit model,” the Consumer Financial Protection Bureau (CFPB) recently released its annual report that details improvements made by the three largest credit bureaus — Equifax, Experian and TransUnion.

The Fair Credit Reporting Act requires the CFPB to submit an annual report about complaints submitted by consumers regarding the nationwide consumer reporting companies. Officials said the report is based on the 488,000 consumer complaints the CFPB transmitted to Equifax, Experian, and TransUnion from October 2021 through September 2022.

The CFPB said through a news release that the findings follow last year’s report that detailed “failures” by the nationwide companies when responding to consumer complaints submitted to the CFPB.

The bureau indicated Equifax, Experian, and TransUnion have remedied some of the issues identified in last year’s report.

Specifically, the CFPB found Equifax, Experian, and TransUnion have:

—Changed how they respond to complaints: Equifax, Experian, and TransUnion use of problematic response types described in last year’s report has declined. Most complaints now receive more substantive responses.

—Provided more tailored complaint responses: Across all three companies, most responses now describe the outcomes of consumers’ complaints. In September 2022, the nationwide companies provided a tailored response to more than 50% of complaints that were closed with an explanation or relief.

—Reported greater rates of relief in response to complaints: In 2022, TransUnion reported providing relief in most complaints. Experian reported providing relief in nearly half of complaints. Equifax reported that it did not provide relief, but its written complaint responses suggest that its rates of relief are comparable to the other two companies.

The CFPB also highlighted other consumer reporting problems and reminded consumer reporting companies of their obligations to consumers under the Fair Credit Reporting Act.

For example, officials pointed out an earlier report revealed how the nationwide consumer reporting companies had often allowed their processes to be used to “coerce individuals to pay medical bills they may not even owe.”

The CFPB said it also issued straightforward guidance on permissible purposes for accessing consumer reports, identifying and eliminating obviously false and junk data, and resolving consumer disputes.

Additionally, the CFPB reiterated that it has taken action against consumer reporting companies when they have broken the law, as well as affirmed the ability of states to police credit reporting markets.

The CFPB now is expecting Equifax, Experian and TransUnion to continue improving how they serve consumers, recommending that:

—Consider consumer burden when implementing automated processes: When companies consider introducing automated processes that will affect their customers, particularly those that relate to a legal right, the CFPB said they should consider consumer burden, especially whether a change will require consumers to do more work to exercise their legal rights.

—Recognize that technology is also improving for consumers: Advances in communications technologies mean consumers do not necessarily need to write complaints on their own. Instead, the CFPB said communications technologies may ease the writing burden. Such innovations, including ones that can generate letters for consumers, may create similar-sounding complaints that are, in fact, from unique individuals with independent concerns. The assumption that similar-sounding letters are from third parties will increasingly be wrong.

—Consider how to transition the market from control and surveillance to consumer participation: The bureau noted one potential reason there are so many reported inaccuracies in consumer reporting data is that consumers are several degrees removed from their own data. Enabling increased consumer participation on the data side of consumer reporting has the potential to create a fairer market with added benefits for consumers, consumer reporting companies, and lenders.

Along with noting those improvements and sharing recommendations, CFPB director Rohit Chopra said in the news release, “TransUnion, Equifax, and Experian routinely top the list of complaints submitted by consumers.

“We will be exploring new rules to ensure that they are following the law, rather than cutting corners to fuel their profit model,” Chopra went on to say.

The entire report examining Equifax, Experian, and TransUnion can be downloaded via this website.

The Consumer Financial Protection Bureau started the year by launching an initiative in connection with what the federal regulator called “exploitative junk fees.”

Last week, the CFPB turned its attention to what it’s calling “junk data.”

The bureau issued guidance to consumer reporting companies about their obligation to screen for and eliminate obviously false “junk data” from consumers’ credit reports. The CFPB said companies need to take steps to “reliably detect and remove inconsistent or impossible information from consumers’ credit profiles.”

For example, officials said many children in foster care have large amounts of information on their credit reports that is “clearly” junk data because as minors they are prohibited from entering into most contracts for credit.

While incorrect data affects millions of Americans, the CFPB believes that children in foster care may be particularly susceptible to these problems because of a high rate of identity theft impacting that population.

The regulator explained roughly 400,000 children in the United States foster care system often lack permanent addresses, and their personal information is frequently shared among numerous adults and agency databases.

“When bad actors take advantage of children passing through their care and use their personal information to take out loans, children in foster care may enter adulthood saddled with negative and clearly inaccurate credit histories that can hinder their progress toward financial independence,” the CFPB said in a news release.

“When consumer reporting companies include inconsistent or conflicting account information or information that does not make sense or cannot be true, consumers can suffer real-world consequences,” the bureau continued.

The CFPB pointed out that junk data in reports can lead to consumers being denied credit, housing, or employment, or paying more for credit. The bureau acknowledged junk data can take many forms, but some examples are credit reports that reflect a child having a mortgage, or a credit report that reflects a debt incurred years before the person’s birth.

The regulator reiterated that consumer reporting companies have a legal requirement to follow reasonable procedures to assure maximum possible accuracy of information that they collect and report. As part of that requirement, companies must have policies and procedures to screen for and eliminate junk data.

Specifically, the CFPB said the policies and procedures should be able to detect and remove:

—Inconsistent account information: Sometimes consumer reports can show two or more pieces of information that cannot all be true. For example, an account is paid in full but still shows a balance, or a date of first delinquency predates the account’s opening.

—Information that cannot be accurate: Sometimes information on consumer reports reflects obvious impossibilities. For example, if a tradeline includes a date that predates the consumer’s date of birth or if just one of many tradelines indicates a consumer is deceased.

The bureau said a consumer reporting company’s policies, procedures, and internal controls should further identify and prevent reporting of illegitimate credit transactions for a minor.

Officials added that minors generally cannot legally enter into contracts for credit except in certain limited circumstances, including applications for student loans, for emancipated minors, or as credit card authorized users.

“When a credit report accuses someone of defaulting on a loan before they were born, this is nonsensical, junk data that should have never shown up in the first place,” CFPB director Rohit Chopra said in the news release. “Consumer reporting companies have a clear obligation to use better procedures to screen for and eliminate conflicting information, or information that cannot be true.”

The entire advisory opinion can be found via this website.

There now is another way to attach soft-pull credit capabilities onto your dealership website.

Automotive digital marketing provider Sincro, an Ansira company, announced last week that it has designated CreditMiner as a preferred partner within its website platform.

According to a news release, the preferred partnership with CreditMiner provides Sincro website customers with access to the Sincro Credit Impact system (SCI), an integration that can enables a customer-facing soft credit pull solution directly within the website experience.

The companies said this activity garners the highest engagement on a dealer’s website.

“The Sincro Credit Impact System is an example of the robust third-party partnerships that can be seamlessly activated within the Sincro website platform,” Sincro senior vice president of product strategy Jason Jewert said in the news release.

“The API integration enables real-time pre-approvals through the simple inputs of name, physical and email address, and phone number,” Jewert continued. “This information combined with the rich reporting capabilities of the website platform provide dealers with all the information needed to drive last-mile conversion.”

Ken Luna is CreditMiner’s vice president of strategic partnerships and explained what soft credit pulls can do for a dealership’s potential sales and financing activities.

“We view the information flow from this process as a super lead,” Luna said. “The consumer knows instantly what they are pre-approved for, and also receives an email with the same information. The firm offer of credit shows an offer based on which credit tier the consumer’s FICO score shows them residing in, as well as whether the vehicle of interest is new, used, or CPO, not a vanilla canned response. The vehicle the consumer is interested in also shows based on where they were on the website when they initiated the get preapproved function.

“The dealership receives all of the information above, integrated into their CRM system, plus they also can see the prospect’s FICO auto score, all the trade lines, and other valuable information derived from the soft credit pull,” Luna continued.

“They can also see the Synthetic Fraud Score of the prospect if they choose that option. Having this information helps steer the prospect to the right vehicle even if the one they like is not feasible.”

Ken Hill, managing director of 700 Credit, acknowledged during this episode of the Auto Remarketing Podcast that he’s a “credit geek.”

While that might sound like a negative moniker, Hill offered his expertise on the impact that dealers are facing because of the enhancement of the Safeguards Rule by the Federal Trade Commission as well as the capabilities that soft credit pulls have to enhance the opportunities for dealerships and finance companies.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

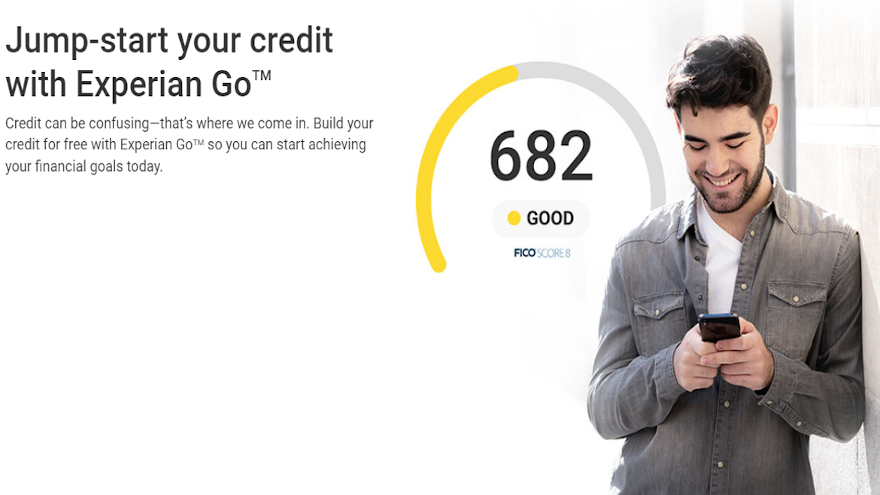

Another initiative to help finance companies cater to consumers with little or no credit backgrounds recently surfaced; this time from Experian.

In what the company said is meant to further financial inclusion across the United States, Experian launched what it dubbed Experian Go, a free program to help “credit invisibles,” or people with no credit history, begin building credit “on their own terms.”

The company explained through a news release that Experian Go is the only program currently available that can help consumers establish their financial identity by creating an Experian credit report.

According to Experian, nearly 50 million consumers have a nonexistent or limited credit history. Without an existing credit report, Experian said finance companies can’t verify a consumer’s identity and consumers are unable to access credit at fair and affordable rates.

“Often, these consumers are caught in cycles of predatory lending; can’t cover emergency expenses; and face limited housing options, higher insurance premiums and interest rates, employment challenges, larger deposit requirements and more,” Experian said.

The company indicated that Experian Go, which began piloting in October, has already helped more than 15,000 credit invisible consumers establish an Experian credit report and become visible to potential finance companies and other lenders.

By helping consumers establish a financial identity through Experian Go, Experian aims to help consumers build the foundation for future financial opportunities.

“Living with a nonexistent or limited credit history can be a significant barrier to financial opportunity in America,” said Craig Boundy, chief executive officer of Experian North America. “We believe every individual deserves the opportunity to reach their fullest financial potential and we’re proud to be the only credit bureau with a program to help credit invisibles build their credit history in minutes.

“Innovations like Experian Boost and Experian Go help to ensure people can access the credit they need when they need it. This new program is a direct reflection of our mission to bring financial power to all,” Boundy continued in the news release.

As Boundy referenced, the launch of Experian Go is a continuation of Experian’s mission to help consumers everywhere get access to fair and affordable credit.

Within minutes, the company said credit invisibles can have an authenticated Experian credit report, tradelines and a credit history by using Experian Boost and instant access to financial offers through Experian Go.

Experian noted that this program can help consumers build credit and become scoreable without going into debt. In fact, Experian said its early analysis shows 91% of consumers with no credit history who connect to Experian Boost, a free feature that allows users to contribute their on-time cell phone, video streaming service, internet, and utility payments directly to their Experian credit report, can become scoreable in minutes with an average starting near-prime FICO Score of 665.

Once a consumer downloads Experian’s free mobile app and enrolls in a free Experian membership, they’ll be asked to authenticate their identity using a government-issued ID, Social Security Number and a “selfie.”

From there, personalized recommendations are available to help users add accounts, also known as tradelines, to their Experian credit report.

Users may receive information about becoming an authorized user or be invited to apply for a credit card designed specifically for those new to credit. Others may contribute their on-time bill payments directly to their Experian credit report with Experian Boost, a feature that’s helped nearly 9 million consumers instantly improve their FICO Score.

Since launching in 2019, the company said Experian Boost has helped more than 10,000 previously unscorable consumers receive a FICO Score each month and added more than 78 million points to FICO Scores nationwide.

According to other Experian research, 28 million consumers are credit invisible and an additional 21 million consumers have “unscorable” credit files, meaning they have what’s considered a thin credit file or limited credit history.

Experian acknowledged the problem more frequently impacts communities of color. In fact, a recent Experian survey revealed one in five Black consumers and one-third of Hispanic consumers don’t have any credit in their name, with 65% of Black consumers and 51% of Hispanic consumers unsure of the steps to take to establish or improve their credit.

“We recognize the correlation between credit scores and opportunity in America and view credit worthiness — or the lack thereof — as a barrier to financial mobility and success,” Operation Hope chief executive officer and founder John Hope Bryant said in the news release.

“We are thankful for our partnership with Experian and stand with them as we work together to amplify an actionable plan that increases financial access to all,” Hope Bryant went on to say.

To learn more about Experian Go, visit www.experian.com/go.

Scores of consumers now are leveraging Buy Now, Pay Later (BNPL) offerings by some retailers.

To help auto finance companies evaluate applicants who might have BNPL commitments during the underwriting process, Equifax recently announced that the company is furthering its commitment to expand access to credit by making BNPL payment information part of credit reports, as identified by a new business industry code.

According to a news release, Equifax said it has created what it believes is the industry’s first policy for acceptance of BNPL tradelines in consumer credit files via Consumer Data Industry Association (CDIA) Metro 2 guidelines.

An Equifax study of anonymized consumer data from a BNPL provider showed that individuals who pay their BNPL loans on time could potentially increase their FICO score — helping consumers to both build and rebuild credit.

“Equifax will be the first credit reporting agency to formalize a standard process for reporting BNPL tradelines for inclusion on traditional consumer credit reports,” said Mark Luber, chief product officer for U.S. Information Solutions (USIS) at Equifax.

“We are committed to helping people live their financial best, and recognize the role that BNPL services can play in helping people build stronger financial profiles,” Luber continued in a news release.

Equifax pointed out that BNPL products — also known as point-of-sale financing — are a growing way for consumers to access convenient, alternative financing options for online or in-store purchases. They typically involve short-term, interest-free installment payments offered at checkout.

Beginning in the first quarter, Equifax will implement a new “business industry code” for BNPL. Equifax explained this is a standard identifier used to classify the industry in which each Equifax customer functions.

The new industry code will classify BNPL tradelines, including payment history and give Equifax customers and scoring partners the ability to view and decide how to incorporate the information into their decisioning to potentially open up new mainstream financial services opportunities to more consumers.

Equifax mentioned that its research also indicated that the inclusion of on-time payments of BNPL loans in credit reporting may increase credit scores. Equifax conducted a study of anonymized consumer BNPL data, where the BNPL tradelines had the following features:

— Reported as revolving line of credit accounts

— Had, on average, five and-a-half months of repayment history reported

— Had an average utilization of 17.9% (including consumers who paid off their BNPL tradeline)

The Equifax study also shows the potential for consumers who pay their BNPL loans on-time to improve their FICO score, specifically:

— The majority of consumers in the study were helped by having an on-time BNPL tradeline in their credit file, with an average FICO score increase of 13 points.

— BNPL can be a powerful way for new-to-credit consumers to build their credit profiles. The study showed that individuals with either a “thin” credit file consisting of two or less tradelines or a “young” credit file — where all credit history is no more than 24 months old — saw an average FICO Score increase of 21 points with the addition of on-time BNPL tradelines to their credit file.

— BNPL can also help consumers rebuild their credit. Consumers who had significantly late payments reported on their traditional credit file experienced an average FICO Score increase of 13 points with the addition of on-time BNPL tradelines to their credit file.

“Most BNPL providers either bypass the credit check completely, or do a soft pull on credit files, which can be attractive to consumers,” Luber said.

“We are encouraging BNPL providers to report into Equifax as a powerful source of data,” he continued. “Those who use BNPL services that report can demonstrate reliable behavior and boost their credit profile.”

Responding in part to consumer demand for as much information as possible before finalizing their vehicle financing, 700 Credit announced a product alliance with fusionZONE Automotive’s digital retailing solution, FastLane Leads.

FastLane Leads is designed to simplify the digital retail process and reduce form abandonment rates through its straightforward four-step process. Dealers can receive more qualified leads and the consumer is provided a more robust pricing offer.

The companies explained the alliance allows fusionZONE to integrate the 700Credit QuickQualify soft-pull platform within FastLane Leads so consumers can receive accurate interest rates and payment quotes before they enter the finance office.

The firms added dealers can receive the FICO score and full credit file without placing a hard inquiry on the consumer’s credit file.

“Accuracy in the monthly payment quotes provided to the consumer by the FastLane Leads tool is critical to dealers completing the sale and removing friction in the finance office,” said Ken Hill, managing director of 700Credit, which is a provider of credit reports, compliance solutions and soft-pull products.

“Empowering dealerships to gain valuable insight into their customers' credit profile while enabling customers to know their interest rate and monthly payments they qualify for earlier in the sales process is a win-win for the dealership and the consumer,” Hill continued in a news release.

Alex Papadopulos, fusionZONE Automotive’s chief operating office and product designer added, “fusionZONE is excited to partner with 700Credit to bring its QuickQualify soft-pull platform to our new FastLane Leads tool.

“By pairing our lightweight, four-step digital retailing solution with accurate monthly payment quotes, we’re empowering the consumer and enhancing the dealer’s ability to attract qualified leads online,” Papadopulos went on to say.

For more information on the partnership, contact customer service at (866) 273-3848.

This week, 700Credit finalized another integration partnership to make available its credit reports as well as compliance and soft-pull solutions.

The latest relationship is with DriveCentric, a robust CRM, artificial intelligence (AI) and conversational engagement platform for automotive retailers. Officials from 700Credit said this new integration can provide dealerships with seamless access to its credit report and compliance platforms that can optimize the sales process.

DriveCentric has also integrated 700Credit’s prescreen solution that can provide dealers visibility to a consumer’s FICO score and current auto-finance information at the start of the sales process.

“The DriveCentric CRM has a strong following in the automotive industry. We are very thrilled to have DriveCentric as a partner and welcome their customer base to our 700Credit family,” 700Credit managing director Ken Hill said in a news release.

“The multiple integration points of our credit, compliance and prescreen solutions will maximize efficiencies for dealerships and expedite the purchase process, as well as help them sell more vehicles,” Hill continued. “Prescreen information enables dealers to make an accurate monthly payment at the beginning of the sales process.”

DriveCentric chief executive officer David Fultz added, “As we continue to innovate and look for ways to improve and streamline our dealership software, 700Credit was an easy choice for integration.

“For dealerships that use DriveCentric and 700Credit, this partnership will significantly impact the sales cycle by providing faster, more accurate quotes and reducing the time it takes to deliver a vehicle,” Fultz went on to say.

For more information about 700Credit, visit www.700credit.com.