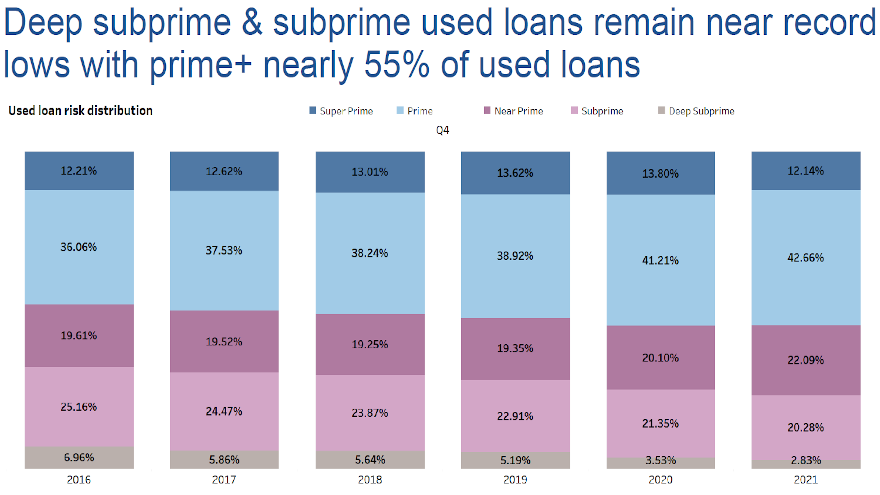

To use the industry vernacular, Experian’s newest State of the Automotive Finance Market report reinforced how much more money is on the street nowadays.

According to Experian’s fourth-quarter report released on Thursday, the average amount financed and monthly payments both jumped significantly year-over-year for both used- and new-vehicle financing.

Read more

If an individual with a less than prime credit background still somehow secured financing for a new vehicle in January, there’s a notable possibility that the installment contract will be underwater for some time, based on record-breaking data Edmunds shared on Tuesday.

Edmunds said more consumers than ever are paying above sticker price for a new car amid inventory shortages and elevated consumer demand.

In fact, Edmunds reported that buyers paid above MSRP in a record 82.2% of all new-vehicle purchases last month, compared to 2.8% in January 2021 and 0.3% in January 2020.

Edmunds data also showed that the average transaction price for a new vehicle climbed to $728 above MSRP in January, compared to $2,152 below MSRP last January and $2,648 below MSRP in January 2020.

“The fact that an overwhelming majority of consumers are paying above sticker price would have been unthinkable even just a year ago,” Edmunds executive director of insights Jessica Caldwell said in a news release.

“This is in part driven by affluent consumers being willing to shell out more cash to get the vehicles that they want, but there’s also a vast population of individuals who are being forced to do so simply because they need transportation and have no other choice,” Caldwell continued.

Edmunds analysts took a look at the difference in new vehicle average transaction prices and compared them to the average MSRP across automakers to identify the brands commanding the largest amounts above sticker price and the brands yielding the greatest discounts.

Analysts discovered Cadillac topped the list of brands that commanded above-sticker price, with an average markup of $4,048 in January, followed by Land Rover, with an average markup of $2,565, and Kia, with an average markup of $2,289.

Edmunds noted that Alfa Romeo topped the list of brands that brought below-sticker price, with an average discount of $3,421 in January, followed by Volvo with an average discount of $869 and Lincoln with an average discount of $510.

“All eyes have been on Ford and GM since they both publicly called for their dealers to stop charging over MSRP for vehicles,” Caldwell said. “Of all automakers, they might be in the most precarious position since they have very high-profile launches in the near future that appeal to a new type of customer. But looking at the numbers, there are clearly some other automakers who might want to follow suit.”

“Savvy dealers, though, are conducting business during this wave of inflation in a way that’s mindful of the possible adverse reaction of their customers,” she added.

Edmunds’ experts said that holding off on a new-vehicle purchase would be the most pragmatic move for consumers in this market, but they also note that this course of action might be unrealistic for some individuals given that prices aren’t expected to normalize for quite some time.

“Consumers might be waiting up to a year or longer if they want to hold off until the market resembles anything close to the pre-pandemic normal, but some buyers simply cannot wait,” Edmunds senior manager of insights Ivan Drury said in the news release.

“If you know you need a new vehicle soon — or if you have a vehicle coming off lease and its term can’t be extended — doing extra research is critical to get an advantage, and using the list set forth below is a decent starting point if you’re looking out for price discrepancies among different brands,” Drury went on to say.

MSRP vs ATP by Vehicle Make

January 2022

|

Make

|

MSRP

|

ATP

|

Difference

|

|

Cadillac

|

$76,914

|

$80,962

|

$4,048

|

|

Land Rover

|

$87,457

|

$90,022

|

$2,565

|

|

Kia

|

$32,218

|

$34,507

|

$2,289

|

|

Porsche

|

$103,590

|

$105,311

|

$1,721

|

|

Acura

|

$49,316

|

$51,017

|

$1,701

|

|

Genesis

|

$59,933

|

$61,536

|

$1,603

|

|

Honda

|

$32,440

|

$33,948

|

$1,508

|

|

Hyundai

|

$33,545

|

$35,043

|

$1,498

|

|

Audi

|

$60,965

|

$62,290

|

$1,325

|

|

Jaguar

|

$66,828

|

$67,937

|

$1,109

|

|

Toyota

|

$37,174

|

$38,189

|

$1,015

|

|

Nissan

|

$32,529

|

$33,433

|

$904

|

|

Infiniti

|

$53,709

|

$54,529

|

$820

|

|

Dodge

|

$48,498

|

$49,227

|

$729

|

|

Mercedes-Benz

|

$67,817

|

$68,536

|

$719

|

|

Fiat

|

$29,818

|

$30,536

|

$718

|

|

GMC

|

$58,749

|

$59,426

|

$677

|

|

Chevrolet

|

$47,728

|

$48,353

|

$625

|

|

Subaru

|

$34,164

|

$34,756

|

$592

|

|

Chrysler

|

$47,779

|

$48,239

|

$460

|

|

Volkswagen

|

$35,046

|

$35,474

|

$428

|

|

Jeep

|

$49,220

|

$49,573

|

$353

|

|

Mazda

|

$32,785

|

$33,097

|

$312

|

|

Lexus

|

$53,490

|

$53,725

|

$235

|

|

Mitsubishi

|

$29,309

|

$29,516

|

$207

|

|

Ford

|

$49,680

|

$49,843

|

$163

|

|

Buick

|

$41,716

|

$41,733

|

$17

|

|

Mini

|

$36,440

|

$36,289

|

-$151

|

|

BMW

|

$63,209

|

$63,010

|

-$199

|

|

Ram

|

$60,057

|

$59,592

|

-$465

|

|

Lincoln

|

$62,202

|

$61,692

|

-$510

|

|

Volvo

|

$57,870

|

$57,001

|

-$869

|

|

Alfa Romeo

|

$54,644

|

$51,223

|

-$3,421

|

|

Industry Average

|

$44,989

|

$45,717

|

$728

|

Source: Edmunds

As one subsidiary of Westlake Technology Holdings posted records in the vehicle leasing space last year, another of its subsidiaries that specializes in shared cash flow auto lending generated new company records in 2021, too.

According to a news release, Western Funding compiled record growth in portfolio payouts, loan portfolio, loans originated and producing dealers for 2021.

Those new high-performance metrics include:

— $3.5 million in portfolio payouts to over 200 participating dealers

— 100% adoption of e-contracting

— 52% year-over-year growth in its loan portfolio

— 49% year-over-year growth in loans originated

— 47% year-over-year growth in producing dealers

“These successes are a testament to Western Funding’s focus on improving its programs, reducing funding time, and making the loan origination experience better for all participating dealers,” Westlake Technology Holdings group president Ian Anderson said in the news release. “We are looking forward to 2022 and anticipate another impactful year of growth for WFI.”

Additionally, Western Funding explained how it adopted a set of values designed to solidify a culture critical to meeting long-term business objectives. The values, referred to by the acronym FASTER, are:

Fun

Accountable

Strategic

Team-oriented

Efficient

Respectful

By implementing these values into its day-to-day operations, Western Funding said that it will continue to create value for participating dealers and consumers.

“I’m extremely proud of the entire Western Funding team,” Western Funding president Jim Murray said. “Building a solid culture is hard but our team recognizes that an investment in a strong culture will increase the likelihood of delivering the innovation needed to better serve our customers in the future.”

Western Funding said it expects continued growth in 2022 by continuing to improve its program, adding near- prime and prime credit segments and reaching out to new dealer segments.

The company added that it will also introduce a formal program this year designed to recognize and reward its top dealers.

For more information, visit www.westernfundinginc.com.

In his first appearance of the year on the Auto Remarketing Podcast, StoneEagle F&I senior vice president of business development Joe St. John acknowledged how enticing it would be to run a dealership again because of the F&I performances many stores enjoyed in 2021.

Along with his top three data points from last year, St. John also described how positive the landscape has been for F&I service providers, too.

To listen to the episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

Almost four months later, the journey of Santander Consumer USA shifting from a publicly traded company to a private firm still isn’t over the financial finish line.

The company announced last week that it has extended the expiration date of its previously announced tender offer to acquire all outstanding shares of common stock not already owned by Santander for $41.50 per share.

Under the terms of the merger agreement entered into on Aug. 23 by and among Santander Holdings USA (SHUSA), SCUSA and Max Merger Sub, a wholly owned subsidiary, the company said through a news release that tender offer will be followed by a second-step merger in which the purchaser will be merged with and into SCUSA, with SCUSA surviving as a wholly owned subsidiary of SHUSA, and all outstanding shares of common stock of SCUSA not tendered in the Tender Offer will be converted into the right to receive the offer price in cash.

The company said the tender offer started on Sept. 7 and as previously extended was scheduled to expire last Thursday.

As a result of this extension, the tender offer is now scheduled to expire this Thursday.

“The transaction is subject to customary closing conditions, including regulatory approval by the board of governors of the Federal Reserve System,” the company said. “The transaction is not subject to shareholder approval and is currently expected to close in the fourth quarter of 2021 upon receipt of regulatory approval.”

The company recapped that the board of directors of SCUSA formed a special committee consisting of the independent and disinterested directors of SCUSA to negotiate and evaluate a potential transaction with SHUSA.

The newest announcement also mentioned the board of directors of SCUSA, acting on the unanimous recommendation of the special committee, has unanimously determined to recommend the tender offer to SCUSA’s shareholders (other than SHUSA).

The board of directors of SHUSA has unanimously approved the transaction, according to the company.

J.P. Morgan Securities LLC is acting as financial advisor, and Wachtell, Lipton, Rosen & Katz is acting as legal counsel to SHUSA. Piper Sandler is acting as financial advisor, and Covington & Burling LLP is acting as legal counsel to the special committee. Hughes Hubbard & Reed LLP is acting as legal counsel to SCUSA.

Computershare Inc. and Computershare Trust Company, N.A., the joint depositary for the tender offer, have informed SHUSA that approximately 13.4 million shares of common stock of SCUSA have been tendered and not validly withdrawn in the tender offer as of last Thursday.

With so many help-wanted signs visible at businesses nowadays, DriveItAway wants to be a part of the transportation solution for both employers and workers — especially individuals with soft credit histories or without significant funds for a down payment.

On Wednesday, the mobility platform with its subscription-to-purchase technology for dealers, announced its newest program for employers to enable vehicle ownership as both a means and incentive for potential new employees to get to work.

DriveItAway explained the disconnect between where entry level jobs are and where the people who want and need them live has been observed in every area of the United States and has been documented in “Poverty of the Carless,” an academic study researched and written by David King from Arizona State University, Michael Smart from Rutgers University and Michael Manville of the University of California.

That study noted the ever-increasing poverty rate of those households without vehicles throughout the United States. Between 1960 and 2014, the U.S. poverty rate fell from 24% to 14%, but for households without vehicles, the poverty rate actually rose from 42% to 44%.

“Historically, the lack of private vehicle ownership has always been a major problem for entry level employees — jobs, particularly retail jobs — are one place, while good people who need them live a great distance away,” DriveItAway founder and chief executive officer John Possumato said in a news release. “While it is nice to think that public transportation or carpooling is available, the fact is, in many areas of the United States, it frequently isn’t a viable option, and the cost of car sharing or ride sharing is an unsustainable expense for many, leaving only private vehicle ownership as a practical alternative.

“If you can’t get to work, you can’t go to work, which creates both unemployment and poverty. Our program, focused on transportation, solves this problem as it enables credit challenged and first-time car owners a way to ‘pay as you go’ for immediate vehicle access,” Possumato continued.

DriveItAway reiterated that its “subscribe to own” app-driven vehicle acquisition platform is the only one of its kind to allow potential new hires, without credit or down payment in hand, to drive the car of their choice immediately, enabling ultimate ownership through a “pay as you go” basis.

With every rental payment, the company said the renter builds equity towards the vehicle down payment, if the renter decides to buy his/her vehicle.

Possumato highlighted that the program fits so well today, that some employers and contract labor organizations are choosing to subsidize the first few payments for new employees that sign on to work, “thought by many to be a more positive and life changing incentive than a one-time bonus payment or other financial inducements now offered.”

Possumato also pointed out that any company, large or small, can implement a program that enables new workers to get to work, and at the same time help eliminate the “poverty of the carless” in their neighborhoods with the DriveItAway vehicle “pay as you go” ownership enablement program.

For more information, send a message to [email protected] or call (856) 577-2763.

Experian’s latest report highlighted additional data about the used-vehicle finance market, showing the amount financed for consumers to take delivery of a used model during the third quarter 20% year-over-year.

During this episode of the Auto Remarketing Podcast, Experian senior director of automotive financial solutions Melinda Zabritski expanded on what other interesting tidbits she and her colleagues discovered.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

More evidence of how rising wholesale and retail prices are landing within finance company portfolios arrived on Thursday.

According to Experian’s latest State of the Automotive Finance Market report, the average amount financed for a used vehicle jumped more than 20% year-over-year during the third quarter.

Read more

Westlake Financial Services is continuing to diversify its portfolio but leveraging a lending strategy that’s gained industry traction this year.

Along with originating indirect auto financing, this week Westlake launched what it’s calling, Cash Now Pay Later. The company said this new product available through its LoanCenter division can provide financial flexibility to its customers by enabling them to borrow cash today and pay it back at a later date.

According to a news release, Cash Now Pay Later is currently being piloted by Westlake to its more than 1 million existing customers and has resulted in a high demand for the program since the launch.

“Westlake recognized a need to provide its established customers with a simple online solution to get cash now,” LoanCenter vice president Jim Eyraud said in the news release.

“Pre-approved offers for financing can be redeemed by existing Westlake customers through a fully automated online process on the MyAccount mobile app,” Eyraud added. “This quick and easy process helps to offer consumers the financial flexibility support they need.”

Westlake said it plans to expand Cash Now Pay Later nationwide through LoanCenter.com during the fourth quarter.

Under the expanded program, customers will be able to personalize their Cash Now Pay Later structure and select amounts between $500 and $5,000. After e-signing, money is deposited into the customers bank account within a couple of hours.

“The goal of LoanCenter.com is to provide lending solutions to help borrowers through any financial situation. The Cash Now Pay Later program is a great compliment to the current auto and secured loan offerings on LoanCenter,” said David Goff, vice president of marketing at Westlake.

To learn more about LoanCenter, visit www.loancenter.com.

StoneEagle F&I senior vice president of business development Joe St. John made his monthly appearance on the Auto Remarketing Podcast to discuss what’s happening in dealership finance offices.

Senior editor Nick Zulovich asked about which elements helping F&I departments this year could be sustained and which ones might be unique to 2021.

To listen to the episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.