Even before COVID-19, auto-finance companies were on the on-ramp to change. An increased focus on the customer, new modes of engagement and preparation for a slowdown were driving digital transformation in their operations and offerings. COVID-19 will not throw this transition into reverse, but instead accelerate it.

Now, auto-finance companies must harness the digital and analytical capabilities they were already developing and put them to work in two new ways. First, to address the current crisis. And second, as part of a longer-term customer- and asset-focused strategy reset.

To achieve this, auto financiers will need to take five concrete steps, including:

1. Develop digital-first debt management capabilities

Auto collections volumes are on the rise. As customer income continues to fall, auto financiers will face an even higher volume of complex collections. And, due to social distancing measures and health issues, fewer collections agents will be available to manage the influx. The solution? Augmenting the human-driven approach to collections with automated and omni-channel customer engagement strategies.

Fortunately, the “stay at home” strategy for dealing with coronavirus has forced digital to become the standard and primary means of communication. Financiers should use this digital goodwill to improve their collections efforts. To manage increased workload from customer calls and delinquencies, which may be delayed due to payment deferrals and loan extensions, auto financiers will need to consider solutions like interactive voice messaging, backed by conversational artificial intelligence (AI) with integrated speech analytics.

What’s more, financiers that develop a quick, accurate, and sensitive digital collections experience will promote more collaborative interactions, increase their chances of being at the top of customers’ wallets, and prevent customers from taking their business to savvier providers.

For example, instead of all delinquent customers receiving a barrage of automated payment reminders, they should receive more pointed, personalized messaging and personally relevant restructuring plans. This type of intelligent targeting is enabled by a deeper understanding of both the organization’s changed debt servicing capacity and the customer’s preference of interactive channel.

A digital-first collections strategy has three further benefits for auto finance companies. First, by enabling them to engage customers early and empathetically, it will help them stay on the right side of consumer-protection bodies looking to ensure that consumers are treated fairly. Second, it will free up agents from more mundane calling activities so they can take on more targeted and nuanced customer interactions. And third, it will deliver huge cost savings to lenders and improve their ability to handle fluctuations in collections volumes, both now and in the future.

2. Enhance risk-based segmentation with data analytics

To emerge from this crisis with reputation and finances intact, auto lenders need to understand two things better: their customer and the macroeconomic conditions. Data — both internal and external — becomes very important in this respect. The world is upside-down: traditional internal data that helped indicate when to collect, how, and from whom, may still be useful — but financiers need to capture and act upon it with more immediacy. Similarly, external data assumes a more significant role in helping to identify new sources of risk. As a result, financiers must now use advanced data analytics to:

• Capture new data: In light of the crisis, new external data sources (such as customer zip codes, geo-economic data, and event-based triggers from credit risk bureaus) have suddenly become more important than traditional, internal, historical payment-cycle data. Finding innovative ways to capture this data will enable auto financiers to conduct what-if scenario modelling as the situation evolves.

• Regularly revise data sources: Data sources must be routinely updated. For example, credit scores captured at the time of auto-loan origination could be a couple of years old and may no longer be a true indicator of a customer’s current credit worthiness. Likewise, data that is useful now may not be in a few months’ time.

• Use synthetic data and theoretical models: Because this is a completely new scenario, auto financiers will have to feed and train models with synthetic or proxy data, or build new theoretical models to help them understand, explain, and predict credit risk and devise appropriate customer segmentation and treatment strategies.

3. Improve customer retention

If auto financiers do not make changes to their offerings and operations, they will not only see a rapid increase in delinquencies, but also a loss of customers.

To improve customer retention, they will need to reshape a range of finance options. For example, some financiers are giving new borrowers the option to defer their first payment by 90 days or existing customers the ability to defer payment for up to 120 days without any late fee.

But it doesn’t end there. Auto financiers need to use predictive analytics to proactively identify and support customers with latent risk of delinquency. This means targeting ‘at risk’ customers early and often with personalized, flexible offers, such as restructured loans, trade-ins, and extended terms. For example, Hyundai and Genesis are offering up to six months of payment relief for owners who lose their jobs.

Financiers will also need to use deep data analytics and build and use digital channels to present these new finance options to customers– for example, a self-service portal that allows customers to rework their terms based on their financial situations and choose their own path to resolution.

4. Roll out new repossession and return strategies

No matter what auto financiers do, many customers will still not be in the position to meet their auto-loan repayments. And in some cases, the relief available will not be enough for them to hold onto their vehicles. Auto financiers will need to brace themselves for much higher rates of repossession and return. But this does not have to be painful.

Auto financiers can implement strategies that will help to reduce repossession in the first place. For example, in addition to developing agile resolution strategies, they can also digitally enable downgrades.

In the past, car-swaps were generally associated with customers looking to upgrade vehicles. Now, due to the financial hardships auto customers are facing, they will also be looking to swap their cars and downgrade in order to reduce their monthly payments. Auto lenders need to provide options to customers to swap vehicles based on their affordability. For example, financiers can roll out and promote affordability calculators to help customers downgrade to a less expensive car to reduce the need for repossession. While this may increase inventory of more expensive vehicles in the short- to mid-term, it will also drive customer retention and help maintain cash flow.

Even with these strategies, a high number of cars may still come back to the market quickly – whether through repossession or return – which will increase pressure on lease residual values, widening the gap between the realizable value of the car and the loan value. Therefore, lenders will need to build intelligent models, feed them with data (such as contact history and external payment history), and use deep data analytics to obtain insights on the asset value and the right time to repossess cars.

5. Remarket more efficiently

As more customers will be returning their cars, and financiers will be repossessing still more vehicles, inventories of used cars are likely to explode. To maximize profitability, these cars cannot sit in the parking lot indefinitely.

To reduce the time from return or repossession to resale, auto financiers can take four steps:

• Use touchless, self-serve inspection solutions: As social distancing remains in effect, customers will be reluctant to bring their vehicles into the dealer for end-of-lease inspections. And there may not be enough staff to perform this service in any case. Remote inspection capabilities will be crucial during, and directly after, the pandemic. And, in the long term, these capabilities will drive cost efficacy for the auto financier.

• Better predict residual values: Using predictive analytics, auto financiers can better predict residual values based on current market conditions.

• Restructure used-car loans: With a rise in hardships, demand for used cars will increase. Financiers need to shift their focus from term-wise management of loans to innovative ways of structuring loans so that customers can buy these used cars in the first place.

• Improve marketing platforms for second-hand vehicles: Existing marketing platforms for used vehicles can be time-consuming to use and opaque in their pricing, and they are not well-trusted by consumers.

By focusing on the whole remarketing journey and using digital and analytical technologies to make it seamless from end-to-end, auto companies can keep inventories of used cars moving, which will help maintain healthy portfolios despite low sales and high returns.

It’s time to hit the gas

People will always need mobility solutions, but the auto-finance industry won’t go back to where it was before. COVID-19 has radically changed its short-term outlook. And rapid action is required to control the immediate risks and ensure long-term success.

The digital and analytical solutions auto finance companies put in place today will serve them well during the pandemic by easing financial pressure on customers and reducing repossessed inventory. They will also enhance loyalty and maximize customer lifetime value, helping to usher in a new era of better customer and asset-focused finance.

The sector was already moving in this direction, but now it’s time to hit the gas.

Rohan de Souza is the global auto finance leader for Genpact. In his role he is responsible for the growth strategy across auto finance clients which encompasses developing disruptive transformation solutions spanning digital, data science and engineering, intelligent operations and the execution of these solutions to deliver business outcomes for the portfolio. Rohan brings extensive financial services expertise having spent over 20 years in the industry. He has deep domain experience across leasing & lending having held leadership positions in operations, business transformation / Lean Six Sigma, human resources and client management in his 19-year career with Genpact. Based in London since 2009 when he relocated from the U.S., he has experience delivering transformation for clients across Europe, North America, Australia & Asia.

The COVID-19 pandemic will undoubtedly have repercussions for consumers and lenders alike, as we are already starting to see. What isn’t evident yet is how things will look in another month, three months, six months and beyond. Have you identified the steps you should take now to help protect the future state?

In times of economic uncertainty, auto finance and other lenders must evaluate the current risk mitigation strategies they have in place and adjust them accordingly. Regardless of the reason for the economic downturn, these periods can be stressful for lenders and consumers alike. Failing to identify necessary adjustments and implement changes can have a catastrophic impact on even the most prudently managed portfolios.

Whether lenders take on this effort themselves or seek consulting expertise, re-evaluating and adjusting risk strategies shouldn’t be considered optional, neither should lenders adopt a “wait and see” approach while relying on the status quo. Now is the time to act in order to effectively monitor and mitigate potential exposure to fraud, update collection treatment strategies, and address the impact of potential delinquencies and bankruptcies. In addition to potentially minimizing exposure to fraud and risk, lenders have a real opportunity to help their customers by identifying those that may need special consideration.

Are automated risk scoring approaches adequate?

For most lenders, an automated risk scoring approach works well under steady state micro and macro-economic conditions. In dynamically changing environments that have a profound impact on consumers, a previously static strategy should be monitored and adjusted on an ongoing basis, particularly when addressing subprime and other populations that are more prone to losses. When lenders are faced with the potential of an increase in delinquencies, a well-defined methodology is critical to help track scorecard variations to determine if adjustments to score cutoffs or pricing are needed.

To address the challenges posed by economic and societal changes, a series of steps can help mitigate risk and improve automated risk scoring mechanisms. New strategies for loan refinance, payment delay or forbearance, and collections are going to be needed.

• Leveraging a past production cache or data stored in a data warehouse, produce through-the-door distribution of risk scores, model attributes, volumes and Population Stability Index (PSI) as your benchmark.

• Once the benchmark is established, track distribution of risk scores, model attributes, volumes, PSI, on a daily, weekly, or monthly basis.

• Analyze trends and divergence from the benchmark, then identify new risk score cutoffs and strategies.

• If needed, perform this regular tracking, reporting and analysis on a long-term basis.

Always be testing and adjust your underwriting accordingly

An enhanced underwriting process that factors in loan deferment, loan forbearance, and ability to cure are critical. As an example, you could have consumers with artificially high scores that have shown no short-term change as a result of forbearance. A decision to lend should most likely not be made if the potential debt burden will be too high once the customer exits the forbearance or deferment window. You can help your customers avoid ‘payment shock’ once the period ends and deferred payments are due.

An effective approach to testing will help lenders understand how key factors will impact their client base. Pre-developed test sets can help risk managers and credit analysts easily test the impact of changes to different variables to help determine if adjustments to the credit policy are needed. To conduct an impact analysis in a test environment, test data that is specific to each of these scenarios can be extremely useful — bankruptcy, collections, delinquency, experience of trades, and new credit. Understanding the impact of changes to these variables on your scoring models will, in turn, help you formulate appropriate collection and treatment strategies.

Keep your customers in mind

It is important that you remain in tune with your customers’ individual debt burdens, and balance the management of risk with empathy for your customers and the unanticipated situation they find themselves in. With more loan deferrals and forbearance, the ability of auto finance applicants to assume additional debt may be in question and can create undue and unnecessary burden. A shift in strategy and focus now will benefit everyone in the long run.

Michael Sogomonian is the director of decision science at Digital Matrix Systems.

Instead of dealers walking around with wads of cash in their pockets to give to potential car buyers and service drive customers, findings from a recent study conducted by daVinci Payments described different approaches dealerships could be using.

The study found that customers in the market for a new vehicle can be significantly incentivized to take a test drive or visit the dealership for vehicle service on a continued basis, by pairing these activities with a prepaid monetary reward.

With 49% of individuals surveyed intending to purchase a vehicle in the next 18 months, daVinci Payments explained this study can provide dealerships with insights on how to encourage customers to push past intent to purchase a vehicle, as well as retain those customers after the point of sale for ongoing parts and services transactions.

The study also found that respondents prefer open-loop prepaid rewards to retailer gift cards or repair discounts. This response extends to a preference for receiving a lower-valued prepaid reward over additional dollars off of the vehicle sticker price or monthly lease rate.

Key findings from the study include:

— 92% of intenders (those planning to buy a new vehicle in the next 18 months) said they would use a $25 virtual prepaid reward that was texted to their phone after a test drive.

— 89% of intenders would use a special service offer that accompanies a prepaid reward.

— 53% of intenders would prefer getting a $15 prepaid reward for each scheduled maintenance visit rather than receiving a 10-percent discount on each maintenance appointment.

— 50% of Generation Z and millennials would bring their vehicle to the dealership for prevention maintenance for a $35 prepaid reward upon arrival.

With only 30% of the average dealership’s revenues coming from vehicle sales and the larger portion of annual revenue coming from service contracts and parts and service sales, daVinci’s study highlighted the opportunity to use open-loop prepaid rewards to increase repeat revenue and grow existing customer bases.

For example, dealerships see a 10% increase in closing rates when taking a prospective customer on a test drive, therefore, “a minimal investment in monetary rewards used as an incentive to take a test drive can result in significant vehicle sales that in turn can drive service when offers accompany test drive reward,” daVinci Payments said.

Even Gen Z and millennials, who daVinci Payments said are notoriously difficult to steer towards brick-and-mortar, deem a prepaid reward incentive enough to bring their vehicle in for prevention maintenance.

Rodney Mason, daVinci Payments’ chief revenue officer closed by stressing that, as dealers know, every face-to-face touchpoint with a buyer serves to build the relationship and present new opportunities to upgrade the client’s driving experience.

“It’s difficult to ignore that 92% of those who intend to buy a car in the next 18 months would complete a test drive for as little as $25 on a virtual prepaid card,” Mason said.

“Their propensity to accept and use virtual rewards and special offers that accompany them, provides dealers with much greater flexibility and value in executing incentives versus just a few years ago,” he went onto say.

The complete study completed by daVinci Payments can be downloaded here.

Ken Kertz summed up FICO’s 2019 U.S. Consumer Survey of Vehicle Finance Perceptions with a point relevant whether a finance company only has a footprint in a couple of states or builds its portfolio from originations nationwide.

“The takeaway for lenders is it’s all about convenience. The less decisions people have to make, the better. The more collaboration, be it online or at the dealership, the better,” Kertz told Auto Fin Journal as FICO released its newest research that looked at how consumers view the financing of their new- and used-vehicle purchases, as well as how vehicle finance companies are currently meeting customer expectations.

The survey determined that there is a disconnect between consumers’ finance preferences for current loans and consumers’ finance preferences for future loans — with the largest gap centered on digital (nearly a 15-point difference). More than a quarter of consumers (28 percent) listed online financing as their first choice for their next loan, an increase from the number of current online borrowers (13 percent).

Conversely, 63 percent of consumers applied for their current automotive loans from the dealership, but only 40 percent said dealership financing would be their first choice for their next automotive loan.

Kertz, who is senior director and practice leader for auto and motorized at FICO, elaborated about the leading points of the latest survey.

“From my side of the story, I think this is a continuing process,” Kertz said. “Consumers are still seeking a frictionless buying experiences. It’s still not quite there yet. They truly want to take control as much as lenders, dealers and OEMs will give them. They still want to feel in the end that they got a good deal, that they’ve made an educated decision both from their standpoint and that the lending institution and the dealership are helping to further that education.

“We’re seeing the digital piece climb up a little bit. It is going to take a few years, maybe three to five, where you can do the majority of your process online, but that’s creeping up. The dealers are obviously still that central focus to do all-in-one shopping experience both for the vehicle and loan,” he continued.

“It’s still revolving around what the lenders can provide the customers from a technology standpoint. When it’s frictionless as possible, the consumer will take advantage of that,” Kertz went on to say. “The technology piece is hard. We hear from our customers that’s it’s going to be another three to five years to remove a lot of that friction to make the researching, the getting the loan, the getting the funding, totally taking place without any human intervention, just go to the dealer and pick up the vehicle.

“For me, the message really is technology is going to help shape the process over the next few years. It’s not there yet. It’s going to take some time. The consumer will take advantage of that technology as much they can give them over that period,” he added.

While dealership financing continues to be the preferred loan option, FICO discovered online loans are gaining traction, which is being driven by the changing consumer expectations. Consumers cited the following top factors for financing options:

• For online financing, consumers most valued convenience, comparison shopping across finance companies and speed.

• For dealership financing, consumers most valued one-stop shopping, possible promotions and discounts and a tie between feeling they might get a better deal and that’s how financing was secured last time.

• For bank or financial institution financing, consumers most valued trusting and liking their bank, believing they get the best rate at their bank and negotiating power.

“With the accelerating adoption of digital, our findings suggest that the U.S., as well as the global market, may be reaching a tipping point where the shift to digital happens rapidly given consumer expectations and the availability of new technology,” Kertz said in a news release.

“Consumers want simplicity and transparency whether financing online or at the dealer, and need to trust the process. Consumers will have a stronger say in how, where and who they do business with, and will greatly influence the emerging business models available today,” he added.

Currently, the majority of the consumers (78 percent) are initiating automotive loan discussions. FICO indicated 95 percent of consumers would consider only between one to three finance companies. They care most about their monthly payment (92 percent), length of term (90 percent) and interest rate (87 percent).

FICO mentioned other significant findings from its new survey included:

• Forty-eight percent of consumers considered only one lender, and 47 percent considered two to three lenders.

• The majority of consumers (78 percent) have to initiate their financing discussions today.

• Ninety-one percent of consumers would accept (or at least consider) an instant vehicle loan offer if that meant they could avoid dealing with a bank or doing extra paperwork.

• The U.S. had the lowest percentage of loans for a new vehicle at 48 percent, compared to 61 percent globally.

• Sixty-eight percent of U.S. consumers rated the financing experience as easy, which tied for the second lowest ranking in surveyed countries behind New Zealand’s 66 percent with the global average at 74 percent.

“Consumers are getting more and more control over the purchasing process. It’s really a consumer empowerment message,” FICO senior manager of solution marketing for risk Mica DuBois told Auto Fin Journal.

“Those lenders and the mix of providers that meet consumers and reduce friction and care about those touchpoints across the entire life cycle, those are the ones who are going to win in the long term. We need to keep doing what's working and close any experience gaps that might exist,” DuBois went on to say.

FICO’s independent research surveyed 2,000 adult consumers across nine countries, including the U.S., Canada, Mexico, Chile, Australia, New Zealand, Germany, Spain and the United Kingdom. The respondents were between the ages of 18 and 64 who acquired a loan or lease on a new or used vehicle within the last three years.

Dealers probably know this sequence all too well. A walkaround and test drive of a vehicle both went well, and the financing process advanced to the point where the potential buyer sees what the monthly payment could be.

Then customers recoil, become frustrated and perhaps even leave the showroom, turning into a dreaded “be back.”

With that scenario in mind, Cox Automotive’s Rates & Incentives Group (CAR&I) released a new whitepaper on Friday, pinpointing a lack of transparency and accuracy in the pricing and payment negotiation process as a main cause of friction between dealers and consumers that can derail a deal.

With vehicle prices and interest rates rising and consumer affordability declining, CAR&I emphasized dealers can’t allow any details to slip through the cracks. It’s why the Cox Automotive division generating the whitepaper titled, “Optimizing Rebates & Incentives for Consumer Digital Retailing Experience.”

According to the 2018 KBB.com Incentives Survey, only 24 percent of shoppers are fully aware and researched all incentives. Historically, Cox Automotive acknowledged transparency into consumer incentives has varied. Changing customer expectations and shopping behaviors now make full transparency required, according to CAR&I.

Today, more automotive dealer service providers (DSPs) are moving the process of applying incentives from a dealer practice to a consumer-centric experience through digital retailing tools. With these new tools, customers can confidently research and price a specific vehicle with the incentives and conditional offers applied — all without entering a dealership.

But CAR&I stressed the success of the deal, however, relies on the accuracy of a dealer’s data within the DSP application.

Utilizing a methodology developed by CAR&I, this new whitepaper analyzes the accuracy of the data used to calculate pricing and payment information presented through DSP tools. In the study, CAR&I compared APRs, cash and conditional incentives through these various tools for seven new vehicles in the East Coast and West Coast markets.

The analysis looked at data from three competitive incentive providers, including CAR&I.

The study found significant variations across the three providers, ranging from $0 to $6,750 in pricing for the same vehicle, resulting in monthly payment fluctuations up to $122 per month for 60 months. The analysis also showed that both unnamed vendors incorrectly applied incentives for two vehicles, resulting in $500 to $750 in overstated incentives applied incorrectly costing dealers valuable margin.

CAR&I emphasized these disparities have wide-ranging consequences for dealers, including a loss of credibility in pricing as well as a loss on deals and profit. Paper authors said it’s not just that consumers might walk away from one purchase. It can affect repeat purchases and referrals, too. Pricing information must be perfect for digital retailing to build trust and transparency, and to improve the customer experience. This also means making accurate pricing available online.

“If DSP application incentive tools aren’t spot-on, the pricing information given to consumers is also inaccurate. If incentive and rebate data isn’t accurate, the whole deal can be sunk,” said Brad Korner, general manager for CAR&I. “Dealers in this hyper-competitive auto retail landscape can’t afford to have less-than-perfect pricing data. That can result in unhappy consumers and lost business.”

CAR&I pointed out that rebates and incentives also continue to play a major role in generating demand and sales for many brands.

Approximately 94 percent of new vehicles sold have a financial incentive applied to the transaction (purchase, finance or lease) which requires accuracy for dealers presenting pricing and payments to their online shoppers, according to Cox Automotive.

CAR&I went on to stress that sharing full coverage of all OEM incentives, and allowing consumers to see what they qualify for, builds trust in the process. It also provides necessary information to inform the buying journey.

The full whitepaper on “Optimizing Rebates & Incentives for Consumer Digital Retailing Experience” is available here.

GM Financial is enhancing its efforts to ensure the individuals signing contracts with the captive are in fact who they say they are.

This week, GM Financial announced its collaboration with Spring Labs as part of its Spring Founding Industry Partners (SFIP) Program, which is geared to drive improved data management standards to help address critical auto finance industry issues like identity verification and synthetic identity fraud.

The SFIP program brings together financial institutions, data furnishers and technology partners to collaborate on research, development and implementation of Spring Protocol, the company’s blockchain technology network, prior to its public launch. Ultimately, this network is designed to transform how information and data are shared globally.

“As the captive finance arm for General Motors and one of the world’s largest auto finance providers, we are continually innovating and evolving our fraud prevention and detection capabilities to better serve and protect our customers and dealers,” said Mike Kanarios, chief strategy officer at GM Financial.

“Today’s announcement underscores our commitment and investment to advance these efforts, and we are pleased to collaborate with Spring Labs as a member of the SFIP program,” Kanarios continued.

Spring Labs chief executive officer Adam Jiwan added, “We are excited to partner with GM Financial to create solutions on our developing network to address vexing economic problems such as identity fraud.

“We look forward to announcing additional significant partnerships in due course,” Jiwan went on to say.

Editor’s note: More details about what’s happening at GM Financial will be showcased in an upcoming episode of the Auto Remarketing Podcast, featuring Kyle Birch, who is the company’s executive vice president and chief executive officer for North America. Previous episodes are available here.

During the Vehicle Finance Conference hosted by the American Financial Services Association this past January in San Francisco, Nick had the opportunity again to sit down with Kyle Birch, executive vice president and chief operating officer for North America at GM Financial.

The wide-ranging conversation covered not only how GM Financial performed in 2018, but also how the captive is leveraging both people and technology to be successful.

The podcast discussion can be found below.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

You can also listen to the latest episode in the window below.

Catch the latest episodes on the Auto Remarketing Podcast homepage and on our Soundcloud page.

Please complete our audience survey; we appreciate your feedback.

How fintech is going to be the technological solder that binds dealerships, finance companies and consumers into an even stronger relationship permeated discussions at a host of annual automotive events late last month in San Francisco.

Cherokee Media Group is looking to continue that dialogue in a more intimate conference setting when it again hosts the Automotive Intelligence Summit, which aims to give leading experts in the auto fintech space the opportunity to reinforce the need for collaboration to strengthen current revenue streams and open new ones.

“Last summer’s first Automotive Intelligence Summit poured a great foundation for industry dialogue we heard for the remainder of 2018 and into the opening portion of this year,” Cherokee Media Group president Bill Zadeits said. “And we want this year’s Summit to extend that conversation where dealerships, finance companies, fintech entrepreneurs, investors and related experts all can let their voices be heard in an interactive setting that delivers more than just talking points, but also tangible strategy to lift the entire industry.”

The Automotive Intelligence Summit again will be in Raleigh, N.C., in the heart of North Carolina’s Research Triangle. Nestled among some of the most successful technological companies and leading universities, attendees will be gathering in the Tar Heel State capital on July 23-25 for a mix of keynote presentations and networking opportunities.

Last year, experts from an array of successful firms participated, including:

— Ally Financial

— Cox Automotive

— defi SOLUTIONS

— DRN

— Experian

— EY

— Fair

— Hudson Cook

— IBM

— IHS Markit

— KAR Auction Services

— Maryann Keller and Associates

— National Automobile Dealers Association

— SAS

These leading authorities shared not only what’s happening within their shops, but also provided projections about ways fintech might influence how dealerships and finance companies gain new customers as well as retain current ones.

Cherokee Media Group is already accepting applications to speak this summer’s event. Applications can be completed here.

“We are looking to provide the platform for the most innovative companies, experts and executives to showcase what is going to impact our businesses so the industry can remain nimble and address potential challenges,” Zadeits said.

“We all know fintech development is in constant motion,” he continued. “The Automotive Intelligence Summit will provide a pathway for growth for the remainder of 2019 and beyond.”

For more details about the Automotive Intelligence Summit, go to www.autointelsummit.com.

Whether a consumer is buying a personal care item costing just a few bucks or financing a vehicle purchase involving thousands of dollars, Experian insisted that digital commerce has changed the way consumers interact with businesses. Experts see how commerce is moving from face-to-face transactions to anonymous relationships built on trust.

Difficult to achieve and earned over time, Experian sees trusted online relationships are based on businesses providing a secure environment and a great customer experience.

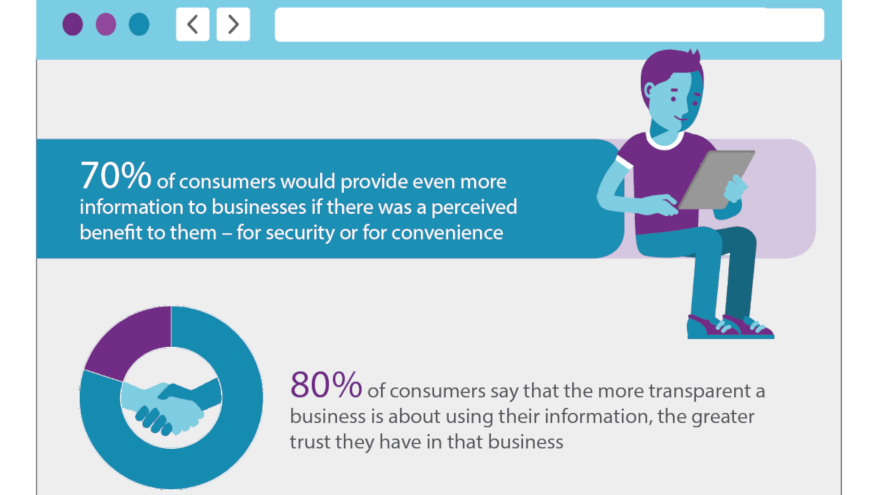

In light of that backdrop, Experian’s Global Identity and Fraud Report found that 74 percent of consumers see security as the most important element of their online experience, followed by convenience.

While businesses often have invested in one at the expense of the other, Experian discovered that consumers across the globe expect both. So much so that 70 percent of them are willing to share more personal data with the organizations they interact with online, particularly when they see a benefit such as greater online security and convenience.

“Security and convenience are the bedrocks of a dynamic digital marketplace that effectively manages risk and delivers a seamless experience,” said Steve Pulley, Experian’s executive vice president and general manager of global identity and fraud solutions.

“The availability of information consumers share with businesses makes this possible, but it’s the same information that puts them at a greater risk for fraud, making trust more important than ever,” Pulley continued.

Findings from the study also reveal that consumers and business leaders agree that security methods enabled by new technologies and advanced authentication solutions instill online trust.

In fact, consumer confidence grew from 43 percent to 74 percent when physical biometrics was used to protect their accounts.

Experian learned that businesses also are beginning to embrace the changing technology. Half of organizations globally reported an increase in their fraud management budget over the past 12 months.

“Trust begins with a business’s ability to deliver more from the information they already have and to use advanced technologies to identify their customers and provide a relevant experience without increasing their risk exposure,” Pulley said.

“In other words, consumers really can expect both — security and convenience.”

The report went on to discuss how many businesses are proactively sharing with customers how they use their personal information. The report found that nearly 80 percent of consumers say the more transparent a business is about the use of their information, the greater trust they have in that business.

The report revealed that 56 percent of businesses plan to invest more in transparency-inspired programs such as educating consumers, communicating terms more concisely and helping consumers feel in control of their personal data.

To develop the study, Experian interviewed more than 10,000 consumers and more than 1,000 businesses across 21 countries around the world.

Additional findings from the third annual fraud report include:

• Fifty-five percent of businesses reported an increase in fraud-related losses over the past 12 months, particularly account opening and account takeover attacks.

• Sixty percent of consumers globally are aware of the risks involved with providing their personal information to banks and retailers online.

• Ninety percent of consumers are aware that businesses are collecting, storing and using their personal information.

• Banks and insurance companies are the organizations trusted most by consumers across most regions. Online retail sites and social media sites trail considerably on trust.

• Nearly nine out of 10 consumers report conducting personal banking as their top online activity.

• Passwords, PIN codes and security questions remain the authentication methods most widely used by businesses, followed by document verification, physical biometrics and CAPTCHA.

The Global Identity and Fraud Report also shows how different regions across the globe view and manage fraud:

• Concern for fraud and increased fraud losses are highest among businesses in the U.S.

• The greatest number of consumers who already have experienced a fraudulent event online are in the U.S., with the lowest number of consumers from EMEA.

• The U.S. and the U.K. lead with the biggest increase in fraud management budgets over the past 12 months, with three-quarters of businesses budgeting more for fraud management this year.

• Latin America is a top user of advanced authentication technology where CAPTCHA, physical biometrics and customer identification programs make up the top three authentication methods. This differs for businesses in other regions, which rely more heavily on passwords, PIN codes and security questions.

• Physical biometrics seems to have the largest positive impact on trust, particularly in Colombia and the U.S.

• The U.S. has invested the most when it comes to transparency initiatives in the past 12 months, and Colombia has the highest intent to invest more in the next six months.

Experian’s identity and fraud business comprises more than 300 fraud experts around the world working to protect people’s identities and fight fraud for businesses across multiple sectors, including financial services, telecommunications, retail/e-commerce, insurance, government and healthcare.

The full Global Identity and Fraud Report can be downloaded here.

With the vehicle-financing process in constant evolution, the demand for dealerships and finance companies to handle consumer concerns is growing, too.

A new commissioned study conducted by Jabian Consulting on behalf of Equifax confirmed that dealers and finance companies alike believe more consumer education, access to data and faster processes will help enhance the vehicle-buying journey.

The study’s goal was to evaluate what dealers and finance companies want to stay and/or remain competitive amid changing consumer buying behaviors.

The study found that universally both franchise and independent dealers want to predict and understand consumer behavior by enabling early engagement online, and leveraging consumer information (trade/buying habits) to help power the consumer purchase. Both dealers and finance companies across the credit spectrum want to engage ahead of the showroom through more guided marketing to better match customers with vehicles during the research process, and ensure the right inventory when the customer arrives at the dealership.

Finance companies cited more insights to engage with consumers before they enter the sell phase at the dealership to inform them on financing to provide a more confident shopping experience.

Additionally, desire for a more educated consumer also came out of the research, for dealers, which highlighted that a customer educated with the right information was better for the dealership and sales process than a customer that was entering the process with negative perceptions or inaccurate information.

Ultimately, the study showed both dealers and finance companies recognize the need to create a more personalized shopping experience.

As an example, a recent Cars.com study revealed that seven out of 10 consumers are undecided about make and model when they shop for a new vehicle, yet nearly all online car search experiences force people to select make or model as the initial step in their research rather than first understanding their unique needs to offer suggestions specific to their desires.

Dealers and finance companies were looking to more analytic and predictive insights to help get them ahead earlier in the process, and proactively offer up the vehicles a consumer was most likely to select.

“The end goal is helping auto dealers and lenders connect the dots with technology for faster adoption and implementation of solutions that ultimately make the consumer buying experience more personalized, efficient and successful,” said Chad McCloud, executive director at Jabian Consulting.

“Solutions like analytic insights and consumer verification accelerate that experience in a positive way,” McCloud continued. “The good news is that many of these customer-centric solutions already exist, and it’s simply a matter of creating and implementing a strategy to maximize their effectiveness.”

Jennifer Reid, vice president of automotive strategy and marketing at Equifax Automotive Services, offered her reaction to the study. Before joining Equifax, Reid spent part of her career working at both dealerships and finance companies, helping consumers secure their transportation.

“When you saw game changers launched last year like Fortellis Automotive Commerce Exchange, and the innovation highlighted at NADA to solve for digital retailing, it provides an opportunity to connect data and leverage analytics much earlier in the process to help fuel tailored, consumer-centric experiences,” Reid said.

“The industry is ripe with intelligence for auto dealers, lenders and the ever-evolving consumer; the key is it needs to be in the right place and connected to deliver the full value,” she continued.

“Equifax has the solutions powered by our investments in technology, analytics and industry expertise to help lead auto dealers and lenders to the next generation of connectedness for an end-to-end relationship with consumers throughout their shopping and ownership journey,” Reid went on to say.

Adopting consumer-centric personalization strategies leveraging predictive insights in the shopping experience has surfaced as a key strategy for successful digital retailing and is top of mind for the dealers and finance comapnies interviewed in the study.

As highlighted in research by CDK Global, 80 percent of car buyers are likely to begin the vehicle-buying process online. Still, 78 percent said they value the in-store dealership experience.

“It’s not just about being earlier, but being connected online and in the showroom,” said Reid.

Reid recently participated in an episode of the Auto Remarketing Podcast discussing the topic further. The episode is available below.