To commemorate 70 years of serving more than 100,000 worldwide members, Blue Federal Credit Union recently paid off five randomly selected members’ loans totaling $70,000, including two vehicle retail installment contracts.

In June, credit union officials said any member in good standing who took out any loan sans a first-time mortgage was automatically entered to have their loan paid off, up to $70,000.

After a three-month-long campaign, Blue Federal Credit Union said 6,469 members and 6,723 loans qualified for the promotion.

According to a news release, the loan payoff amounts ranged from $5,216.54 all the way to more than $23,000. Two cars, two motorcycles, and a personal loan were paid down or paid off during the campaign.

The five winning members were all notified that their loans were paid off throughout September.

Megan, one of the loan payoff recipients who wanted to only go by her first name, said through the news release, “Whoever has heard of a financial institution paying off loans that they generate? I originally took out this loan to cover some personal expenses related to medical bills. Now, my husband and I are starting to think of the future and what we can do together.”

Blue Federal Credit Union president and chief executive officer Stephanie Teubner recapped the campaign’s successes.

“This is something that points to Blue’s mission of discovering pathways to realize possibilities,” Teubner said in the news release. “We exist for our members and because of our members. Paying off loans for our members is a way that we can definitively show that we are in our members' corner and want to see them succeed financially.”

Blue Federal Credit Union vice president of public relations and membership development Michele Bolkovatz added, “We are constantly looking to be in our members’ corner.

“After notifying the recipients of the loan payoff and hearing the disbelief and gratitude, it makes me proud to be a part of an organization that lives up to its mantras and mission,” Bolkovatz went on to say.

This week, Credit Union Leasing of America (CULA) expanded its client footprint for the fourth time this year.

After previously expanding in the Northeast as well as into Texas, CULA announced that it now is partnering Utah’s University Federal Credit Union (UFCU).

The companies booked their first contracts in August, as the partnership makes University Federal Credit Union the only credit union in Utah to offer vehicle leasing.

University Federal Credit Union, which was founded in 1956, serves more than 100,000 members and their communities.

“Our core values are to create a positive impact on our community and to make a difference for every member, every day, and this means making sure a wide range of financial products are available to our members,” UFCU chief executive officer Jack Buttars said in a news release. “Finding the right vehicle at the right price has probably never been more challenging than it is today.

“Working with the terrific CULA team, who streamline the complexities of leasing — from analytics to insurance to operations to compliance — we are now able to ensure that our members have the opportunity to benefit from leasing’s more affordable payments and term flexibility, critical factors given the current market landscape,” Buttars continued.

In addition to Utah, CULA now has coverage in New Hampshire, Texas, Massachusetts, Michigan, Pennsylvania and California.

“We’re pleased to be able to further extend our footprint in the West, at a time when leasing is such an important option for consumers, by partnering with UFCU, an institution that exemplifies what credit unions are all about: serving the community,” CULA president Ken Sopp said. “Utah is a new state for us and we are excited to ‘pioneer’ credit union leasing here.

“Our leasing program can amplify the customer-centric values of University Federal Credit Union, while also expanding and diversifying their portfolio of services, helping to further enhance membership and yield,” Sopp went on to say.

CULA highlighted that that first six months of the year have been record breaking for the company, with more than $950 million in lease originations. That amount represents an 88.8% increase over the same period in 2019 and the highest period of originations in CULA’s more than 30-year history.

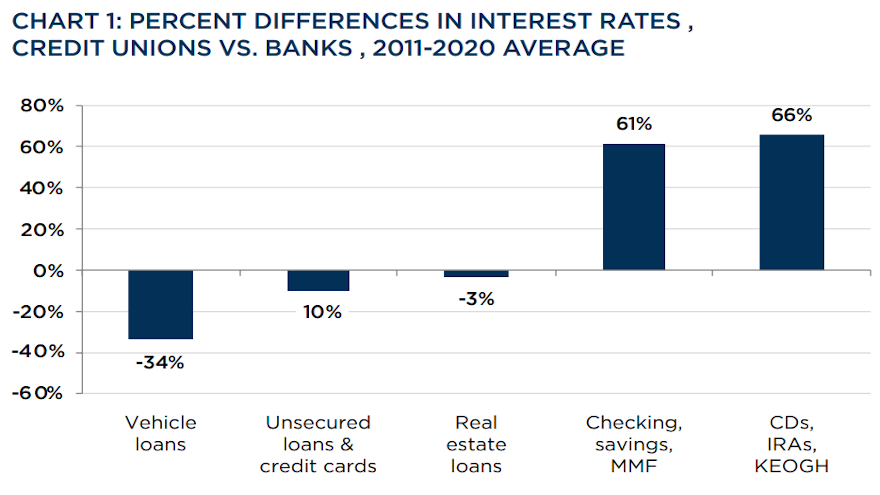

Auto financing was among the positives highlighted in new, independent study released on Monday that examined the economic benefits of the credit union tax exemption to consumers, businesses, and the U.S. economy.

The study commissioned by the National Association of Federally-Insured Credit Unions (NAFCU) determined that credit union rates on new- and used-vehicle financing are 34% lower than what offered by commercial banks.

The study conducted by Douglas Meade of the Interindustry Economic Research Fund and American University’s Robert Feinberg also found that removing the credit union tax exemption would have far reaching consequences for consumers and the economy.

NAFCU reiterated that credit unions are member-owned, not-for-profit cooperative financial institutions that serve defined fields of membership under the general oversight of volunteer boards of directors.

While banks have been lobbying Congress to remove credit union’s tax exemption, NAFCU said its study underscores the economic damage that would occur.

NAFCU pointed out that the study found that removing the tax exemption status for credit unions would reduce tax revenue by $56 billion and reduce economic activity by $120 billion over ten years.

The study also showed it would eliminate 80,000 jobs a year over 10 years.

“As not-for-profit cooperative financial institutions, credit unions have always put their members first by providing them with the best financial products, rates, and lower fees,” NAFCU president and chief executive officer Dan Berger said in a news release. “Today, 127 million consumers are members of a credit union. Consumers continue to recognize the benefits of credit unions and how a credit union can help them achieve financial freedom.

“The tax exemption status provided to credit unions has yielded dividends to consumers, Main Street businesses, and the U.S. economy through lower fees, better financial products and better rates,” Berger went on to say.

Along with the auto financing metric, the study also found that the credit union tax exemption benefits households to the tune of $15 billion a year. NAFCU explained this benefit derives from credit unions passing along the value of their tax exemption to their members through low rates and fees.

Furthermore, NAFCU the study showed that non-credit union consumers benefit from the competitive influence of credit unions on other financial institutions.

A 50% reduction in credit union market share would cost bank customers between $6.8 to $9.9 billion per year in higher loan rates and lower deposit rates, according to the study, which can be downloaded via this website.

Credit Union Leasing of America (CULA) is on quite a roll after posting its ninth consecutive month of record lease originations in June.

After booking $150 million in lease originations in a single month for the first time in October, CULA said it surpassed $200 million in lease originations in a single month for the first time in its history in May.

Then the company followed that performance by facilitating more than $215 million in lease originations in June.

CULA highlighted in a news release that the first six months of 2021 brought in more than $950 million in lease originations, an 88.8% increase over the same period in 2019, and the highest period of originations in its more than 30-year history.

CULA is the leader in indirect vehicle leasing for credit unions and has originated more than $1 billion in vehicle leases for credit unions annually on average since 2018.

CULA looks to help many of the industry’s most innovative credit unions grow membership, diversify lending options and increase yield, including nine of the top 10 credit unions offering car leasing in the U.S.

“This has been a remarkable six months for credit union vehicle leasing and for CULA. Our success is only possible because of our extraordinary credit union partners whose competitive rates and ability to scale their teams and processes have enabled them to meet consumer demand,” CULA president Ken Sopp said in the news release.

In just the past two months, CULA expanded its leasing footprint into New Hampshire and Texas, and recently helped increase regional coverage for credit unions in Massachusetts, Michigan, Pennsylvania, and southern California, among the many markets it serves.

“As CULA has expanded into new states, bringing on new credit union partners, we are well-positioned to serve a post-pandemic market that is seeking out the affordability and flexibility vehicle leasing offers, all of which is reflected in the record lease volume we have been seeing,” Sopp said.

Meanwhile, CULA noted that it has also increased its engagement with dealerships during the past six months, hitting new records for dealerships submitting leases through CULA credit union partners.

For the first time in its history, CULA said it had dealers that leased more than 100 vehicles in a single month through their credit unions — with one dealer just short of reaching the 200-unit mark.

“CULA’s recent milestones were achieved during the lowest new car inventory level in history,” CULA vice president of business development Mark Chandler said. “These record numbers were greatly helped by the increase in the number of our valued auto dealer partners in new and existing markets, all of whom benefitted from the data, analytics and communication specific to each dealer’s inventory that our team provides every day.”

According to Chandler, the trends that have been fueling credit union success with leasing show no sign of abating.

“For those seeking affordable payments as they emerge from the pandemic’s challenges, leasing’s lower payment (on average $100 or more lower per month) makes a huge difference,” he said. “And for those who can’t find the exact model they want because of inventory constraints, a shorter commitment helps advance their decision.

“Just as importantly, the trusted position credit unions hold in their communities in these uncertain times, is more important than ever and that holds true when members are ready to lease,” Chandler went on to say.

A Massachusetts man is scheduled to be sentenced on June 1 after being indicted by a federal grand jury in Providence, R.I., last summer for alleged participation in a wide-ranging conspiracy to defraud seven credit unions through a scheme involving used-vehicle financing.

According to a news release from the Justice Department, Hiancarlos Mosquea-Ramos of Lawrence, Mass., pleaded guilty in U.S. District Court in Providence, as one of nine individuals involved in the fraud.

Officials said Mosquea-Ramos admitted in July that he participated in schemes as the seller or the buyer of used vehicles, defrauding:

— Merrimack Valley Credit Union

— Sharon Credit Union

— Digital Federal Credit Union

— Metro Credit Union

— Direct Federal Credit Union

— RTN Credit Union

— Workers Credit Union

Officials indicated that Mosquea-Ramos admitted that by using his own personal identification information along with counterfeit earnings statements, fabricated automobile purchase and sales agreements and counterfeit motor vehicle titles, he obtained at least $92,000 in fraudulent financing to purchase fictitious cars.

A co-conspirator, Jonathan Pimental, also of Lawrence, Mass., was allegedly listed as the seller of the cars. Pimental is awaiting trial on a charge of conspiracy to commit bank fraud, according to the Justice Department.

Additionally, officials said Mosquea-Ramos admitted that he posed as the seller of various used cars. It is alleged co-conspirator Rolando Estrella,of Lawrence, Mass., prepared false purchase and sales agreements and counterfeit automobile titles naming Mosquea-Ramos as the seller of the vehicles.

DOJ said the financial institutions approved a total of more than $275,200 in used-vehicle financing, disbursing checks made payable to Mosquea-Ramos. The checks were quickly deposited and the funds quickly withdrawn and divided among participants of the conspiracy, according to officials.

The Justice Department said Estrella also is awaiting trial on multiple charges of conspiracy to commit bank fraud, bank fraud, aggravated identity theft, and fraudulent use of a Social Security Number.

Credit Union Leasing of America (CULA) is coming off its two best quarters in company history.

And now the indirect vehicle leasing program provider that empowers credit unions to diversify their existing portfolios is in the Lone Star State.

This week, CULA announced that it now offers vehicle leasing services in Texas through its partnership with InTouch Credit Union (ITCU).

CULA helped ITCU successfully implement its vehicle leasing program in Michigan in the midst of the pandemic, closing the first contract in November.

Based in Plano, Texas, ITCU has close to $1 billion dollars in assets and serves close to 90,000 members across the U.S., as well as more than 20 countries around the world.

“Launching a brand-new auto finance program during the height of a pandemic may seem unusual, but to us it just made sense: the economic uncertainty fostered by COVID meant our Michigan members were looking for the affordable and flexible vehicle finance options that leasing provides,” said Bridger Robinson, senior vice president of lending and branch operations at ITCU. “Plus, we had a partner in CULA who enabled us to ramp up quickly.

“The success of our Michigan program made the decision to offer vehicle leasing to members in our home state of Texas easy,” Robinson continued in a news release.

“CULA’s understanding of the complexities of leasing, and of each market, their commitment to serving our members while helping us improve yield, and their flexibility in customizing services that fit ITCU’s specific member profiles have all been key to the success of our program in Michigan. We anticipate continued success offering our members the best leasing experience in Texas,” Robinson went on to say.

CULA has been facilitating indirect vehicle leasing for credit unions for more than 30 years, providing vehicle leasing programs for credit unions that help them grow membership, diversify lending options and increase yield. The ITCU leasing program marks CULA’s first leasing offering in Texas where vehicle leasing represents about 15% of all new-vehicle sales, according to Experian.

“Texas is one of the largest car markets in the U.S. and, with less than 4% of its credit unions offering vehicle leasing, we believe the opportunity is significant,” CULA vice president of business development Mark Chandler said.

“We are excited to continue to grow our national footprint right here in Texas with such a high caliber, customer-focused partner. ITCU cares about ensuring its members have access to the best financing programs and options available,” Chandler continued.

After a record-breaking fourth quarter, CULA said it started 2021 with its best Q1 ever.

“October 2020 was a record-breaking month for CULA, with more than $150 million in lease originations in a single month, leading to our best Q4 ever,”, of CULA president Ken Sopp said. “The first quarter of the year is typically not a good one for auto sales, but the momentum from Q4 continued. This resulted in nearly $400 million in lease originations for the quarter — our best Q1 ever.”

For more information, visit www.cula.com.

The robust fruit of Enterprise Car Sales working with credit unions for four decades recently reached a major milestone

The division of Enterprise Rent-A-Car announced that week that it has generated more than $12 billion in total origination volume for its credit union partners during the past 40 years.

Executives highlighted in a news release that the announcement underscores the importance of the enduring relationships Enterprise has established with more than 1,000 credit unions nationwide.

“The work we do in partnership with credit unions represents a significant aspect of our business,” said Mike Bystrom, vice president at Enterprise Car Sales. “We’re grateful for the relationships we’ve forged over the years and look forward to continuing to work alongside our credit union partners to help them grow their used-car portfolios.”

With more than 147 dealership locations nationwide, Enterprise Car Sales said that it specializes in offering competitive, transparent pricing on a wide selection of high-quality inventory of vehicles 3 years old or newer.

As Enterprise Car Sales continues to expand into new markets, Bystrom noted that this growth is due in part to the brand’s laser focus on providing exceptional customer service — an attribute it shares with its credit union partners.

“Our longstanding relationship with Enterprise Car Sales is an additional benefit of being a Golden 1 member that offers immense value,” said Reva Rao, senior vice president of consumer lending at Golden 1 Credit Union.

“Golden 1 is committed to providing convenience and exceptional service to our members, and our partnership with Enterprise is one we can trust to do the same,” Rao continued.

The retailer is striving toward the next $12 billion in credit union originations, too.

Enterprise Car Sales recently announced the completion of its nationwide rollout of the Accelerated Customer Experience (ACE) digital platform.

This new in-dealership technology solution, coupled with the launch of “Start My Purchase” functionality on the Enterprise Car Sales website, has enabled customers to complete their purchases as quickly as they’d like.

What’s more, Enterprise Car Sales indicated that buyers now have the flexibility to start their purchase from home (with delivery, where available) or complete their entire purchase inside a dealership location.

Many customers are now able to complete their purchase in 45 minutes or less and some in as little as 15 minutes, according to Bystrom.

“We’ve invested in technology that makes the car-buying process as flexible, easy and transparent as possible for our customers,” Bystrom said. “And we’ll continue to listen to our customers and employees as we look for innovative new ways to meet their evolving expectations.”

Furthermore, to provide drivers with greater peace of mind, Enterprise Car Sales has also introduced its Complete Clean Pledge — a promise to go above and beyond Enterprise’s already rigorous cleaning protocols, including the use of a disinfectant to sanitize more than 20 high-touch points after every test drive and before the customer takes possession of their vehicle.

On the heels of announcing its latest initiatives to support the military, TrueCar announced a partnership to bring exclusive value to servicemembers and their families for all their vehicle buying and financing needs.

TrueCar and Navy Federal Credit Union now are working together to provide members with an online platform to research and compare vehicles that match their preferences, get upfront transactable pricing on local inventory and the option to minimize personal contact at the dealer through TrueCar’s Buy from Home program.

“From personalized pricing and price comparisons in your local area to transparent online car valuation, this partnership is another great way we can help our members find the best vehicle that fits their financial lifestyle,” Navy Federal Credit Union vice president of consumer lending Joe Pendergast said in a news release about Navy Federal’s Car Buying Service.

“TrueCar allows us to further arm our members with the guidance and negotiating power they need to be successful in today’s contactless car buying experience.”

Members can take advantage of TrueCar’s benefits such as:

• Savings: More than $3,500 average savings off MSRP on new models

• Price context: See what other individuals paid for a similar vehicle in your local area

• Real Pricing: Personalized price on a specific vehicle from a TrueCar network dealer

• Trade or sell: The platform looks to offer transparent online valuation with context around factors that affect a vehicle’s value and receive a cash offer in minutes

• Buy from home: Identify TrueCar Certified Dealers that offer remote paperwork, vehicle delivery and vehicle sanitization

• Extensive dealer network: Access TrueCar’s Certified Dealer Network, which includes thousands of dealers nationwide.

“Navy Federal Credit Union is a leader when it comes to member service and support, and membership affinity. We’re delighted to partner with them to provide their members access to military exclusive benefits and a modern digital car buying experience built on a commitment to price transparency, efficiency and value,” TrueCar president and chief executive officer Mike Darrow said.

Additionally, all members can access a variety of exclusive offerings through TrueCar’s military appreciation benefits, including:

• Up to $4,000 worth of benefits for repair and auto deductible reimbursement

• Dedicated TrueCar member service hotline, which includes military vehicle-buying specialists

• Discounts on new and used vehicles from TrueCar network dealers

• Vehicle condition review on every used vehicle

For more with Darrow, listen to the episode of the Auto Remarketing Podcast below.

Alliant Credit Union now is originating vehicle leases in four different states thanks to assistance from Credit Union Leasing of America (CULA).

Having supported vehicle leasing for credit unions for more than 30 years, CULA is helping power the expansion of Alliant Credit Union’s vehicle leasing program into Pennsylvania, completing its first leases in the Keystone State in February.

CULA has been successfully working with Alliant Credit Union since 2017, administering its existing vehicle leasing programs in Colorado, Michigan and Florida.

Based in Chicago, Alliant Credit Union is one of the largest credit unions in the nation with more than $13 billion in assets. Alliant’s history spans more than 80 years and it has more than 500,000 members nationwide.

“As consumers emerge from the economic and personal challenges of the pandemic, they are seeking affordable, flexible options in vehicle financing, which is exactly what leasing provides,” Alliant Credit Union vice president of consumer lending Jeremy Pinard said in a news release.

“And, with vehicle leasing representing over one-third of all new auto financing in Pennsylvania, it just makes sense for us to offer it to our members there, and to continue expanding that opportunity to more states nationwide,” Pinard continued.

“CULA has been doing leasing for a long, long time, and they have the historical data to answer any questions a credit union might have. As a partner, they really help you understand the complexities of a lease. Specifically, important elements like residual risk, wear and tear and how that ties into the risks related to leasing,” Pinard went on to say. “With CULA, you can work to create a leasing program that fits your credit union’s desires, goals and expectations.”

CULA enables credit unions to offer the flexibility and affordable payments of new-vehicle leasing, while also helping them grow membership, diversify lending options and increase yield.

CULA experienced first-hand the recent swell of consumer interest in leasing. After the challenges of stemming from spring’s COVID-19 lockdown, the fourth quarter represented CULA’s best quarter ever for lease originations booked through its credit union partners.

“October 2020 was a record-breaking month for CULA, with more than $150M in lease originations in a single month,” CULA president Ken Sopp said. “We finished the quarter strong, and we are well-positioned for a successful 2021.”

And part of the reason CULA can make that claim is because of enhanced relationships with clients such as

“We are excited to further deepen our partnership with Alliant Credit Union as they expand their auto finance offerings into new states,” CULA vice president of business development said Mark Chandler. “Their member-first philosophy, along with their commitment to digital services, means they are well-positioned to meet consumer interest in leasing in today’s new pandemic normal.

“Like Alliant, CULA has a customer-first philosophy, and we are laser-focused on helping our credit union partners achieve their growth goals,” Chandler added.

Visit www.cula.com to learn more details about the firm’s leasing program.

Black Book’s presence in the credit-union market strengthened on Thursday.

The provider of vehicle pricing and analytics announced the integration of Black Book values into the Origence consumer LOS, a CU Direct brand.

The companies highlighted in a news release that the Origence consumer LOS is a comprehensive loan origination system designed to improve the lending experience for both consumers and lenders for a variety of loan products, including indirect auto loans largely driven by its connection to the CUDL network.

The Origence consumer LOS is designed to remove the friction from the lending process with customizable workflows and data-driven decisions via its robust decision engine.

“With the integration of Black Book data, including new and used car/light truck, Powersports, RV/camper, and cars of particular interest, Origence customers will have access to unparalleled, comprehensive industry data,” Black Book executive vice president of revenue Jared Kalfus said.

“This data, coupled with our industry-leading history adjusted valuations, will provide the insights necessary for financial institutions to successfully grow their vehicle lending portfolios,” Kalfus continued.

Black Book’s integration with the Origence consumer LOS can give credit unions another choice when customizing workflows, providing them with easy access to data that further improves decision making and the overall auto-financing process.

“Through our partnership with Black Book we’re able to provide the data necessary to simplify the decision-making process for lenders,” said Bill Lynch, senior director of strategic alliances for Origence.

“This data forward approach is a great offering for our clients. The integration of Black Book Values into our consumer lending platform further expands our support of all types of vehicle loans for our lenders,” Lynch added.