Wolters Kluwer is continuing to see a gradual migration by dealerships and finance companies to more digital infrastructure.

Wolters Kluwer head of auto strategy Tim Yalich took time during the 2023 Vehicle Finance Conference in Dallas hosted by the American Financial Services Association to describe the challenges that remain during this episode of the Auto Remarketing Podcast.

To listen to the conversation, click on the link available below.

Download and subscribe to the Auto Remarketing Podcast on iTunes.

Pete MacInnis, founder and CEO of eLEND Solutions, and his team rolled out a pair of new tools during NADA Show 2023 to help dealerships and finance companies.

First, eLEND Solutions launched of DealMaker, a digital finance pre-desking platform. MacInnis explained that the platform is an evolution of basic online payment calculator tools and the “educated guesswork used by most desk managers.”

Also, MacInnis and eLEND Solutions deployed of IDentify, a layered, multi-factor, identity verification solution designed to verify a customer’s true identity and establish “proof of presence” in an interaction.

Both tools are geared to help amid an uncertain economic landscape with fraud growing more prevalent.

With DealMaker, eLEND Solutions said it is designed to eliminate frictions and profit leaks by providing customer and vehicle-qualified payment terms matched to finance company fundable contract terms prior to the F&I handoff.

“Most digital retailing experiences promise more than they can deliver, especially when it comes to matching a consumer’s credit profile, vehicle selection and deal structure to a fundable purchase contract with lenders,” said MacInnis, who runs an automotive fintech company focused on accelerating “transactional” digital buying experiences.

With affordability representing a bigger challenge to vehicle buyers and monthly payments matter more than the selling price, eLEND Solutions contends that ensuring quoted payments are accurate is critical to modern retailing success.

Yet, in a new report from eLEND Solutions, based on a recent survey of auto dealerships, the majority said it’s common for payment estimator tools to provide inaccurate or unrealistic payment expectations.

DealMaker is designed to solve this matter and is currently being piloted by a handful of dealers across the country.

Here’s how DealMaker is designed to work:

• DealMaker is powered by a logic- and rules-based decision engine and pre-desking software that goes deeper than other tools that calculate payments based on factory cash, finance, and lease incentives with fully integrated rates and residuals.

• DealMaker is embedded within the dealer’s sales and finance workflow, similar to a finance company’s loan origination system (LOS) and empowers fundable deal structuring matching the vehicle model ID/trim level and the consumer’s entire credit profile to a waterfall of lender programs, including underwriting, pricing, loan advance and stipulations simultaneously.

• DealMaker includes advanced credit filtering and calculation logic for all makes, all models, new and used, all terms and all credit tiers.

• Consumer-submitted credit application and full credit file is parsed and filtered by DealMaker to determine ability, stability and credit qualifications.

• DealMaker’s rules-based decision engine then calculates debt-to-income, payment-to-income and loan-to-value ratios; identifies high credit, time on credit report and lender rules, which can vary depending on consumer qualifications.

• DealMaker’s loan program pricing varies by lender and is based on: is the vehicle new, pre-owned, or certified pre-owned? Is it the same brand as the captive lender, are there mileage limitations at different terms and more.

• DealMaker credit decision results are displayed instantly at the point of sale.

• DealMaker matches “The Deal” to the best lender fundable program.

•The near-final deal can be negotiated online or completed before the test drive ends.

A hybrid, pre-desking solution for digital retailing, MacInnis noted that DealMaker is powered by advanced credit filtering and calculation logic and can match a remote or in-store customer and vehicle-of-choice to a waterfall of qualifying finance company programs, “eliminating F&I guesswork.”

MacInnis mentioned that 88% of dealers report they would realize a 10% or more increase in F&I sales penetration if consumers are quoted qualified payment terms matched to finance company fundable contract terms, with dealer mark-ups, before getting to the F&I office.

Moreover, MacInnis said 85% of surveyed dealers estimate that this process could save 15 minutes or more in the F&I office (with over 30% saying it would save more than 30 minutes).

“Quoting transactional and fundable rate, term and payment options reduces frictions during the negotiation, leads to faster, more profitably structured deals and higher closing ratios. It can also positively impact F&I sales penetration,” MacInnis said.

“Making deals transparent is the linchpin to accelerating digital retailing into truly successful modern retailing. This, along with fully connected workflows, is the mission of DealMaker,” MacInnis went on to say.

Details of fraud-stopping tool

MacInnis said a combination of identity proofing technologies can dramatically reduce fraud risks by detecting account takeover, true name, synthetic and other forms of identity fraud in the vehicle purchase process.

In just the past year, eLEND Solution’s recent report found that 79% of dealers directly experienced an identity fraud-related vehicle loss at their dealership.

Furthermore, the report revealed that the large majority are not using any identity verification technologies as part of their fraud prevention strategy, instead choosing to rely on conventional methods such as photocopying IDs.

“These unsophisticated defenses are not only ineffective against increasingly sophisticated fraud schemes, but they also put dealerships at risk” MacInnis said in another news release. “This is why we developed IDentify, which offers unparalleled ID fraud protection for dealerships, including protections for both traditional (in-store) and digital retailing (remote) transactions” continued MacInnis.

IDentify offers a combination of multi-factor identity verification solutions:

• Identity Data Check can cross match customer-provided information against hundreds of databases, including government agencies, public utilities, cell phone carriers, etc. to verify the customer’s name, address, date of birth, Social Security and cell phone numbers.

• Confirm Identity is a multi-factor authentication and fraud prevention tool that can replace traditional out-of-wallet questions with a “proof of presence” feature that sends a one-time passcode to the cell phone number of the customer identified by the phone carrier.

Here’s how IDentify is designed to work:

• Once a customer has signaled a strong intent to buy, dealers can send an email link to a short form requesting their personal information and their consent to verify identity to protect against identity fraud.

• If a customer has already submitted a credit application through one of eLEND’s Credit Solutions, the consent language includes running the IDentify Data Check Report.

• In-store, dealers are able to get customer consent and run the IDentify Data Check Report through the dealer dashboard.

• Dealers have the option to run the Identity Data Check independently or in conjunction with the Confirm IDentify multi-factor authentication and fraud prevention tool.

• Results are displayed in the dealer dashboard, showing a match to customer name, address, date of birth, social security number and cell phone or an alert that warns there is no match to database records.

• IDentify can be implemented in any digital retail solution through APIs – an increasingly critical function as 95% of dealers attribute increased identity fraud to the increased digitization of the deal and remote buying.

Chuck Bell is corporate finance director for Bayway Auto Group and added perspectives in the news release from eLEND Solutions.

Bell said, “eLEND Solutions IDentify product is a core component of our digital retail strategy. It enables us to identify our customers before engaging in test drives and remote test-drives or deliveries. It has already saved us countless thousands of dollars.”

MacInnis added IDentify is fully integrated with eLEND Solutions’ ID Drive, a driver's license scanner that can perform dozens of forensic document tests in real time for robust authentication on any driver's license or any other government issued ID from the U.S., Canada, and Mexico, plus 160 worldwide jurisdictions.

Furthermore, MacInnis said eLEND’s Identification Solutions are integrated with eLEND’s Credit Solutions that match identity to credit application and credit report data. From pre-screen, pre-qualification and traditional hard credit pulls, all data is cross-referenced and integrated with Red Flag and Synthetic Fraud tools from companies such as 700Credit.

Upstart recently added two new applications to its auto retail platform.

The artificial intelligence (AI) lending marketplace boosted Digital Finance and Online Sales in an effort to offer dealerships a seamless online to in-store vehicle-buying experience, from search to signing.

Upstart Auto Retail combines online and in-store digital retail capabilities with financing and manager tools to help dealerships create an omnichannel car-buying experience. In the second quarter, Upstart will add:

• Digital Finance: Enables a frictionless signing and contracting process, with automated verification, more loan approvals, and next-day funding powered by Upstart’s AI – and no new sales process required for dealers.

• Online Sales: Enables the completion of a car purchase entirely online, including financing and e-signing contract documents.

Both applications can be customized to a dealership’s existing software solutions or workflows, according to a news release.

“Engaging customers with a seamless experience – whether shopping from the comfort or their homes or in-store – is the key to winning in the next generation of auto retail,” said Jeremy Nowling, sales and digital retailing director at Rohrman Auto Group,

“We are excited to continue our partnership with Upstart as it introduces a new range of increasingly flexible and cutting-edge retail and financing software solutions for dealerships,” Nowling continued in the news release.

In addition to Rohrman, Upstart has also partnered with Del Grande Dealer Group (DGDG), one of the largest family-owned automotive groups in the San Francisco Bay Area, and

“In 2022, we launched a successful pilot program with Upstart to extend our leadership in creating a best-in-class digital experience,” DGDG chief executive officer Jeremy Beaver said in the news release.

“We expect to make further progress this year by completing our start-to-finish omnichannel sales approach. Upstart has enabled DGDG to help customers that would have otherwise not had access to reasonably priced auto financing options,” Beaver added.

All told, Upstart said it’s working with 780 dealerships across the U.S.

“Buying and financing a car is an important financial milestone, and Upstart is continually evolving to help dealerships meet customers where they are,” Upstart co-founder and CEO Dave Girouard said.

“As more consumers opt for a digital car-buying experience, the new Digital Finance and Online Sales applications will enable dealerships to deliver the buying experience that consumers expect,” Girouard went on to say.

Wolters Kluwer recently announced fourth quarter and end-of-year results and analysis from its Auto Finance Digital Transformation Index, a resource designed to track the rate at which auto dealers, service providers and finance companies are seeing growth in the evolution from paper-based finance back-office processes to digital.

According to the index, dealers, service providers and finance companies showed a digital adoption growth rate of 56% during the past 12 months dating back to the fourth quarter of 2021.

Wolters Kluwer explained through a news release that rate of adoption is significant considering that the U.S. auto industry saw 2022 new-model sales reach just 13.7 million on the year, the lowest annual total in more than a decade and an 8% decline from the previous year.

For more complete context, Wolters Kluwer pointed out annual new-car sales had crested above 17 million for the five-year period prior to 2020, when COVID-19 impacted the industry.

“The continued macroeconomic impact in auto purchases is having an effect on the index’s rate of adoption measure and overall eContract volume, but year-over-year digital adoption still remains steady and positive,” Wolters Kluwer head of auto strategy Tim Yalich said in the news release.

“In looking ahead to 2023 early estimates from analyst firms are pointing to a slight increase in sales activity, but we believe companies throughout the industry are realizing the value and benefit digital resources, assets and processes are injecting into operational efficiencies, regulatory compliance needs and overall profit preservation,” Yalich continued.

Wolters Kluwer also took a closer look at digital asset and workflow adoption in the securitization markets.

As a way of contextual analysis, and based on an analysis of data from Wolters Kluwer, this digital adoption rate has increased 36% over the last five years.

While the adoption rate is expected to drag in 2023 based on the challenging automotive market conditions, Wolters Kluwer said the ongoing upward trend of securitizations suggests that the trust in digital loan origination and management is well established in the secondary market, with companies realizing efficiency gains in the pooling, auditing, collateralization, and the execution of security exchanges using digital assets.

According to industry data, auto ABS totaled $110 billion in 2022, down 16.7% from the previous year.

Industry observers expect auto-specific ABS to remain relatively flat in 2023.

Despite this pause in further volume growth, a recent Wolters Kluwer survey revealed that roughly 82% of finance company executives said they have plans to digitize more of their securitization processes, paperwork and workflows during 2023.

To learn more and to access additional data insights from the Wolters Kluwer Auto Finance Digital Transformation Index, go to this website.

Last week, Wolters Kluwer announced the latest results from its ongoing industry survey it has commissioned to better understand where automotive, dealer, and auto finance professionals are still finding barriers in adopting more digitized solutions for back-office documentation processing.

Wolters Kluwer presented an online survey to more than 2,000 automotive dealer, finance company and service provider professionals during November. The information, software solutions and services provider said nearly 80% of respondents said they are not currently using digital finance solutions.

The survey showed 23% said they still have not found the right solution to fit their needs, and 24% said they haven’t yet found the right qualified provider to implement these solutions.

Only 11% cited budget reasons as to why they haven’t yet implemented, according to the survey.

Of those that are leveraging digital, Wolters Kluwer discovered 82% said they are utilizing eSignature tools through a partner, and 75% said they are utilizing eContracting tools through a partner.

Only 34% said they are leveraging a more robust eVault solution, Wolters Kluwer found.

“We are certainly starting to see a wider migration and adoption levels for critical digital finance tools like eSignature and eContract, but the industry has a lot of catching up to do in adopting a more complete eVault environment for their documents,” Wolters Kluwer head of auto strategy Tim Yalich said in a news release. “It’s not enough to offer your customer just an electronic way of signing a contract.

“You need to also have a completely digitized back-office process for holding, securitizing, managing, and transitioning all documents between a dealer and lender, and a lender to investor,” Yalich continued.

The rate of digital workflows by automotive professionals reinforces this, as Wolters Kluwer mentioned 85% of respondents said they are leveraging digitized processes for credit application and decisioning, and 82% are using for contract processing and funding.

The newest survey revealed only 43% are leveraging digital tools for securitization or collateralization. However, when asked where they would like to transition more toward digital in 2023, 82% said they would like to digitize more of their securitization or collateralization processes.

Wolters Kluwer said, “It’s critical for automotive and auto finance professionals to continue pushing for a well-rounded, robust digital back-office ecosystem,” explaining that assertion is because 54% of respondents said they are trying to focus on a reduction of errors, and 53% said they want to align with a full suite of technology being used by partners and compete with other finance companies that have become digitized.

Upstart, a leading artificial intelligence lending marketplace, recently announced that Upstart Auto Retail is now certified as a Honda Digital Solutions (HDS) partner.

As an HDS Digital Retailing solution, Upstart Auto Retail’s modern vehicle buying software is now available to Honda dealers and customers nationwide.

Scott Thomas is general manager of Buckeye Honda in Lancaster, Ohio.

“What I love most about Upstart Auto Retail is that it’s a combination of a high-quality digital retail tool with an in-store app that streamlines the process for both customers and sales — making it a game-changer,” Thomas said in a news release from Upstart. “It’s a customer experience tool, a retention tool, and a profit generator all wrapped up into one.”

The addition of Honda bolstered Upstart’s growing roster of OEM certifications, including Kia, Lexus, Mitsubishi, Subaru of America, Toyota and Volkswagen.

Upstart Auto Retail can help franchised dealers provide the fast, transparent, and convenient vehicle buying experience that most consumers now expect.

From building and pricing, all the way through to F&I and signatures, Upstart Auto Retail’s integrated workflow can give customers a consistent omnichannel purchasing journey that serves them when, where, and how they want to interact.

“Today’s customers do a lot of the car-buying process online before heading to the dealership, so Upstart Auto Retail gives them an intuitive mobile and web experience and seamless transitions to the showroom floor,” Upstart Auto Retail general manager Michia Rohrssen said in the news release. “Honda has always had some of the most loyal customers, and our digital retail platform will enable Honda dealers to provide a best-in-class purchasing experience and boost sales.”

Perhaps the digitization of vehicle financing and retailing really is gaining significant momentum.

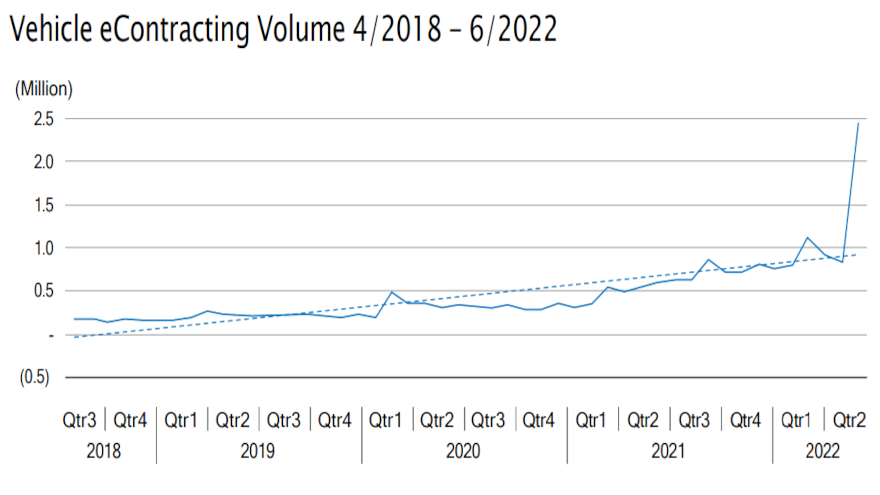

This week, Wolters Kluwer, a global leader in professional information, software solutions and services, announced second quarter results and analysis from its Auto Finance Digital Transformation Index, a resource that tracks the rate at which dealers, service providers and finance companies are seeing growth in the evolution from paper-based finance back-office processes to digital.

According to the index, dealers, service providers and finance companies have fueled a growth rate of 144% during the last 12 months; a 282% growth rate comparing Q2 2022 to Q2 2021; and a growth rate of 78% when comparing to Q1 of 2022.

Wolters Kluwer explained the continued decline in auto sales and lease activity is affecting the overall index eContract volume. Despite this pullback, analysts said it is evident that digital adoption remains high.

The company pointed out the 78% quarter-over-quarter growth rate was helped by a significant Wolters Kluwer client driving further digital adoption by moving their entire platform into the company’s cloud-based environment.

For the year, 2022 has already exceeded 2021 YTD volume by 13%, further illustrating strong continued digital adoption growth, according to Tim Yalich, head of auto strategy for Wolters Kluwer.

“The automotive industry continues to look for digital transformation and adoption across the entire spectrum of operations, illustrated by the continued rise of digital retailing since the pandemic,” Yalich said in a news release.

“However, it is critical for dealers, lenders and service providers to digitize their back-office functions to properly sync with the now digitized consumer facing experience, ensuring all loan and contract documents are converted from paper to digital assets,” he continued.

Wolters Kluwer acknowledged the term “digital transformation” has frequently been discussed in the ever-changing business environment for automotive.

“In 2018 and 2019, the U.S. economy was relatively strong. During that time, there was only a modest increase in digital adoption,” the company said in the full report shared with Auto Fin Journal that also can be found online. “The disruption in 2020 forced retailers and technology providers to innovate faster to meet the demand for contactless engagements. eContract volumes remained steady and elevated compared to previous years, and touchless and virtual transactions became more common. By 2021, digital adoption had begun to accelerate rapidly and was quickly becoming part of our new normal.

“It’s critically important to adopt and achieve this paper-to-digital transformation to improve business processes, remain compliant, reduce risks, achieve higher efficiencies, and satisfy customers through more seamless transactions. This transformation helps automotive professionals keep compliance top of mind proactively with changing regulations and mandates, rather than leaving it on the back burner and opening up to exposure in a paper-based environment,” Wolters Kluwer continued.

“The demand for touchless and virtual engagements remains high, especially with a continued increase in refinancing activity and consumer lease purchases. Used vehicle prices have also risen significantly, and many large used car conglomerates rely on digital platforms to efficiently manage the transaction volume. Whether auto finance and dealer service providers should implement digital technologies is no longer the question. As the need for digitization continues to accelerate, leadership may instead focus on how quickly they can adopt the technology to avoid the risk of being left behind,” Wolters Kluwer went on to say.

Yalich elaborated about those points and more during an episode of the Auto Remarketing Podcast that’s available through the below window.

If your dealership or finance company has an online path for potential vehicle buyers to apply for credit, Cox Automotive said 96% of individuals surveyed are willing to do so.

However, the inaugural Cox Automotive Car Buyer Financing Journey Study also found that only 29% of buyers applied for financing online for their most recent vehicle purchase.

The new study published by Cox Automotive this week also highlighted five other notable findings. Cox Automotive has been researching the vehicle-buying process for 12 years and delved into the credit component this time since 85% of new models and 39% of used vehicles retailed in 2021 were financed, according to Experian data.

The study revealed that buyers who completed key financing steps online saved time and were more satisfied with their time at the dealership than buyers who completed the same steps in person.

The Cox Automotive Car Buyer Financing Journey Study is based on an online survey of 3,050 consumers who financed the purchase or lease of a new or used vehicle during the past 12 months. Analysts said 2,116 survey participants were involved in a new-model transaction, while the other 934 individuals involved in the study took delivery of a used vehicle.

To qualify, the respondents had to be at least 18 years old and had to use the internet during their shopping process. The survey was conducted from Oct. 7 to Nov. 16.

Cox Automotive highlighted that its study measured buyers’ satisfaction with the vehicle financing steps taken, including the finance company selection process and resources used to obtain vehicle financing.

In addition, the research uncovered what financing steps consumers take online versus in person and their comfort level and concerns with financing online.

Here are five other takeaways from the study:

1. Car buyers spend significant time on vehicle financing.

Cox Automotive said nearly all (87%) car buyers explored their financing options before visiting a dealership. The study showed more than a third of the time spent in the vehicle-shopping process is dedicated to financing activities.

Of the 12 hours and 19 minutes spent vehicle shopping, the study indicated 4 hours and 23 minutes are spent on researching financing options, securing financing and signing the contract.

2. Strong relationships matter.

The study showed that 70% of vehicle buyers considered two or more finance companies before choosing one and many had an established relationship with the provider they considered first.

Cox Automotive noted that buyers who were mostly digital — meaning they completed more than 51% of their car-buying journey steps completely online — have stronger loyalty to their finance company, resulting in more direct financing and higher contract satisfaction.

“I trust this lender” was the top reason mostly digital purchasers stated for selecting a particular finance company, according to the study.

3. Vehicle affordability is paramount.

According to the latest Cox Automotive/Moody’s Analytics Vehicle Affordability Index, the median weeks of income needed to purchase the average new vehicle in March was 42.9 weeks, and the estimated typical monthly payment increased to $691, a record high.

The study found that monthly payments and interest rates were considered the most helpful information, as 86% of buyers estimated their monthly payments and 76% compared interest rates.

4. Digitization positively impacts time spent and satisfaction.

Cox Automotive explained mostly digital buyers spent more time researching and securing their financing online and less time at the dealership.

Buyers who applied for financing online saved 30 minutes at the dealership, and those who signed paperwork online saved 38 minutes, according to Cox Automotive research.

Analysts added that both groups of mostly digital buyers indicated that they were more satisfied with the time they spent at the dealership.

5. Many buyers are open to buying a vehicle completely online.

More than three-quarters of the study respondents said that they were open to buying a car completely online, and 47% said they were open to buying a vehicle completely online from a finance company.

After rattling off those five points, Cox Automotive noted what it believed to be another interesting insight from this new study.

Analysts mentioned that although different generations are similar in their willingness to apply for financing online, their need for assistance from a dealer or finance company during the process varies.

While younger generations — Gen Z and millennials — are the most likely to apply for financing online, Cox Automotive discovered nearly half prefer assistance.

While they understand how digital lending works, analysts pointed out that younger buyers need a specialist to guide them and explain the stages of the transaction.

On the other hand, baby boomers are only slightly less likely to apply for financing online, and when they do, only 38% state that they prefer assistance, according to the study.

“Our industry is well past wondering if consumers will ever buy a car online,” said Andy Mayers, lender solutions strategist and associate vice president of operations at Cox Automotive. “This time has come, and the research indicates a solid growth trajectory.

“The auto financing industry needs to be prepared by implementing digital strategies that increase operational efficiency and enable consumers to find, finance and finalize their next vehicle purchase when, where, and however they prefer,” Mayers continued in a news release.

In March, the Titus-Will Automotive Group launched an online channel for consumers in the Puget Sound area of Washington state to buy used cars digitally using technology powered by Cox Automotive’s Esntial Commerce platform.

On Wednesday, Capital Automotive Group, with 29 full-service dealerships across the Carolinas, made a similar move, leveraging the same Cox technology.

Capital’s tool is called RideShift and is designed to be a fully online, automated, pre-owned vehicle e-commerce site, across 20 participating locations.

The site enables consumers to find, finance and purchase a vehicle in a matter of minutes and schedule vehicle delivery or curbside pick-up — whatever the buyer desires.

RideShift uses Cox Automotive’s Esntial Commerce technology to move the consumer through the buying process. It integrates a wide array of Cox Automotive platforms into one centralized and sophisticated tool that benefits both the retailer and customer.

AI-powered shopping features and patent-pending finance automation can enable customers to see pre-qualified payments on every vehicle in inventory and shop by make, model, price and monthly budget.

“We know that each of our customers is unique, and they want car buying to be more convenient — less haggle, less hassle, and less negotiations. RideShift makes the vehicle purchase transaction easy and enables our dealership to reach customers who may not have thought about us before this option in buying fully online,” RideShift director of operations Curtis Driver said in a news release.

“The automotive industry is not immune to disruption be it supply chain or new players, underscoring why innovation and resiliency are essential to business longevity. RideShift enables Capital Automotive Group to transform our business into a true e-commerce offering and has positioned us to be at the forefront of this market transition,” Driver continued.

Capital Automotive Group highlighted that RideShift will be introduced via a regional consumer campaign featuring former Carolina Panthers football star Luke Kuechly.

Through engaging ads, the partnership between Kuechly and RideShift will educate about key benefits, including:

— Ease of shopping, car comparisons, and automated financing with precise payments

— Safe and secure environment to complete and sign all deal paperwork and make payments remotely

— AI-powered technology delivering transparent pricing at vehicle and full deal structure level

— 20 delivery centers across North Carolina for pickup or delivery and service needs

— Seven-day return policy, maximum of 500 miles, three-month or three-thousand-mile warranty, and free delivery within the Carolinas and delivery available throughout the continental U.S.

“With RideShift, Capital Automotive Group customers have straightforward, flexible purchase options, such as delivery or curbside pickup,” said Kuechly, who still resides in North Carolina. “RideShift’s range of customer convenience options — well beyond those of new market players — enable customers to shop how they want, when they want and where they want — all while doing business with people they know and trust.”

Serving the Carolinas for nearly four decades, Capital Automotive Group’s brands include:

— Buick

— GMC

— Chevrolet

— Chrysler

— Dodge

— Ford

— Genesis

— Hyundai

— Jeep

— Kia

— Lincoln

— Mazda

— Nissan

— RAM

— Subaru

“RideShift complements our efforts to build a robust and sustainable automotive industry in the Carolinas that is affordable, profitable and equitable for all involved,” RideShift chief operating officer Lindsey Michael Longo said. “As with every Capital Automotive Group initiative, it is about products, service to our customers, and the community.

“RideShift underscores all of this by transforming the car buying experience unlike anything else available in our market. We are thrilled to be one of the first automotive groups to offer this optimized experience and dedicated level of customer service that nobody else can come close to competing with,” Michael Longo went on to say.

In the next installment of the Auto Remarketing Podcast originating from the Vehicle Finance Conference hosted by the American Financial Services Association earlier this month in Las Vegas, senior editor Nick Zulovich shared a conversation with Cheryl Miller, who is vice president of operations for Dealertrack F&I Solutions.

Miller assessed the current auto-finance landscape, pinpointing what could be the “silver lining” developing out of the pandemic.

To listen to this episode, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.